|

市場調査レポート

商品コード

1910936

ロボット支援手術システム:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Robotic Assisted Surgery Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ロボット支援手術システム:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 137 Pages

納期: 2~3営業日

|

概要

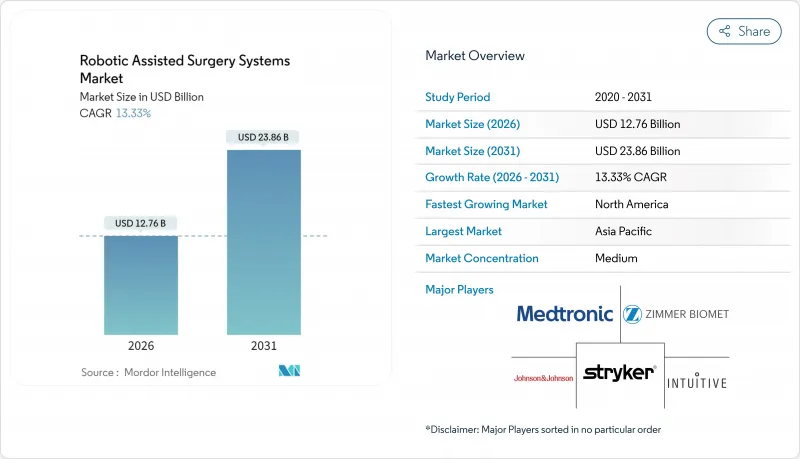

ロボット支援手術システム市場は、2025年に112億6,000万米ドルと評価され、2026年の127億6,000万米ドルから2031年までに238億6,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは13.33%と見込まれています。

低侵襲手術への需要増加、人工知能の急速な統合、5G対応遠隔手術ネットワークの拡大が、主要診療分野におけるプラットフォーム導入を加速させております。主要医療システムでは、従来の腹腔鏡手術と比較して合併症率の低減、入院期間の短縮、再入院率の減少を継続的に実現する本技術を、価値に基づく医療戦略の基盤として位置付けております。手術件数が外来手術センター(ASC)へ移行する中、コンパクトな設置面積に対応し複数手術室のローテーションを可能とするモジュール式・移動型構成への関心が高まっています。既存大手は、低資本支出と迅速なソフトウェア更新を約束するオープンアーキテクチャプラットフォームを導入するコスト重視の課題者との競合激化に直面しています。高齢化、慢性疾患の増加、多くの地域における外科医不足の継続が、長期的な成長の基盤を支えています。

世界のロボット支援手術システム市場の動向と洞察

急速な技術アップグレードと新プラットフォームの投入

da Vinci 5などの次世代システムは、組織への負担を43%軽減する力覚フィードバックモジュールを統合し、外科医の受容性を高め、ロボット支援手術システム市場の拡大を促進しています。部品の小型化により、狭い空間でも操作可能な独立型患者用カートが実現し、手術室の回転時間を短縮し、貴重な手術時間を確保します。ベンダー各社は、単一専門分野向けのニッチプラットフォームを提供する機敏な新規参入企業に対抗するため、製品サイクルを加速させています。また、医療システムは、コアハードウェアを交換せずに進化するソフトウェアアップグレード可能なユニットを好みます。これにより資本予算の効率化が図られ、地域病院における複数ロボットの運用が可能となります。

低侵襲手術・日帰り手術の急増

米国における全手術件数の72%を外来手術センター(ASC)が担うようになり、病院外来部門より45~60%低いコストで手術を実施しながら、92%の患者満足度を維持しています。この移行は、コンパクトで可搬性の高いロボットが手術室間でローテーション可能となり稼働率を最大化できるため、ロボット支援手術システム市場に根本的な利益をもたらします。施設中立性を評価する償還制度改革により、医療提供者は高スループットの関節・脊椎・消化器ワークフロー向けに設計されたロボット手術室への投資を促進しています。プラットフォームベンダーはこれに対応し、消耗品・分析ツール・フリート管理ソフトウェアを「従量課金契約」に統合。これにより費用をASCの収益構造に連動させています。

高コストな調達・ライフサイクル費用

主力ロボットの価格は依然として約200万米ドルで、年間保守契約は10万~20万米ドル、器具は10回使用ごとに更新が必要です。外科医が熟練するには20~40件の指導付き手術が必要であり、導入コストが増加する上、一時的に手術室の生産性を低下させます。手術ごとの支払いまたは成果保証に連動した資金調達スキームが登場しつつありますが、新興市場のCFOは依然として慎重な姿勢を崩しておらず、ロボット支援手術システム市場の浸透を遅らせています。

セグメント分析

2025年、病院が中核ハードウェア群の更新・拡充を継続した結果、システム部門がロボット支援手術システム市場規模の57.84%を占めました。サブスクリプション型分析・AIモジュールにより、ソフトウェア&サービス分野は17.62%のCAGRを達成。機械設計以上にソフトウェアが性能を差別化する現状を浮き彫りにしました。ハードウェアの平均ライフサイクルは10年ですが、四半期ごとのファームウェア更新によりカメラ解像度・運動制御・ワークフローダッシュボードが継続的に強化され、機材の標準化が促進されています。

消耗品は安定した収益源であり続けております。単回使用ステープラー、シーリングデバイス、ドレープは、手術件数が増加する中で無菌状態を保証するからです。オープンソースの取り組みにより、エンジニアはカスタムイメージングフィルターや人間工学的インターフェースを追加でき、臨床医の要求にイノベーションが追いつくことを保証すると同時に、初期の資本支出を保護します。このアーキテクチャはCFOの優先事項に沿い、ロボット支援手術システム市場全体での交換需要を持続させます。

地域別分析

北米は2025年の収益の45.10%を占めました。メディケアの保険適用決定と民間保険の同等性が安定した手術経済性を保証したためです。同地域のロボット支援手術システム市場規模は、機材更新、クリニックベースの手術拡大、自律機能の早期導入を背景に引き続き上昇しています。欧州はこれに続き、da Vinci 5のCEマーク承認により調達パイプラインが拡大した後、大学病院全体で広く普及しています。

アジア太平洋地域は15.26%のCAGRで成長を牽引しており、中国の五カ年計画による国内ロボット製造への補助金と、5G遠隔手術の概念実証パイロットが専門医の待ち時間を短縮しています。インドの一流民間病院チェーンは、肥満手術や心臓手術を求める医療観光客を惹きつけるため、多専門分野のロボット手術センターを展開しており、ロボット支援手術システム市場に追加的な需要をもたらしています。

ラテンアメリカではメキシコとブラジルを中心に導入が徐々に進み、官民連携による共有手術室複合施設の資金調達が行われています。中東・アフリカ地域は依然として発展途上ですが、アラブ首長国連邦での実証プロジェクトでは欧州の指導者による完全遠隔前立腺切除術が実施され、償還枠組みが成熟した際の将来的な普及を予見させています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 急速な技術アップグレードと新プラットフォームの投入

- 低侵襲手術および日帰り手術の急増

- 高齢化と慢性疾患負担の増加

- AI駆動によるワークフロー最適化と自律機能

- 5Gを活用した遠隔手術のパイロット事業が対象範囲を拡大

- オープンアーキテクチャ、モジュラー型ロボット・アズ・ア・プラットフォーム・エコシステム

- 市場抑制要因

- 調達コスト及びライフサイクルコストの高さ

- 複数の管轄区域における規制認可の長期化

- サイバーセキュリティ及びデータ完全性の脆弱性

- 限られた触覚フィードバックが外科医の採用曲線を遅らせています

- テクノロジーの展望

- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品タイプ別

- システム

- 手術用ロボット

- ナビゲーションシステム

- 消耗品・付属品

- ソフトウェアおよびサービス

- システム

- 用途別

- 婦人科手術

- 循環器

- 脳神経外科

- 整形外科手術

- 腹腔鏡検査

- 泌尿器科

- その他の用途

- エンドユーザー別

- 病院

- 外来手術センター

- その他のエンドユーザー

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Intuitive Surgical

- Stryker Corporation

- Johnson & Johnson(Ethicon/Auris)

- Medtronic

- Zimmer Biomet

- Smith & Nephew

- Accuray

- Renishaw

- Globus Medical

- Brainlab

- SRI International

- CMR Surgical

- Asensus Surgical

- Siemens Healthineers(Corindus Vascular)

- Think Surgical

- Titan Medical

- MicroPort MedBot

- Meere Company

- Medicaroid