|

|

市場調査レポート

商品コード

1562736

収益機会の欠如と法的課題にもかかわらず、生成AIが世界を席巻:データセンターのゴールドラッシュは終わるのか?この熱狂はどこに向かうのか?データセンター需要に何が起こるのか?Will the Data Center Gold Rush Come to an End? Generative AI has Taken the World by Storm, despite the Lack of Proven Revenue Opportunities and Huge Legal Challenges, Where Does the Hype Head Next, and What Happens to Data Center Demand? |

||||||

|

|||||||

|

|||||||

| 収益機会の欠如と法的課題にもかかわらず、生成AIが世界を席巻:データセンターのゴールドラッシュは終わるのか?この熱狂はどこに向かうのか?データセンター需要に何が起こるのか? |

|

出版日: 2024年09月26日

発行: MTN Consulting, LLC

ページ情報: 英文 9 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

当レポートは、データセンター需要と、特にウェブスケール分野での投資の増加に拍車をかける生成AIの役割に焦点を当て、当社の設備投資予測のサポートデータを提供します。

ビジュアル

生成AIは、そのあらゆる進化形が投資コミュニティの注目を集めています。生成AIは、初期の勝者が数十年にわたって支配する可能性を秘めた、一生に一度のチャンスであるといった感覚がもたれています。このようなことは、以前にも他の技術革新で起こったことがあり、熱狂はたいてい沈静化します。生成AIは今どこに向かっているのでしょうか?生成AIはバブルであり、普及に向けて苦しい戦いを強いられています。生成AIツールは興味深く、さまざまな応用が可能ですが、深刻な法的課題に直面しており、キラーアプリもありません。

先週、AIデータセンターと関連エネルギー投資に最大1,000億米ドルの資金を調達・運用するファンドが発表されました。この新しいファンド、GAIIP (Global AI Infrastructure Investment Partnership) は、マイクロソフトとAIインフラに期待する金融機関3社、BlackRock、Global Infrastructure Partners (GIP)、アブダビを拠点とするMGX. の提携によるものです。 この新しい提携は、ここ数年で発表された数多くのプライベートエクイティ主導によるデータセンター投資に追加されます。こうした投資は、ChatGPTがリリースされた2022年後半から急増しています。生成AIが2022年末から2023年初頭に展開される以前から、デジタルインフラへの資本調達と投資管理を目的とした新たな投資ビークルは出現していました。2024年に生成AIが盛り上がりを見せ、それが加速しています。

生成AIへの熱狂によるデータセンターへの支出の急増は特にニュースではありません。より大きく、より良く、より多く電力消費する新しいデータセンターは次々と発表されています。これらの新しいインフラに資金を供給するため、新たな金融手段が生まれています。これによって、コンピューター、特に、現在GPUサーバーが主流となっているウェブスケールデータセンターで普及しているコンピューターの巨大なクラスタがが実際にどれほど電力を消費するか、より広く認識されるようになりました。エネルギー消費量は2019年以降、ウェブスケール部門で倍増し、過去2年間はそれぞれ年率15%増加しています。さらに重要なことに、COVID以降、ウェブスケール部門のエネルギー集約度は低下するどころか高まっています。2021年には、収益100万米ドルあたり59MWhのエネルギーが消費され、この数字は2022年には65MWh、2023年には70MWhに増加しています。ウェブスケーラーは、その規模を活かして規模から効率を得ることができるはずであるため、これは注目に値します。生成AIへの大きなコミットメントによって、エネルギー集約度は上昇し続けると思われます。手頃な価格の再生可能電力へのアクセスが不十分であることは、生成AI市場が直面する多くの課題の一つですが、このような課題にもかかわらず、データセンターの支出はウェブスケール市場に牽引され、数四半期は高止まりする可能性が高いです。このような新しいAIモデルを進化させるための競合が進行中であり、早期の勝者は何年も優位性を保てるという見方があります。そのため、スキルを有する開発者、ツール、エネルギー容量、そして土地の争奪戦が繰り広げられています。

対象範囲

言及された組織

|

|

目次

サマリー

イントロダクション

分析

- ウェブスケールの設備投資は24年上半期に急増し、生成AIが好調な見通しを牽引

- ウェブスケーラー上位4社がデータセンター開発を牽引

- クラウド今では大きな収益源となっている

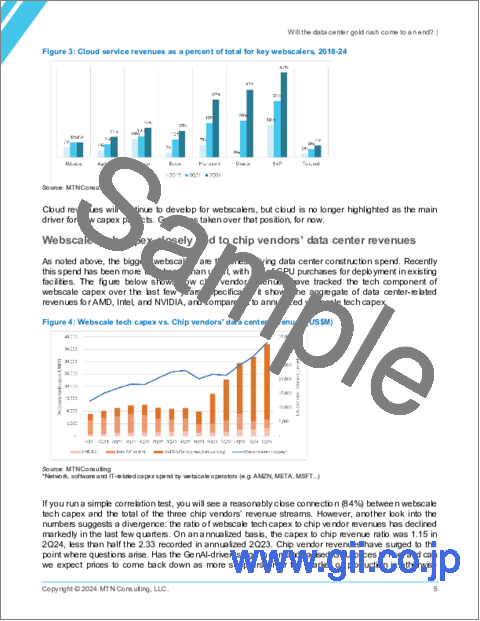

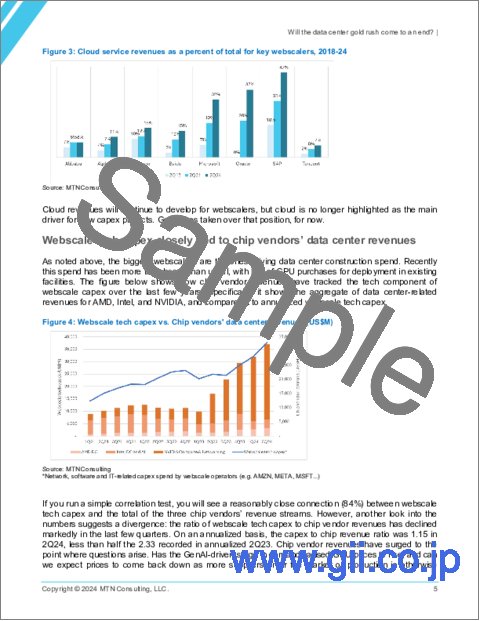

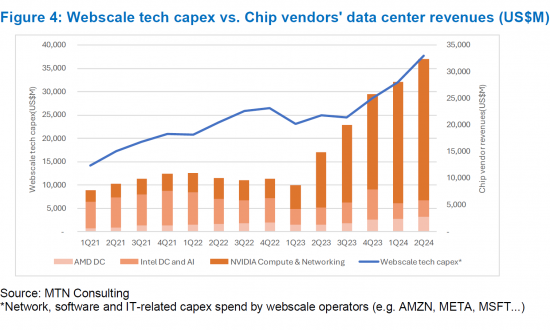

- ウェブスケール技術の設備投資はチップベンダーのデータセンター収益と密接に関係している

- ウェブスケール市場におけるエネルギー消費の動向が懸念される

- 世界の政治と米中貿易戦争による介入

展望

付録

This short brief is focused on data center demand and the role of generative AI in spurring an uptick in investments, particularly in the webscale sector. This brief supports our pending capex forecast update.

VISUALS

Generative AI (GenAI) in all its evolving flavors has captured the attention of the 'investment community' - there is a feeling that GenAI is a once in a lifetime opportunity where the early winners have the potential to dominate for decades. This has happened before with other technology breakthroughs and the hype usually dies down. Where is it going now? There is a strong argument that GenAI is a bubble which faces an uphill battle towards widespread adoption. The tools are interesting and do have a range of applications, but they also face serious legal challenges and lack a killer app. There's also support for the idea that the "smart money" already believes this but doesn't care, due to confidence in being able to sell others on the hype.

Last week a fund was announced to raise and manage up to $100 billion (B) in funding for AI data centers and related energy investments. The new fund, Global AI Infrastructure Investment Partnership (GAIIP), is a partnership between Microsoft and three financial institutions betting big on AI infrastructure: BlackRock, Global Infrastructure Partners (GIP), and Abu Dhabi-based MGX. The new partnership adds to a long list of private equity-driven investments in data centers announced over the last few years. These investments have spiked since late 2022, when ChatGPT was released. Even prior to GenAI rolling out in late 2022/early 2023, new investment vehicles were emerging to raise capital and manage investments in digital infrastructure. With GenAI gaining steam in 2024, that has accelerated.

It's not news that data center spending is surging thanks to widespread enthusiasm for GenAI. The announcements keep on coming: new data centers, bigger and better, consuming more power. New financial vehicles arising to fund all this new infrastructure. With this, a more widespread appreciation of how power-hungry computers actually are - especially the massive clusters of computers prevailing in webscale data centers, now dominated by GPU servers. Energy consumption has doubled in the webscale sector since 2019, growing 15% per year in each of the last two years. More important, since COVID, the webscale sector has become more energy intensive, not less; in 2021, 59 MWh of energy was consumed per US$1M in revenues. That figure grew to 65 in 2022 and 70 in 2023. This is notable, as webscalers are supposed to be able to exploit their size in order to get efficiencies from scale; it's going the opposite direction with data center power consumption. And energy intensity is likely to keep rising with big commitments to GenAI. Inadequate access to affordable, renewable power is one of many challenges faced by the GenAI market. Despite these challenges, data center spend is likely to remain elevated for a few quarters, driven by the webscale market. There is a race underway to train and evolve these new AI models. There is a feeling that the early winners will be able to preserve their advantage for many years. Hence there is a land grab underway: for skilled developers, for tools, for energy capacity, and for land.

Coverage

Organizations mentioned:

|

|

Table of Contents

Summary

Introduction

Analysis

- Webscale capex surged in 1H24 and GenAI is driving strong outlook

- Top four webscalers drive data center developments

- Cloud may have started as a side business but it's now big money

- Webscale tech capex closely tied to chip vendors' data center revenues

- Energy consumption trends in webscale market are concerning

- Global politics and the US-China trade war will intervene

Outlook

Appendix

Figures:

- Figure 1: Webscale sector capex and free cash flow margin trends through 2Q24

- Figure 2: Big data center spenders (webscale and CNNO) - annualized capex and YoY % change

- Figure 3: Cloud service revenues as a percent of total for key webscalers, 2018-24

- Figure 4: Webscale tech capex vs. Chip vendors' data center revenues (US$M)

- Figure 5: Energy intensity (MWh of energy consumption per $M in revenue)