|

市場調査レポート

商品コード

1643038

マイクロインバータ:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Micro Inverter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| マイクロインバータ:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

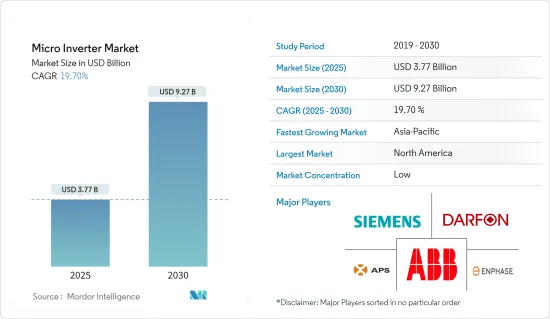

マイクロインバータの市場規模は2025年に37億7,000万米ドルと推計され、予測期間(2025-2030年)のCAGRは19.7%で、2030年には92億7,000万米ドルに達すると予測されます。

モジュールレベルのモニタリングが可能であること、設置が容易であること、設計の柔軟性が向上していること、DCスイッチングポイントが不要であること、従来のインバータよりも安全性が高いことなどが、マイクロインバータ市場の成長を後押ししています。

主なハイライト

- 絶え間ない研究開発活動とマイクロインバータの大幅なコスト削減がマイクロインバータ市場を牽引しています。さらに、そのコンパクトなサイズと多用途性により、市場も大きく後押しされています。さらに、モジュール性、安全性、最大エネルギー収穫量に基づく消費者の要求の高まりが、予測期間中もかなりのペースで市場を牽引すると思われます。

- 超小型インバーターへの需要により、企業は蓄電池の増設を開発できるようになった。2022年4月、エネルギー貯蔵プロバイダーのYotta Energy社(テキサス州オースティン)は、ラスベガスのネリス空軍基地に太陽光+貯蔵マイクログリッドを設置する契約を197万米ドルで獲得したと発表しました。

- マイクロインバータは様々な用途で使用されているため、世界中で広く採用されています。設計の柔軟性や、最大電力点追従(MPPT)技術によってソーラーパネルから最大電力を生成する機能など、さまざまな利点があります。これらの要因により、マイクロインバータ市場は住宅用および商業用アプリケーションにおいて他のインバータよりも優位に立っています。

- マイクロインバータの需要により、各社は蓄電池の増設を開発できるようになった。2022年4月、テキサス州オースティンのヨッタ・エナジー社は、ラスベガスのネリス空軍基地に太陽光+蓄電マイクログリッドを設置する197万米ドルの契約を獲得しました。同社は、バッテリーが同じ方向に向かっていると考えています。モジュール・レベルのマイクロストレージです。この事業では、52ポンド、1kWhのリン酸鉄リチウム電池を、バラストを保持する同じソーラー・モジュール・ラッキング・ギアに配備しています。

- 国際エネルギー機関(政府間機関)によると、世界の再生可能エネルギー発電容量は2020年から60%以上拡大し、2026年には4,800(GW)を超え、化石燃料と原子力を合わせた世界の総発電容量に匹敵すると予測されています。

マイクロインバータ市場動向

住宅用セグメントが市場成長を牽引

- 米国やカナダなどの住宅分野で太陽光発電の採用が増加しているのは、主に電気料金の節約、代替電力源の必要性、気候変動リスクの軽減を望む声が背景にあります。そのため、マイクロインバータ市場の成長機会を後押ししています。

- 予測期間中、太陽光発電コストの低下、住宅用太陽光発電に対する政府の支援政策、FITプログラムおよびインセンティブ、さまざまな政府によって設定された太陽光エネルギーに関する目標などが、マイクロインバータ市場を牽引する重要な要因であるため、屋上太陽光発電のシェアは増加すると予想されます。

- 世界のマイクロインバータ事業の大半は単相装置を提供しています。さらに、単相送電は家庭用アプリケーションに最適であるため、世界的にかなりの需要が観察され、同様にマイクロインバータの主要マーケットプレースの一つとなっています。例えば、米国や欧州では、住宅部門は単相送電に依存しています。

- 太陽光発電モジュールの高効率化など、絶え間ない技術改良がコスト削減を後押ししています。こうした高度にモジュール化された技術の産業化は、規模の経済や競争の激化から製造プロセスやサプライチェーンの改善まで、目覚ましい利益をもたらし、マイクロインバータ市場の成長をさらに加速させています。

アジア太平洋地域が最も高い市場成長率を記録

- アジア太平洋地域は、調査期間中、マイクロインバータの市場として最も急成長すると予想されます。中国、日本、インド、オーストラリアなどの数カ国は、先進的な太陽光発電システムを通じて太陽光発電の設置能力を高め、ひいては電気の安定性を高めようと努力しています。

- アジア太平洋では、住宅用、商業用、太陽光発電所用のマイクロインバータがいくつか設置されています。日本とオーストラリアはマイクロ・インバータ技術の主要な採用国です。さらに、インドと日本では住宅用屋根上太陽光発電の設置が増加しているため、メーカーはこの地域の潜在的な顧客のニーズに応えようとしています。

- インド、中国、日本などの国々では、それぞれの政府が電力部門の近代化のために規制、改革、イニシアチブを敷いています。

- インドでは、住宅用太陽光発電の設置コストは1KW当たり1,000米ドルと推定され、商業用(1KW当たり692米ドル)と比較すると高いです。しかし、インドの設置コストは住宅用(1KWあたり1,638米ドル)、商業用(1KWあたり1,379米ドル)ともに世界平均より安いです。こうした要因がこの地域の市場成長を後押ししています。

- インドはまた、現行のセーフガード税に代わり、2021年に輸入太陽電池セルとインバーターに20%の課税を課す予定です。この課税は、インドの電力大臣が業界代表との電話会談で提案したもので、インド首相が輸入品に20%の基本関税(BCD)を課す意向であることを確認しました。

マイクロインバータ産業の概要

マイクロインバータ市場は非常に細分化されており、 Enphase Energy Inc., Altenergy Power System Inc., DARFON, ABB Ltd, and Siemens AGなどの大手企業が参入しています。これらの市場プレーヤーは、新製品発売、事業拡大、提携、買収などの戦略を駆使して、この市場での足跡を増やしています。

- 2022年4月-ヨッタ・エナジーは350万米ドルの新規資本を獲得し、シリーズA資金調達総額を1,650万米ドルとすることを発表しました。今回の資金調達ラウンドと受賞により、Yottaの資金調達総額は2,550万米ドルを超えます。

- 2021年10月- マイクロインバーターベースのソーラーおよびバッテリーシステムの世界的メーカーであるEnphase Energy, Inc.は、北米の顧客向けにIQ8TMソーラーマイクロインバーターを搭載したEnphase Energy Systemを発表。IQ8は、Enphaseの最も先進的なマイクロインバータです。ライバルのガジェットとは異なり、IQ8は停電中も太陽光を利用してマイクログリッドを構築し、バッテリーなしでバックアップエネルギーを供給することができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 再生可能エネルギーに関する利点と認知度の向上、採用の増加

- 費用対効果の高さとこれらの製品の開発増加

- 市場抑制要因

- 高い設置費用とメンテナンス費用

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19のマイクロインバータ市場への影響評価

第5章 市場セグメンテーション

- タイプ別

- 単相

- 三相

- 通信技術別

- 有線

- ワイヤレス

- 販売チャネル別

- 直接

- 間接販売

- 用途別

- 住宅

- 商業

- 太陽光発電所

- 地域別

- 北米

- 欧州

- アジア太平洋

- 世界のその他の地域

第6章 競合情勢

- 企業プロファイル

- Enphase Energy Inc.

- Altenergy Power System Inc.

- DARFON

- ABB Ltd

- Siemens AG

- Zhejiang Envertech Corporation Limited

- Omnik New Energy

- Sunpower Corporation

- ReneSolaPower

- AEconversion GmbH & Co. KG

- SMA Solar Technology AG

- Sparq Systems

- Sensata Technologies Inc.

- EnluxSolar Co. Ltd

- Delta Energy Systems

- SolarEdge Technologies Inc.

第7章 投資分析

第8章 市場機会と今後の動向

The Micro Inverter Market size is estimated at USD 3.77 billion in 2025, and is expected to reach USD 9.27 billion by 2030, at a CAGR of 19.7% during the forecast period (2025-2030).

The factors like enabling module-level monitoring, easier installation, enhanced design flexibility, removing the need for DC switching points, and better safety than conventional inverters are some factors that are fueling the growth of the micro inverter market.

Key Highlights

- Constant R&D activities and significant reductions in the costs of microinverters drive the micro inverter market. Furthermore, the market also receives a considerable boost due to its compact size and versatility. Additionally, the increasing requirement of consumers, based on modularity, safety, and maximum energy harvest, will continue to drive the market at a considerable pace in the forecast period.

- The demand for micro inverters has enabled companies to develop increased battery storage. In April 2022, energy storage provider Yotta Energy, Austin, Texas, announced that it had been awarded a USD 1.97 million contract to install a solar + storage microgrid at Nellis Air Force Base in Las Vegas.

- Due to the varying use of micro inverters, they are widely adopted worldwide. They provide various benefits such as design flexibility and capabilities like producing the maximum power from solar panels through maximum power point tracking (MPPT) technology. These factors have helped the micro-inverter market gain an advantage over other inverters in residential and commercial applications.

- The demand for micro inverters has enabled companies to develop increased battery storage. In April 2022, Yotta Energy of Austin, Texas, was awarded a USD 1.97 million contract to install a solar + storage microgrid at Nellis Air Force Base in Las Vegas. The company believes batteries are headed in the same direction: module-level microstorage. The business is deploying a 52lb, 1kWh lithium-iron-phosphate battery on the same solar module racking gear, which holds the ballast.

- Worldwide renewable electricity capacity is predicted to expand by more than 60% from 2020 to over 4,800 (GW) by 2026, equaling the total global power capacity of fossil fuels and nuclear power combined, according to the International Energy Agency (an intergovernmental agency).

Micro Inverter Market Trends

Residential Segment to Drive the Market Growth

- The increasing adoption of solar photovoltaics in the residential sector in countries such as the United States and Canada is primarily driven by expected savings in electricity costs, the need for an alternative source of electricity, and the desire to mitigate climate change risk. Therefore, boosting the growth opportunities for the micro inverter market.

- During the forecast period, the share of the rooftop solar PV is expected to increase, on account of decreasing solar PV costs, supportive government policies for residential solar PV, FIT programs and incentives, and targets set by various governments for solar energy are some of the critical factors that are driving the micro inverter market.

- The majority of micro-inverter businesses throughout the world provide single-phase devices. Furthermore, considerable demand is observed globally because single-phase power transmission is best adapted for domestic applications, which is likewise among the primary marketplaces for micro-inverters. For example, the residential sector relies on single-phase power transmission in the United States and Europe.

- Continuous technological improvements, including higher solar PV module efficiencies, drive cost reductions. The industrialization of these highly modular technologies has yielded impressive benefits, from economies of scale and greater competition to improved manufacturing processes and supply chains, further accelerating the micro-inverter market growth.

Asia-Pacific to Register Highest Market Growth

- Asia-Pacific is expected to be the fastest-growing market for micro-inverters over the study period. Several countries, such as China, Japan, India, and Australia, are striving to boost their solar PV installation capacity through advanced solar PV systems that could, in turn, enhance electric stability.

- Asia-Pacific has several micro-inverter installations for residential, commercial, and PV power plant applications. Japan and Australia have been the major adopters of micro-inverter technology. Additionally, the growth in residential rooftop solar PV installations in India and Japan encourages manufacturers to cater to the needs of potential customers in this region.

- In countries such as India, China, and Japan, respective governments have laid regulations, reforms, and initiatives for modernizing the power sector.

- In India, the residential PV installation cost is estimated to be USD 1000 per KW, which is higher when compared to its commercial counterpart (USD 692 per KW). However, the Indian installation costs are cheaper than the global average for both residential (USD 1638 per KW) and commercial (USD 1379 per KW). These factors fuel the market growth in the region.

- India is also set to impose a 20% levy on imported solar module cells and inverters in 2021, replacing the current safeguard duty. The levy was proposed by the Indian power minister during a call with industry representatives, confirming that the Prime Minister of India intended to impose a Basic Custom Duty (BCD) of 20% on imports.

Micro Inverter Industry Overview

The micro-inverter market is highly fragmented, and the major players such as Enphase Energy Inc., Altenergy Power System Inc., DARFON, ABB Ltd, and Siemens AG, among others. These market players are using strategies such as new product launches, expansions, partnerships, acquisitions, and others to increase their footprints in this market.

- April 2022 - Yotta Energy announced obtaining USD 3.5 million in new capital, bringing its total Series A funding to USD 16.5 Million. Yotta's total funding is now over USD 25.5 million due to the current funding round and award.

- October 2021 - Enphase Energy, Inc., the world's premier microinverter-based solar and battery system manufacturer, unveiled the Enphase Energy System with IQ8TM solar microinverters for clients in North America. IQ8 is Enphase's most advanced microinverter to date. Unlike rival gadgets, IQ8 can build a microgrid using sunlight throughout a power outage, delivering backup energy without a battery.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definitions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in benefits and awareness about the renewable energy sources along with increased adoption

- 4.2.2 Cost-effectiveness and increased developments of these products

- 4.3 Market Restraints

- 4.3.1 High installation and maintenance costs

- 4.4 Industry Value Chain Analysis

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Assessment of Impact of Covid-19 on the Micro Inverter Market

5 MARKET SEGMENTATION

- 5.1 By Type

- 5.1.1 Single Phase

- 5.1.2 Three Phase

- 5.2 By Communication Technology

- 5.2.1 Wired

- 5.2.2 Wireless

- 5.3 By Sales Channel

- 5.3.1 Direct

- 5.3.2 Indirect

- 5.4 By Application

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 PV Power Plant

- 5.5 Geography

- 5.5.1 North America

- 5.5.2 Europe

- 5.5.3 Asia-Pacific

- 5.5.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Enphase Energy Inc.

- 6.1.2 Altenergy Power System Inc.

- 6.1.3 DARFON

- 6.1.4 ABB Ltd

- 6.1.5 Siemens AG

- 6.1.6 Zhejiang Envertech Corporation Limited

- 6.1.7 Omnik New Energy

- 6.1.8 Sunpower Corporation

- 6.1.9 ReneSolaPower

- 6.1.10 AEconversion GmbH & Co. KG

- 6.1.11 SMA Solar Technology AG

- 6.1.12 Sparq Systems

- 6.1.13 Sensata Technologies Inc.

- 6.1.14 EnluxSolar Co. Ltd

- 6.1.15 Delta Energy Systems

- 6.1.16 SolarEdge Technologies Inc.