|

|

市場調査レポート

商品コード

1644414

組み込みSIM(eSIM):市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Embedded SIM (eSIM) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 組み込みSIM(eSIM):市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

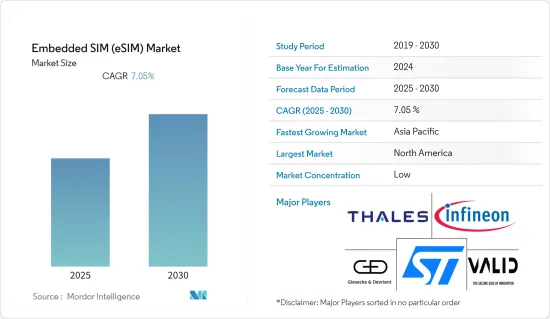

組み込みSIM(eSIM)市場は、予測期間中にCAGR 7.05%を記録する見込みです。

eSIMは、スマートフォン、タブレット、ウェアラブルデバイス、その他のIoTデバイスなどのデバイスに直接埋め込まれる小型のプログラマブルチップであり、物理的なSIMカードを必要とせずにリモートSIMプロビジョニングを可能にします。

主なハイライト

- モノのインターネット(IoT)はeSIM採用の主要な促進要因の一つです。eSIMは、IoTデバイスを世界に展開・管理するためのスケーラブルなソリューションを提供しました。

- コネクテッドとM2M(マシン・ツー・マシン)のエコシステムの進歩は、市場成長の主な促進要因でした。5Gネットワークの成長もeSIM採用の新たな機会を生み出しています。企業は資産追跡、スマートメーター、産業モニタリング、サプライチェーン管理などのM2M展開にeSIMを採用しました。

- スマートデバイスに対する需要の高まりは、eSIM技術の採用を増加させる重要な原動力の一つでした。スマートフォン、タブレット、ウェアラブル、コネクテッドカー、さまざまなモノのインターネット(IoT)デバイスを含むスマートデバイスは、消費者や産業用アプリケーションでより普及しています。

- セキュリティと相互運用性の標準化の問題が市場の成長を抑制しています。従来のSIMカードでは、SIMの改ざんや交換には物理的なアクセスが必要であり、悪意ある行為者が接続を侵害することはより困難です。しかし、eSIMはデバイスの回路に直接はんだ付けされるため、不正アクセスやクローニングの可能性は重大なセキュリティリスクとなりうる。

組み込みSIM(eSIM)の市場動向

スマートフォンアプリケーションセグメントが大きな市場シェアを占める見込み

- eSIMは物理的なSIMカードを必要としないため、ユーザーは携帯電話会社のアクティベーションや切り替えがより簡単に行えます。eSIMを使えば、ユーザーは物理的なSIMカードを入手したり、それが届くのを待ったりする手間をかけることなく、新しいキャリアのプロファイルをリモートでデバイスにプロビジョニングすることができます。

- eSIM技術は、スマートフォンにおけるデュアルSIM機能の採用を可能にしました。eSIMの物理カードスロットを組み合わせることで、ユーザーは同じ端末で2つの有効な電話番号を持つことができ、これは旅行者、ビジネスマン、複数の携帯電話契約を持つ人々にとって特に便利です。

- モバイルネットワーク事業者にとっては、eSIM技術は新規顧客の獲得においてより大きな柔軟性を提供します。MNOは、小売チャネルを通じて物理的なSIMカードを配布する代わりに、eSIMをリモートでプロビジョニングすることができ、アクティベーションプロセスを簡素化し、流通コストを削減することができます。

- eSIMは、IoTデバイスの接続を可能にする上で重要な役割を果たしています。スマートフォンは様々なIoTアプリケーションのゲートウェイであり、eSIM技術はIoTデバイスをセルラーネットワークに接続する安全で効率的な方法を提供します。

- 現在進行中の5Gネットワークの開発とIoTデバイスの普及により、スマートフォンやその他の接続デバイスへのeSIMの統合がさらに進むと予想されます。エリクソンによると、2022年の世界における重要なIoTおよびブロードバンドとのセルラーIoT接続数は約15億。5年後には、同接続タイプのセルラーIoT接続数は毎年着実に増加し続け、最大33億に達するという予測です。

北米が大きな市場シェアを占める見込み

- 北米では、ヘルスケア、自動車、スマートホーム、産業用アプリケーションなど、さまざまな業界でIoTデバイスの導入が急速に増加しています。eSIM技術は、これらのデバイスにシームレスな接続性を提供する上で重要な役割を果たし、eSIM市場の成長を牽引しています。

- メーカーはeSIM技術をスマートフォン、タブレット、ウェアラブル、IoT機器など多くの機器に組み込んでいます。eSIMに対応する機器が増えるにつれて、eSIMサービスの需要も高まると予想されます。

- 北米では5Gネットワークの展開が加速しており、eSIM技術はシームレスな接続性を提供することで5Gネットワークの機能を補完し、消費者による通信事業者やプランの切り替えを容易にします。シスコシステムズによると、北米では2022年にウェアラブル端末を使った5G接続が最も多くなるといいます。北米における4億3,900万接続は、2017年の4Gネットワークへの接続を2億2,200万接続上回る。

- eSIMが同地域で大幅に安価になり、安全な国際ローミングソリューションに関連する計画は、同地域でのeSIMの採用をかなり促進します。eSIMをサポートする携帯電話では、ユーザーは複数の国またはローミングプランから選択することができ、複数国のオペレーターは米国モバイルのソリューションよりも大幅に割高になる傾向があります。ユーザーが海外に旅行する場合は、キャリアのローミングプランを選択できます。eSIMを使えば、ユーザーはQRコードをスキャンしたり、端末上のメニューから新しい通信事業者を選んだりできるので、通信事業者の変更やローミングが非常に簡単になります。

- 2022年12月、コンシューマー向けテクノロジーのトップ・サブスクリプション・プロバイダーのひとつであるグローバーは、米国でテクノロジーをレンタルする顧客向けのMVNO、グローバー・コネクトを発表しました。同国の顧客は、グローバー・コネクトを利用することで、eSIM対応のテクノロジー機器を素早くアクティベートできます。また、グローバーは、あらゆるビジネスやブランドがMVNOになることを可能にするテレコム・アズ・ア・サービス・プラットフォームの世界的リーダーの1つであるギグス社と提携し、この革新的な新サービスを導入しました。顧客は米国での会計時にグローバーのeSIMを購入することができ、まもなく欧州地域でも利用可能になります。

組み込みSIM(eSIM)業界の概要

組み込みSIM(eSIM)市場は断片化されており、Gemalto N.V.(タレス・グループ)、Giesecke+Devrient GmbH、STMicroelectronics N.V.、Infineon Technologies AG、Valid S.A.などの主要企業が存在します。市場のプレーヤーは、製品提供を強化し、持続可能な競争優位性を獲得するために、提携や買収などの戦略を採用しています。

2023年2月、Giesecke+Devrient(G+D)とそのパートナーであるNetLyncは、AirOn360 ESを発表しました。AirOn360 ESは、物理的なSIMカードまたはeSIMからiPhoneへのシームレスなSIM転送を含むエンタイトルメントの展開を可能にし、携帯電話事業者が簡素化されたデジタルアクティベーションプロセス、全デバイスの同期、または(e)SIM転送などの便利なサービスを提供できるようにします。ユーザーにとっては、eSIMによって、既存のプランを簡単にデジタル接続したり、迅速に移行したりすることができ、1つのデバイスで複数の携帯電話プランを利用できるようになります。

2022年11月、STマイクロエレクトロニクスは、Google Pixel 7のセキュアで非接触な利便性を支えるThalesと協業しました。ST54KシングルチップNFCコントローラとセキュア・エレメントは、ThalesセキュアOSと組み合わされ、組み込みSIM、交通機関発券、デジタル・カーキー・アプリケーションにおいて優れた性能を発揮します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界利害関係者分析オペレーター、OEM、システムインテグレーター

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19が接続状況に与える影響

- e-SIM対応デバイスの世界出荷台数に関する調査範囲

第5章 市場力学

第6章 市場促進要因

- コネクテッド&M2Mエコシステム分野の進展

- スマートデバイスに対する需要の高まり

- eSIMが従来の代替品よりも提供する使いやすさとアクセス性

第7章 市場課題市場の課題

- セキュリティ、相互運用性の標準化問題

第8章 市場機会

- M2Mの普及に向けた極めてポジティブな予測

第9章 世界のSIMカード情勢分析(出荷数・地域別内訳)

第10章 市場セグメンテーション

- 用途別

- スマートフォン

- タブレット&ノートPC

- ウェアラブル

- M2M(産業、自動車など)

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- アジア

- 中国

- 韓国

- 日本

- オーストラリアとニュージーランド

- ラテンアメリカ

- 中東・アフリカ

- 北米

第11章 競合情勢

- 企業プロファイル

- Gemalto N.V.(Thales Group)

- Giesecke+Devrient GmbH

- STMicroelectronics N.V.

- Infineon Technologies AG

- Valid S.A.

- Idemia(Advent International Corp)

- Workz Group

- Truphone Limited

- Gigsky, Inc.

- ARM Limited

第12章 ベンダーのポジショニング分析

第13章 市場の展望

The Embedded SIM Market is expected to register a CAGR of 7.05% during the forecast period.

An eSIM is a small, programmable chip embedded directly into devices, such as smartphones, tablets, wearable devices, and other IoT devices, allowing remote SIM provisioning without needing a physical SIM card.

Key Highlights

- The Internet of Things (IoT) was one of the key drivers for eSIM adoption. As the number of connected devices increased, managing physical SIM cards for each device became impartial. eSIM provided a scalable solution for deploying and managing IoT devices globally.

- Advancements in the connected and M2M (machine-to-machine) ecosystem were key drivers in the market's growth. The growth of the 5G network also creates new opportunities for eSIM adoption. Enterprises embraced eSIM for their M2M deployments, such as asset tracking, smart meters, industrial monitoring, and supply chain management.

- The growing demand for smart devices was one of the key drivers that increased the adoption of eSIM technology. Smart devices, including smartphones, tablets, wearables, connected cars, and various Internet of Things (IoT) devices, have become more prevalent in consumer and industrial applications.

- Security and interoperability standardization issues are restraining the market growth. With traditional SIM cards, physical access is required to tamper with or replace the SIM, making it more difficult for malicious actors to compromise the connection. However, as eSIM is soldered directly onto the device's circuitry, the potential for unauthorized access or cloning could be a significant security risk.

Embedded SIM (eSIM) Market Trends

Smartphones Application Segment is Expected to Hold Significant Market Share

- eSIM technology has been increasingly integrated into smartphones, bringing numerous benefits to consumers and mobile network operators (MNOs). eSIM eliminates the need for physical SIM cards, allowing users to activate and switch between mobile carriers more easily. With eSIMs, users can remotely provision their devices with a new carrier's profile without the hassle of acquiring a physical SIM card and waiting for it to be delivered.

- eSIM technology has enabled the adoption of dual-SIM functionality in smartphones. With a combination of eSIM physical card slots, users can have two active phone numbers on the same devices, which is especially useful for travelers, business professionals, or people with multiple cellular subscriptions.

- For mobile network operators, eSIM technology offers greater flexibility in onboarding new customers. Instead of distributing physical SIM cards through retail channels, MNOs can remotely provision eSIMs, simplifying the activation process and reducing distribution costs.

- eSIM plays a significant role in enabling connectivity for IoT devices. Smartphones are a gateway for various IoT applications, and eSIM technology provides a secure and efficient way to connect IoT devices to cellular networks.

- The ongoing development of 5G networks and the proliferation of IoT devices are expected to further the integration of eSIM in smartphones and other connected devices. According to Ericsson, the number of cellular IoT connections with critical IoT and broadband globally in 2022 was approximately 1.5 billion. In five years, the forecast is that the number of cellular IoT connections with the same connection type will continue to rise steadily each year, up to 3.3 billion.

North America is Expected to Hold Significant Market Share

- North America has witnessed a rapid rise in the adoption of IoT devices across various industries, including healthcare, automotive, smart home, and industrial applications. eSIM technology plays a crucial role in providing seamless connectivity for these devices, driving the growth of the eSIM market.

- Manufacturers have incorporated eSIM technology into many devices, including smartphones, tablets, wearables, and IoT devices. As more devices become eSIM-enabled, the demand for eSIM services is expected to rise.

- The deployment of 5G networks in North America has been gaining momentum. eSIM technology complements the capabilities of the 5G network by providing seamless connectivity and making it easier for consumers to switch between carriers and plans. According to Cisco Systems, North America will have the most 5G connections made using wearable devices in 2022. The 439 million connections in North America would be 222 million more than those made to 4G networks in 2017.

- The plans related to eSIM becoming significantly cheap in the region and a secure international roaming solution considerably drive the adoption of eSIM in the region. On phones with eSIM support, the user can select from several individual countries or roaming plans, where the multi-country operators tend to be significantly more expensive than US Mobile's solution. If the user is traveling abroad, he can select the carrier's roaming plan. The user can also buy a local SIM card or a multi-country travel SIM card like KnowRoaming, which is the most expensive. eSIM lets the user scan a QR code or pick a new carrier from an on-device menu, making it much easier to switch carriers or roam.

- In December 2022, Grover, one of the top subscription providers for consumer technology, unveiled Grover Connect, an MVNO for clients renting technology in the United States. The country clients can quickly activate any eSIM-enabled technology gadget using Grover Connect. Also, Grover partnered with Gigs, one of the global leaders in telecom-as-a-service platforms in the world that enables any business or brand to become an MVNO, to introduce this innovative new offering. Customers can purchase a Grover eSIM at checkout in the United States, which will soon be available in its European regions.

Embedded SIM (eSIM) Industry Overview

The embedded SIM (eSIM) market is fragmented, with the presence of major players like Gemalto N.V. (Thales Group), Giesecke+Devrient GmbH, STMicroelectronics N.V., Infineon Technologies AG, and Valid S.A. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

In February 2023, Giesecke+Devrient (G+D) and its partner NetLync launched AirOn360 ES, enabling Mobile Network Operators to deploy Entitlements, including the seamless SIM transfer on iPhone from physical SIM card or eSIM, allowing mobile operators to offer convenient services such as simplified and digital activation processes, synchronization of all devices, or (e)SIM transfers. For users, eSIM allows them to easily connect or quickly transfer their existing plans digitally and provides for multiple cellular plans on a single device.

In November 2022, STMicroelectronics collaborated with Thales, which powers secure, contactless convenience in Google Pixel 7. The ST54K single-chip NFC controller and secure element combine with Thales secure OS for superior performance in embedded SIM, transit ticketing, and digital car-key applications.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis Operator, OEM & System Integrators

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Impact of COVID-19 on the Connectivity Landscape

- 4.5 Coverage on e-SIM Enabled Device Shipments Globally

5 MARKET DYNAMICS

6 Market Drivers

- 6.1 Advancements in the Field of Connected & M2M Ecosystem

- 6.2 Growing Demand for Smart Devices

- 6.3 Ease of Use and Access Provided by eSIM over Traditional Substitutes

7 Market Challenges

- 7.1 Security, Interoperability Standardization Issues

8 Market Opportunities

- 8.1 Highly Positive Forecasts for M2M Adoption

9 GLOBAL SIM CARD LANDSCAPE ANALYSIS (SHIPMENTS & REGIONAL BREAKDOWN)

10 MARKET SEGMENTATION

- 10.1 By Application

- 10.1.1 Smartphones

- 10.1.2 Tablets & Laptops

- 10.1.3 Wearables

- 10.1.4 M2M (Industrial, Automotive, etc.)

- 10.2 By Geography

- 10.2.1 North America

- 10.2.1.1 United States

- 10.2.1.2 Canada

- 10.2.2 Europe

- 10.2.2.1 United Kingdom

- 10.2.2.2 Germany

- 10.2.2.3 France

- 10.2.3 Asia

- 10.2.3.1 China

- 10.2.3.2 South Korea

- 10.2.3.3 Japan

- 10.2.3.4 Australia and New Zealand

- 10.2.4 Latin America

- 10.2.5 Middle East and Africa

- 10.2.1 North America

11 COMPETITIVE LANDSCAPE

- 11.1 Company Profiles

- 11.1.1 Gemalto N.V. (Thales Group)

- 11.1.2 Giesecke+Devrient GmbH

- 11.1.3 STMicroelectronics N.V.

- 11.1.4 Infineon Technologies AG

- 11.1.5 Valid S.A.

- 11.1.6 Idemia (Advent International Corp)

- 11.1.7 Workz Group

- 11.1.8 Truphone Limited

- 11.1.9 Gigsky, Inc.

- 11.1.10 ARM Limited