|

市場調査レポート

商品コード

1690796

ピースピッキングロボット:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Piece Picking Robots - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ピースピッキングロボット:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 139 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

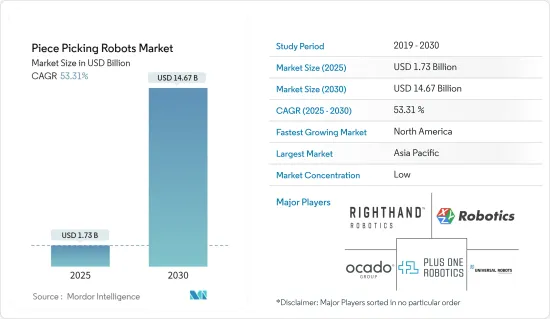

ピースピッキングロボット市場規模は2025年に17億3,000万米ドルと予測され、予測期間(2025~2030年)のCAGRは53.31%で、2030年には146億7,000万米ドルに達すると予測されます。

主要ハイライト

- 自動化への投資が、特にeコマース、物流、製造などのセグメントでピースピッキングロボットの成長を促進しています。効率性、精度、拡大性、費用対効果の向上がこの自動化動向を後押ししています。COVID-19の大流行やeコマース需要の急増によって悪化した倉庫や物流における労働力不足が、自動化への投資拡大に拍車をかけています。その結果、ピッキングロボットがオーダー・ピッキングのような労働集約的な役割を担うことが増え、膨大な労働力への依存度が低下しています。

- 2024年9月、イスラエルのメイタルに本社を置くPickommerceは340万米ドルの資金を獲得しました。同社はこの資金注入により、主力製品であるピースピッキングロボットPickoBotの開発、生産、市場開拓を加速させると発表しました。さらに、Pickommerceは、今日の物流ハブにおける自動化の動向の高まりを強調し、ロボットは現在、主に木箱の回収や荷物の積み下ろしなどの業務を担っていると指摘しました。

- 様々な地域で賃金が上昇する中、企業は運営経費を削減するためにロボットをますます活用するようになっています。ピースピッキングロボットや自動化技術への先行投資は高額になる可能性があるが、長期的な労働力削減の約束や、疲労のない継続的な作業という利点から、魅力的なものとなっています。さらに、バンク・オブ・アメリカは、2025年までに製造業全体の45%がロボティクスに支配されると予測しています。この軌跡に沿って、インドの著名な繊維企業であるレイモンド・リミテッドや、Samsungのようなハイテク大手の主要な中国サプライヤーであるフォックスコン技術・グループといった産業大手は、それぞれ1万人と6万人の労働者を生産設備の自動化で代替する構えです。

- ピースピッキングロボットには多額の先行投資が必要であり、市場成長への顕著な障害となっています。この投資は、支援インフラの必要性によってさらに拡大します。さらに、速度が遅い、従来とは異なる品目をつかむのが難しい、信頼性に懸念があるなど、これらのロボットの技術的な制約が市場拡大の妨げとなっています。

- その他の先端技術と同様、ピースピッキングロボットも定期的なメンテナンスが必要であり、これが稼働停止につながる可能性があります。これらのロボットが高スループット産業にシームレスに適合するためには、このような中断を最小限に抑えることが極めて重要です。さらに、さまざまな産業で独自のワークフローや製品タイプが存在するため、カスタマイズが強く求められています。このニーズは、ピースピッキングソリューションの展開を複雑にし、時間とコストの両方を増加させています。

- 現在進行中のウクライナ紛争は、ピースピッキングロボットの製造に不可欠な原料や部品のサプライチェーンを混乱させています。このような混乱は、欠品、リードタイムの延長、コストの上昇を招き、これらはすべて市場に直接影響を与えます。これに対応するため、企業は代替サプライヤーに目を向けたり、現地生産を強化したりする可能性があり、市場力学や価格設定が再構築される可能性があります。ロシアとウクライナの緊張の持続は、中国の「ゼロトレランス施策」と相まって、世界のインフレの顕著な上昇に拍車をかけた。このインフレ高騰は、電子部品産業や産業オートメーション産業をはじめとするさまざまなセクタに波及し、部品価格を押し上げ、研究市場の成長を阻害しています。さらに、インフレと金利の上昇は個人消費を抑制し、市場の拡大をさらに抑制しています。

ピースピッキングロボット市場動向

小売、倉庫、流通センター、物流センターが最大のエンドユーザーに

- 市場の需要が急速に変化する中、ロボティクスは小売企業にとって不可欠な資産として台頭しています。Amazon、ボサノバ・ロボティクス、ブレインコープなどの大手企業がその先頭に立ち、需要の急増を後押ししています。世界中で、企業は主に人件費削減のため、倉庫にロボットによる自動化を導入しています。

- Amazon.comやWalmartなどの小売大手は、倉庫や小売店舗にモバイルロボットをシームレスに組み込んでいます。消費者の期待がオンデマンド小売に傾く中、在庫戦略にも顕著な変化が生じています。これを踏まえ、小売企業はeコマースのインフラ、オムニチャネル・フルフィルメント、消費者に近接した小型店舗の設置などに投資を注いでいます。

- 倉庫管理だけでなく、小売産業ではロボット工学の波が押し寄せています。店内ロボットは、単に顧客をサポートするだけでなく、在庫管理や清掃業務まで担っています。このような技術革新は、業務効率を高めるだけでなく、小売業者が顧客に合わせたサービスを提供することを可能にしています。技術的な進歩や競合との差別化の推進により、ロボット工学の導入が減速する兆しはないです。小売業が進化を続ける中、ロボティクスを巧みに活用する企業は、市場で優位に立つことができると考えられます。

- 伝統的ビジネスのパラダイムの変化、特に小売セクタの実店舗からオンラインプラットフォームへの軸足は、検査市場の成長に拍車をかけています。例えば、米国国勢調査局のデータは、米国の小売セグメントにおけるeコマースの着実な台頭を強調しています。2024年第2四半期、eコマースは米国の小売売上高全体の16%を占め、前四半期から上昇しました。さらに、2024年4月から6月にかけて、米国の小売eコマース売上高は2,910億米ドルを超え、四半期売上高としては歴史的な高水準を記録しました。

- 急増するeコマース需要、労働力不足、迅速かつ正確な注文処理の必要性に企業が適応しようと努力する中、ピースピッキングロボットの採用は、小売、倉庫、配送センター、物流センター全体で顕著な上昇を確認しています。人工知能(AI)、機械学習、3Dビジョン、自律移動ロボット(AMR)などの技術進歩のおかげで、ピースピッキングロボットは現代の小売・物流インフラに不可欠なコンポーネントとしての地位を固めつつあります。

- Amazon、Walmart、DHL、Alibabaのような産業大手は、これらの技術に継続的に投資しており、世界の物流と小売フルフィルメントの軌道に大きな影響を与え、この市場におけるロボットシステムの急成長を予告しています。

北米が大きな市場シェアを占める

- 米国やカナダといった国々を含む北米セグメントは、世界のピースピッキングロボット市場で大きなシェアを占めています。この優位性は、同地域の先進的技術インフラ、旺盛な自動化需要、製造、物流、小売、倉庫などの発展セグメントに起因します。北米におけるピースピッキングロボット導入の主要促進要因としては、業務効率化の推進、コスト削減、eコマースの急増、労働市場の逼迫などが挙げられます。

- 特に、手作業の繰り返しに頼っている流通・倉庫部門の労働力不足が、米国とカナダでの自動化導入に拍車をかけています。賃金が上昇し、労働力が不足する中、企業は生産を維持し、運営コストを削減するためにロボットソリューションに目を向けています。

- 米国商工会議所によると、パンデミックの発生で製造業は大きな打撃を受け、約140万人の雇用が失われました。米国労働統計局による2023年2月のデータでは、製造業では約75万人が未就職です。予測では、2030年までに米国で200万人以上の製造業が空席になる可能性があります。このような原動力により、製造業と非製造業の両方がオートメーションとロボット技術の採用を加速させています。さらに、数多くの市場参入企業がこの地域でのプレゼンスを積極的に強化しています。

- 例えば、協働作業ロボット(Rapyuta PA-AMR)や倉庫ソリューションで知られるRapyuta Roboticsは、2023年2月に米国子会社を設立しました。この動きは、Rapyutaにとってインドでの設立に続く2番目の国際的ベンチャーとなります。Rapyutaは先進的な技術とハードウェアで、米国市場に大きな価値を提供することを目指しています。シカゴオフィスはRapyutaの全国的な販売とオペレーションを強化する態勢を整えており、アメリカの顧客に対して確実な投資収益率を確保するという同社のコミットメントを強調しています。

- eコマースの急増、技術の進歩、労働問題、自動化への投資の高まりといった要因が、北米のピースピッキングロボット市場の急成長を後押ししています。製造、ロジスティクス、小売、eコマースなどの企業が、効率向上、コスト削減、精度向上のためにロボットを活用しています。人工知能(AI)、機械学習、ロボットシステムの進歩が続いていることから、北米は今後数年で大きな成長を遂げるだけでなく、世界のピースピッキングロボットセグメントで極めて重要な役割を維持することになると考えられます。

ピースピッキングロボット産業概要

ピースピッキングロボット市場には、SSI Schaefer、Swisslog、Dematic、RightHand Roboticsなどの主要企業があります。彼らの存在と継続的なイノベーションが市場情勢を再構築しています。

例えば、2023年9月、先進的な倉庫自動化ソリューションの構築と展開における重要な参入企業であるMOVU Roboticsは、最新のイノベーションである「Movu Eligo」ロボットピッキングアームを発表しました。市場への浸透と先進的製品提供を考えると、競争企業間の敵対関係は予測期間中にエスカレートすると考えられます。

参入障壁が緩やかな中、ベンチャーキャピタル(VC)の支援を受けた新規参入企業数社が勢力を伸ばしており、市場競争が激化する可能性があります。競争上の優位性を確保するため、参入企業は投資収益率(ROI)の向上と迅速なピックレートを目指してボット機能を強化しています。また、人工知能(AI)、ディープラーニング、ビジョン技術などの先端技術にも投資しています。さらに、高品質のコンポーネントへの一貫したアクセスがパフォーマンスを押し上げます。概要の通り、市場は激しい競争と企業間の高い敵対関係が特徴です。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

- COVID-19の自動化産業への影響評価

- ピースピッキングロボットのソフトウェア技術と進化

第5章 市場力学

- 市場の促進要因

- フルケースまたはパレットピッキングからピースフローへのシフトと技術投資の改善

- 自動化投資の増加

- 市場課題

- 速度低下、グリッパーによる特殊品への対応不能、信頼性問題

第6章 市場セグメンテーション

- ロボットのタイプ別

- 協働型

- モバイルその他

- エンドユーザー用途別

- 医薬品

- 小売/倉庫/配送センター/物流センター

- その他のエンドユーザー用途

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Plus One Robotics Inc.

- Ocado Group Plc

- Universal Robots A/S(TERADYNE, INC.)

- XYZ Robotics Inc.

- Righthand Robotics Inc.

- Berkshire Grey Inc.

- Robomotive BV

- Lyro Robotics Pty Ltd.

- Knapp AG

- Grey Orange Pte. Ltd.

- Hand Plus Robotics Pte Ltd

- Dematic Group(KION Group AG)

- Nomagic Inc.

- Fizyr B.V.

- Mujin Inc.

- Nimble Robotics Inc.

- Swisslog Holding AG

- Daifuku Co., Ltd.

- Osaro Inc.

- Covariant

- SSI Schaefer Group

第8章 投資分析

第9章 市場の将来

The Piece Picking Robots Market size is estimated at USD 1.73 billion in 2025, and is expected to reach USD 14.67 billion by 2030, at a CAGR of 53.31% during the forecast period (2025-2030).

Key Highlights

- Investment in automation is propelling the growth of piece-picking robots, particularly in sectors like e-commerce, logistics, and manufacturing. The push for enhanced efficiency, precision, scalability, and cost-effectiveness is driving this automation trend. Labor shortages in warehousing and logistics, exacerbated by the COVID-19 pandemic and surging e-commerce demands, have spurred heightened investments in automation. As a result, piece-picking robots are increasingly taking on labor-intensive roles, such as order picking, thereby diminishing the reliance on a vast workforce.

- In September 2024, Pickommerce, hailing from Meitar, Israel, clinched funding of USD 3.4 million. The company announced that this capital infusion would accelerate the development, production, and marketing of its flagship, the PickoBot piece-picking robot. Furthermore, Pickommerce underscored the escalating trend of automation in today's logistics hubs, noting that robots are now chiefly tasked with duties like crate collection and package unloading.

- As wages climb in various regions, businesses are increasingly leaning on robots to trim operational expenses. While the upfront investment in piece-picking robots and automation tech can be steep, the promise of long-term labor savings and the benefit of continuous, fatigue-free operation make it enticing. Moreover, Bank of America projects that by 2025, a significant 45% of all manufacturing will be dominated by robotics. In alignment with this trajectory, industry giants such as Raymond Limited, a prominent Indian textile firm, and Foxconn Technology Group, a key Chinese supplier for tech behemoths like Samsung, are poised to substitute 10,000 and 60,000 workers, respectively, with automation in their production facilities.

- Piece-picking robots demand a hefty upfront investment, presenting a notable hurdle to market growth. This investment is further magnified by the necessity for supportive infrastructure. Moreover, technical constraints of these robots-such as their slower speeds, difficulties gripping unconventional items, and concerns about reliability-hinder market expansion.

- Like other advanced technologies, piece-picking robots need regular maintenance, which can lead to operational downtime. To ensure these robots fit seamlessly into high-throughput industries, it's crucial to minimize such interruptions. Additionally, given the unique workflows and product types across various industries, there's a strong demand for customization. This need complicates the deployment of piece-picking solutions, increasing both time and costs.

- The ongoing Ukraine conflict has disrupted the supply chain for raw materials and components vital to manufacturing piece picking robots. Such disruptions can result in shortages, longer lead times, and increased costs, all of which directly influence the market. In response, companies might turn to alternative suppliers or bolster local production, potentially reshaping market dynamics and pricing. The persistent Russia-Ukraine tensions, coupled with China's "Zero Tolerance Policy," have spurred a notable rise in global inflation. This inflation surge has reverberated across various sectors, notably the electronic components and industrial automation industries, driving up component prices and stunting the studied market's growth. Furthermore, elevated inflation and interest rates have curtailed consumer spending, further constraining market expansion.

Piece Picking Robots Market Trends

Retail, Warehousing, Distribution Centers, and Logistics Centers to be the Largest End Users

- As market demands shift swiftly, robotics is emerging as a vital asset for retail companies. Leading the charge are major players such as Amazon, Bossa Nova Robotics, and Brain Corp, propelling this surge in demand. Across the globe, organizations are adopting robotic automation in their warehouses, primarily to cut down on labor costs.

- Retail behemoths, including Amazon.com and Walmart, have seamlessly integrated mobile robots into their warehouses and retail outlets. With consumer expectations leaning towards on-demand retail, there's a noticeable shift in inventory strategies. In light of this, retailers are pouring investments into e-commerce infrastructure, omnichannel fulfillment, and setting up smaller stores in closer proximity to consumers.

- Beyond warehousing, robotics is making waves in retail. In-store robots are not just assisting customers; they're managing inventory and even taking on cleaning duties. Such innovations are not only boosting operational efficiency but also allowing retailers to provide tailored services. With technological strides and a push for competitive differentiation, the adoption of robotics shows no signs of slowing down. As the retail landscape continues to evolve, those companies that harness robotics adeptly stand to gain a pronounced advantage in the market.

- The shifting paradigms of traditional businesses, notably the retail sector's pivot from physical stores to online platforms, are fueling growth in the examined market. For instance, data from the US Census Bureau underscores the steady ascent of e-commerce's prominence in the US retail arena. In Q2 2024, e-commerce constituted 16% of the total retail sales in the US, a rise from the previous quarter. Additionally, from April to June 2024, US retail e-commerce sales eclipsed USD 291 billion, marking a historic high for quarterly revenue.

- As businesses strive to adapt to surging e-commerce demands, labor shortages, and the necessity for swift and accurate order fulfillment, the adoption of piece-picking robots is witnessing a notable uptick across Retail, Warehousing, Distribution Centers, and Logistics Centers. Thanks to technological advancements such as artificial intelligence (AI), machine learning, 3D vision, and Autonomous Mobile Robots (AMRs), piece-picking robots are cementing their status as integral components of modern retail and logistics infrastructure.

- With industry giants like Amazon, Walmart, DHL, and Alibaba continuously investing in these technologies, the trajectory of global logistics and retail fulfillment is set to be significantly influenced, heralding rapid growth for robotic systems in this market.

North America Holds Significant Market Share

- The North American segment, encompassing countries like the US and Canada, holds a significant share of the global piece-picking robots market. This dominance is attributed to the region's advanced technological infrastructure, a robust demand for automation, and evolving sectors such as manufacturing, logistics, retail, and warehousing. Key drivers for the adoption of piece-picking robots in North America include the push for operational efficiency, cost reduction, the surge of e-commerce, and a tightening labor market.

- Labor shortages, particularly in distribution and warehousing sectors reliant on repetitive manual tasks, have notably spurred the adoption of automation in the US and Canada. With wages on the rise and labor becoming scarce, companies are turning to robotic solutions to sustain production and curtail operating costs.

- According to the US Chamber of Commerce, the manufacturing sector faced a major blow, shedding around 1.4 million jobs at the pandemic's onset. Data from February 2023 by the US Bureau of Labor & Statistics highlighted about 750,000 unfilled positions in manufacturing. Projections suggest over 2 million manufacturing roles could remain vacant in the US by 2030. Such dynamics have driven both manufacturing and non-manufacturing entities to increasingly adopt automation and robotic technologies. Furthermore, numerous market players are actively bolstering their presence in the region.

- For example, in February 2023, Rapyuta Robotics, known for its collaborative pick-assist robots (Rapyuta PA-AMR) and warehouse solutions, inaugurated its US subsidiary. This move marks Rapyuta's second international venture following its establishment in India. With its advanced technology and hardware, Rapyuta aims to deliver substantial value to the US market. The Chicago office is poised to boost Rapyuta's sales and operations nationwide, underscoring the company's commitment to ensuring a solid return on investment for its American customers.

- Factors like the e-commerce surge, technological advancements, labor challenges, and heightened investment in automation are propelling the swift growth of North America's piece-picking robots market. Businesses spanning manufacturing, logistics, retail, and e-commerce are leveraging these robots to enhance efficiency, cut costs, and boost accuracy. Given the ongoing advancements in artificial intelligence (AI), machine learning, and robotic systems, North America is not only poised for significant growth in the coming years but is also set to maintain its pivotal role in the global piece-picking robot arena.

Piece Picking Robots Industry Overview

The piece-picking robot market includes several key players, including SSI Schaefer, Swisslog, Dematic, and RightHand Robotics. Their presence and ongoing innovations are reshaping the market landscape.

For instance, in September 2023, MOVU Robotics, a significant player in crafting and deploying advanced warehouse automation solutions, announced its latest innovation, the 'Movu Eligo' robot picking arm. Given their market penetration and advanced product offerings, competitive rivalry is set to escalate during the forecast period.

With moderate entry barriers, several Venture Capital (VC)-)-backed newcomers have gained traction, potentially heightening market competition. To secure a competitive advantage, players enhance bot capabilities for better Return on Investment (ROI) and quicker pick rates. They also invest in advanced technologies like Artificial Intelligence (AI), deep learning, and vision tech. Moreover, consistent access to quality components boosts performance. In summary, the market is characterized by intense competition and high rivalry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porters Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of COVID-19 on the Automation Industry

- 4.5 Piece-picking Robot Software Technology and Evolution

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 A Shift from Full-case or Pallet Picking to Piece Flow and Improved Technology Investments

- 5.1.2 Increasing Investments in Automation

- 5.2 Market Challenges

- 5.2.1 Slower Speeds, Inability of the Grippers to Deal with Unusual Items, and Reliability Issues

6 MARKET SEGMENTATION

- 6.1 By Type of Robot

- 6.1.1 Collaborative

- 6.1.2 Mobile and others

- 6.2 By End User Application

- 6.2.1 Pharmaceutical

- 6.2.2 Retail/Warehousing/Distribution Centers/Logistics Centers

- 6.2.3 Other End User Applications

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Plus One Robotics Inc.

- 7.1.2 Ocado Group Plc

- 7.1.3 Universal Robots A/S (TERADYNE, INC.)

- 7.1.4 XYZ Robotics Inc.

- 7.1.5 Righthand Robotics Inc.

- 7.1.6 Berkshire Grey Inc.

- 7.1.7 Robomotive BV

- 7.1.8 Lyro Robotics Pty Ltd.

- 7.1.9 Knapp AG

- 7.1.10 Grey Orange Pte. Ltd.

- 7.1.11 Hand Plus Robotics Pte Ltd

- 7.1.12 Dematic Group (KION Group AG)

- 7.1.13 Nomagic Inc.

- 7.1.14 Fizyr B.V.

- 7.1.15 Mujin Inc.

- 7.1.16 Nimble Robotics Inc.

- 7.1.17 Swisslog Holding AG

- 7.1.18 Daifuku Co., Ltd.

- 7.1.19 Osaro Inc.

- 7.1.20 Covariant

- 7.1.21 SSI Schaefer Group