住宅用マイクロインバータの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Residential Micro Inverter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773271

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

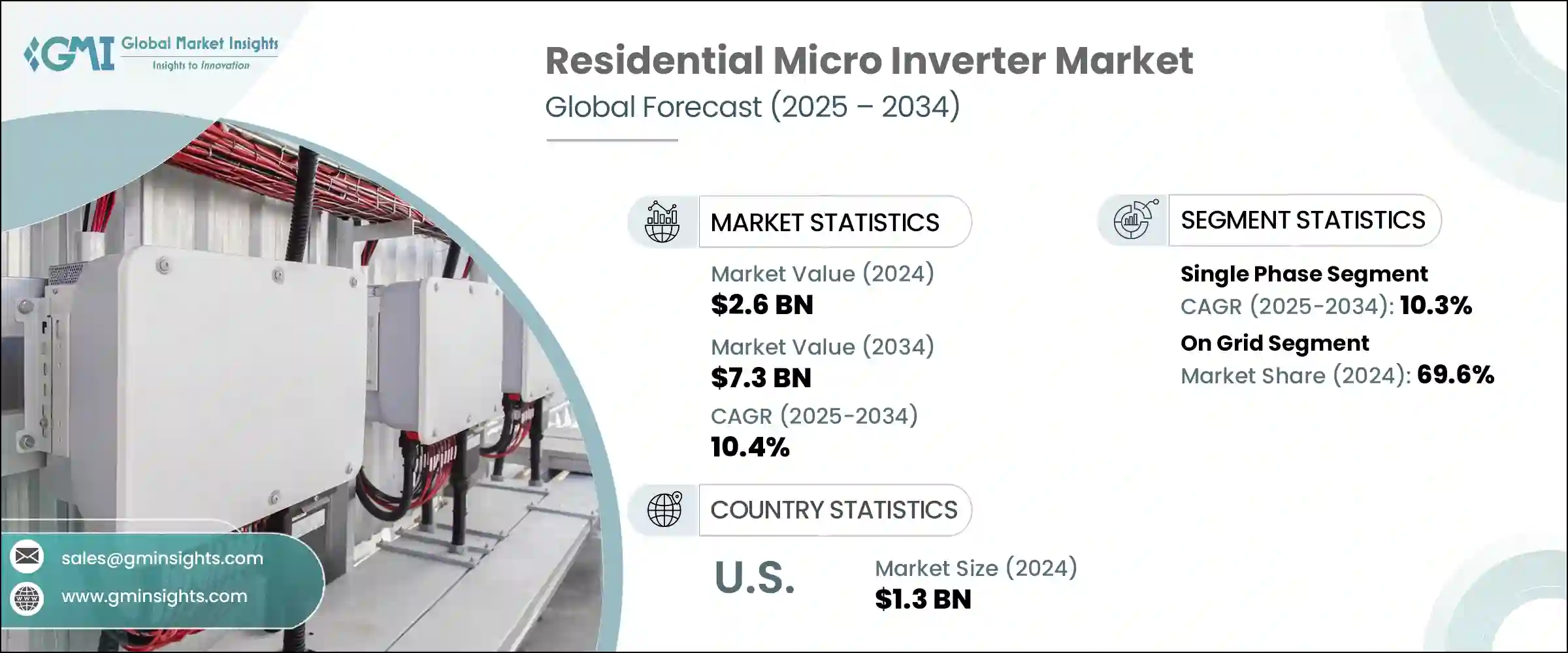

世界の住宅用マイクロインバータの市場規模は、2024年に26億米ドルとなり、CAGR 10.4%で成長し、2034年には73億米ドルに達すると予測されています。

エネルギー自立への関心の高まりと家庭の電力消費の管理強化が、住宅用マイクロインバータソリューションの採用を促進しています。電気料金が上昇し続け、電力会社の送電網が不安定さを増す中、信頼性の高いソーラー屋上システムに投資する家庭が増えています。マイクロインバータは、安定した性能を提供し、変動時にもシステムの整合性を維持する能力で支持されています。特に、政策支援によってPVモジュールやマイクロインバータのような分散型エネルギー資源が後押しされている市場では、政府が支援する奨励金制度や家庭用太陽光発電設備への融資アクセスの改善も普及を後押ししています。

コンパクトなモジュール式太陽光発電設備に対する需要の高まりが、マイクロインバータシステムの住宅導入を後押ししています。これらの装置により、住宅所有者は集中型システムの脆弱性を排除しつつ、各パネルの出力を追跡できるようになります。エネルギーの自律性を重視する傾向が強まり、安全性に関する規制が整いつつあることも、市場の拡大を後押ししています。国の太陽光発電目標に呼応して住宅屋上設置が増加している新興国では、普及が加速しています。こうした動向が続く中、マイクロインバータは、長期的な性能、柔軟性、システムの回復力を確保するための重要な技術として台頭してきています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 26億米ドル |

| 予測金額 | 73億米ドル |

| CAGR | 10.4% |

単相マイクロインバータシステムは、2034年までCAGR 10.3%で成長すると予測されます。これらのソリューションは、個々のパネルレベルでの性能最適化を提供し、継続的な技術革新とコスト効率の改善を通じて強化されています。これらのシステムを家庭用蓄電池やスマートエネルギーソリューションと組み合わせることへの消費者の関心が、住宅用途での拡大に拍車をかけています。インテリジェントなエネルギー管理機能と遠隔監視機能の進歩が、成長をさらに押し上げると予想されます。

独立型住宅用システムは、遠隔地におけるオフグリッドエネルギーソリューションへの嗜好の高まりに支えられ、2025~2034年にかけてCAGR 14.1%で成長する見通しです。エネルギーの自立を求める住宅所有者は、特に送電網へのアクセスが不安定な地域で、蓄電池と統合されたマイクロインバータを選択しています。これらのシステムにより、家庭は自律的に動作し、系統停電時にバックアップを提供できるようになり、エネルギーの安全性と魅力が向上します。

アジア太平洋地域の住宅用マイクロインバータ市場は、2034年までに9億米ドルに達すると予想されます。住宅用PVセットアップにおけるスマートなモジュールレベルのエネルギー管理に対する需要の高まりがその要因です。また、スマートグリッドシステムの継続的な開発と、十分なサービスを受けていない地域の電化も普及を後押ししています。エネルギー自給自足のメリットやシステム全体の出力最適化能力に対する認識が高まっていることも、この地域の市場機会を高めています。

この業界で事業を展開する主要企業には、Sensata Technologies、Hoymiles、Envertech(Zhejiang Envertech)、SMA Solar Technology、Chisageess、Sparq Systems、Fimer Group、Yotta Energy、Altenergy Power Systems、Lead Solar Energy、NingBo Deye Inverter Technology、TSUNESS、Enphase Energy、Growatt New Energy、Chilicon Power、Darfon Electronicsなどがあります。市場での存在感を確固たるものにするため、主要企業はスマートグリッド対応、パネルレベルの性能最適化、統合ストレージソリューションの継続的な研究開発を通じて、技術の差別化を優先しています。各社は、より幅広い屋上構成やエネルギー需要に対応するため、製品ラインを拡大しています。太陽電池パネルメーカー、流通業者、公益事業者との戦略的提携により、市場へのアクセスとブランドポジショニングが向上しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク・課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略的ダッシュボード

- 戦略的取り組み

- 企業の市場シェア

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:フェーズ別、2021~2034年

- 主要動向

- 単相

- 三相

第6章 市場規模・予測:接続性別、2021~2034年

- 主要動向

- スタンドアロン

- オングリッド

第7章 市場規模・予測:地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- イタリア

- ポーランド

- オランダ

- オーストリア

- 英国

- フランス

- スペイン

- ベルギー

- アジア太平洋地域

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- イスラエル

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- エジプト

- ナイジェリア

- ラテンアメリカ

- ブラジル

- チリ

- メキシコ

第8章 企業プロファイル

- Altenergy Power Systems

- Chilicon Power

- Chisageess

- Darfon Electronics

- Enphase Energy

- Envertech(Zhejiang Envertech)

- Fimer Group

- Growatt New Energy

- Hoymiles

- Lead Solar Energy

- NingBo Deye Inverter Technology

- Sensata Technologies

- SMA Solar Technology

- Sparq Systems

- TSUNESS

- Yotta Energy

目次

The Global Residential Micro Inverter Market was valued at USD 2.6 billion in 2024 and is estimated to grow at a CAGR of 10.4% to reach USD 7.3 billion by 2034. Rising interest in energy self-reliance and greater control over household electricity consumption is driving the adoption of residential microinverter solutions. As electricity costs continue to rise and utility grids face growing instability, more homeowners are investing in reliable solar rooftop systems. Microinverters are favored for their ability to deliver consistent performance and maintain system integrity during fluctuations. Government-backed incentive programs and improved access to financing for home solar installations are also encouraging adoption, especially in markets where policy support boosts distributed energy resources like PV modules and microinverters.

Growing demand for compact, modular solar installations is supporting the residential deployment of microinverter systems. These devices allow homeowners to track each panel's output while eliminating the vulnerability of a centralized system. Increasing emphasis on energy autonomy and regulatory alignment around safety is reinforcing market expansion. Adoption is accelerating in emerging economies where residential rooftop installations are rising in response to national solar targets. As these trends persist, microinverters are emerging as a critical technology to ensure long-term performance, flexibility, and system resilience.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.6 Billion |

| Forecast Value | $7.3 Billion |

| CAGR | 10.4% |

Single phase microinverter systems segment is predicted to grow at a CAGR of 10.3% through 2034. These solutions offer performance optimization at the individual panel level and are being enhanced through continuous innovation and cost-efficiency improvements. Consumer interest in pairing these systems with home battery storage and smart energy solutions is fueling their expansion in residential applications. Advancements in intelligent energy management features and remote monitoring capabilities are expected to push growth further.

The standalone residential systems segment is poised to grow at a 14.1% CAGR between 2025 and 2034, supported by the growing preference for off-grid energy solutions in remote regions. Homeowners looking for energy independence, especially in areas with unreliable grid access, are opting for microinverters integrated with battery storage. These systems enable homes to operate autonomously and provide backup during grid outages, improving energy security and appeal.

Asia Pacific Residential Micro Inverter Market will reach USD 900 million by 2034, driven by greater demand for smart, module-level energy management in residential PV setups. Continued development of smart grid systems and electrification of underserved regions is also propelling deployment. Greater public awareness about the benefits of self-sufficient energy use and the ability to optimize overall system output are enhancing market opportunities across the region.

Key players operating across this industry landscape include Sensata Technologies, Hoymiles, Envertech (Zhejiang Envertech), SMA Solar Technology, Chisageess, Sparq Systems, Fimer Group, Yotta Energy, Altenergy Power Systems, Lead Solar Energy, NingBo Deye Inverter Technology, TSUNESS, Enphase Energy, Growatt New Energy, Chilicon Power, and Darfon Electronics. To solidify their market presence, leading residential micro inverter companies are prioritizing technology differentiation through continuous R&D in smart grid compatibility, panel-level performance optimization, and integrated storage solutions. Firms are expanding their product lines to cater to a wider range of rooftop configurations and energy demands. Strategic alliances with solar panel manufacturers, distributors, and utility providers improve market access and brand positioning.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Strategic initiative

- 4.4 Company market share

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Phase, 2021 - 2034 (USD Million & MW)

- 5.1 Key trends

- 5.2 Single phase

- 5.3 Triple phase

Chapter 6 Market Size and Forecast, By Connectivity, 2021 - 2034 (USD Million & MW)

- 6.1 Key trends

- 6.2 Standalone

- 6.3 On grid

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & MW)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 Italy

- 7.3.3 Poland

- 7.3.4 Netherlands

- 7.3.5 Austria

- 7.3.6 UK

- 7.3.7 France

- 7.3.8 Spain

- 7.3.9 Belgium

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Israel

- 7.5.2 Saudi Arabia

- 7.5.3 UAE

- 7.5.4 South Africa

- 7.5.5 Egypt

- 7.5.6 Nigeria

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Chile

- 7.6.3 Mexico

Chapter 8 Company Profiles

- 8.1 Altenergy Power Systems

- 8.2 Chilicon Power

- 8.3 Chisageess

- 8.4 Darfon Electronics

- 8.5 Enphase Energy

- 8.6 Envertech (Zhejiang Envertech)

- 8.7 Fimer Group

- 8.8 Growatt New Energy

- 8.9 Hoymiles

- 8.10 Lead Solar Energy

- 8.11 NingBo Deye Inverter Technology

- 8.12 Sensata Technologies

- 8.13 SMA Solar Technology

- 8.14 Sparq Systems

- 8.15 TSUNESS

- 8.16 Yotta Energy

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 125 Pages

- 納期

- 2~3営業日