|

市場調査レポート

商品コード

1445956

海軍用アクチュエーター・バルブ:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Naval Actuators And Valves - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 海軍用アクチュエーター・バルブ:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

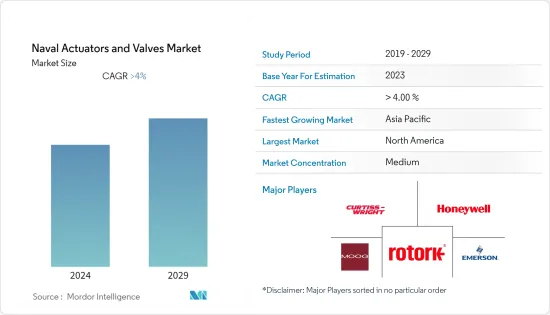

Equal-4.64の観点からの海軍用アクチュエーター・バルブの市場規模は、予測期間(2024年から2029年)中に4.64%のCAGRで、2024年の33億4,000万米ドルから2029年までに41億8,000万米ドルに成長すると予想されます。

主なハイライト

- 海戦戦線における高性能レーダーや長距離照準システムなどの新技術の出現により、各国は海軍能力の近代化とアップグレードを推進しています。アクチュエーター・バルブはすべての海軍艦船サブシステムの重要な部分を形成するため、新しい海軍艦艇の導入により、仕様どおりのシステム性能を確保するためにアクチュエーター・バルブに対する並行した需要が生じる可能性があります。

- 厳しい規制政策により、予測期間中の市場の成長が抑制されると予想されます。海洋産業は、主に海洋活動に伴うリスクのため、厳しく規制されています。

- 高度な統合戦闘システムまたは海軍の使用の人気の高まりは、市場に新たな機会を提供すると予想されており、これは今後の期間に焦点を当てている市場にプラスの影響を与えると予想されます。

海軍用アクチュエーター・バルブの市場動向

防衛部門が市場を独占すると予想される

国際戦略情勢の重大な変化により、国際安全保障システムの構成は、進行中のいくつかの世界紛争を煽る覇権主義、一国主義、強権政治の増大によって損なわれてきました。米国、英国、中国、インドなどの軍事大国は海軍火力の増強に注力しており、国家安全保障に対する進化する脅威に対処するためにいくつかの艦隊の近代化と調達契約が進行中です。

2022年、ロシアとウクライナの間の戦争により、各国の国防予算がさらに膨らみ、世界的に軍隊の作戦準備を再評価する必要性が高まっています。 2022年の世界の軍事支出は前年比3.7%増加し、過去最高の2兆2,000億米ドルに達しました。ロシアとウクライナの戦争は、2022年の支出増加の主な原動力でした。2022年の最大の支出国5つは米国、中国、ロシア、インド、サウジアラビアで、世界の軍事支出の63%を占めました。

30年間の造船計画によれば、米国は2024年までに314隻の有効艦隊規模を達成するために、55隻の新造船を調達することを構想しています。アジア太平洋地域では、中国やインドなどの有力国も海軍艦隊の規模と能力を強化しており、ライバル国に対して技術的優位性を獲得します。このような誘導プログラムは、防衛プラットフォーム用の新しい海軍艦艇の設計および建造におけるアクチュエーター・バルブの需要を促進することが想定されています。

予測期間中に北米が市場を独占する

この市場は、国内の平和と安全を確保することに加えて、この地域での軍事的優位性を達成するための米国海軍による先進兵器の調達によって動かされています。米国は、陸、空、水のすべての領土に対する軍事力を強化するために、その膨大な技術力をいくつかの兵器システムの先住民開発に投資してきました。

2023年度予算案において、米国海軍は海軍に1,805億米ドル、海兵隊に503億米ドルを含む総額2,308億米ドルの予算要求を提案しました。アメリカの海軍拡張プロジェクトの一環として、米国海軍は2023会計年度予算で、海軍からさまざまな軍艦や空母艦隊を除外したり包含したりして艦隊を近代化する計画を提案しました。 USSニミッツは2025年度までに戦闘部隊から外され、ジェラルド・R・フォード級空母が機敏な戦力の艦隊に容易に加えられることを段階的に受け入れる予定です。

この国は、誘導ロケット、弾道ミサイル、武装無人航空機、潜水艦、水上軍艦などの先進兵器に対する軍事パートナーからの需要に応えています。このプログラムでは、Sercoが関連するサブコンポーネントの評価および修理サービスを含む、SubHDRアンテナペデスタルグループ(APG)に修理およびオーバーホールを提供することが求められます。このような誘導およびMROプログラムは、この地域のアクチュエータとバルブの需要を促進し、軍艦に搭載されている他の制御システムとのシームレスな統合を促進および可能にすることを想定しています。

海軍用アクチュエーター・バルブ業界の概要

海軍用アクチュエーター・バルブの市場は、本質的に半統合化されています。市場の著名な企業には、MOOG Inc.、Honeywell International Inc.、Rotork PLC、Emerson Electric Co.、Curtiss-Wright Corporationなどがあります。

いくつかの国で地政学的な不安が増大することによって安全保障環境が新たになり、その結果、先進的な海軍システムに対する需要が高まっています。長期契約を獲得し、世界の存在感を拡大するために、プレイヤーは新しい海軍資産の調達に多額の投資を行っています。

継続的な研究開発により、海軍艦艇に統合されたサブシステムおよびその他の技術の精度と効率の進歩が促進されています。防衛費の高騰に伴い、企業間の競合はさらに激化すると予想されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- アクチュエータの種類

- 機械

- 油圧

- 空気圧

- 電気

- ハイブリッド

- プラットフォーム

- 防衛

- 商業

- 材料

- アルミニウム

- ステンレス鋼

- 合金ベース

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州

- アジア太平洋

- インド

- 中国

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- メキシコ

- ブラジル

- その他ラテンアメリカ

- 中東とアフリカ

- アラブ首長国連邦

- サウジアラビア

- エジプト

- イスラエル

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- MOOG Inc.

- Honeywell International Inc.

- Rotork PLC

- Emerson Electric Co.

- Curtiss-Wright Corporation

- Flowserve Corporation

- IMI PLC

- Diakont

- Schlumberger Limited

- Wartsila Corporation

- AUMA Riester GmbH &Co. KG

- Bosch Rexroth AG(Robert Bosch GmbH)

第7章 市場機会と将来の動向

The Naval Actuators And Valves Market size in terms of Equal-4.64 is expected to grow from USD 3.34 billion in 2024 to USD 4.18 billion by 2029, at a CAGR of 4.64% during the forecast period (2024-2029).

Key Highlights

- The emergence of new technologies, such as high-performance radar and long-distance targeting systems, on the naval warfare front has driven nations to modernize and upgrade their naval capabilities. As actuators and valves form a critical part of all naval vessel subsystems, the induction of new naval vessels may create a parallel demand for actuators and valves to ensure systems performance as per the specifications.

- Stringent regulatory policies are expected to restrain the market's growth during the forecast period. The marine industry is heavily regulated, primarily because of the risks associated with marine activities.

- The increasing popularity of advanced integrated combat systems or the use of naval forces is expected to provide new opportunities for the market, which is anticipated to positively affect the market in focus during the upcoming period.

Naval Actuators And Valves Market Trends

Defense Segment is Expected to Dominate the Market

Due to the profound changes in the international strategic landscape, the configuration of the international security system has been undermined by the growing hegemonism, unilateralism, and power politics that have fueled several ongoing global conflicts. Military powerhouses, such as the United States, the United Kingdom, China, and India, have been focused on augmenting their naval firepower, and several fleet modernization and procurement contracts are underway to address the evolving threats to their national security.

In 2022, the war between Russia and Ukraine further fueled the defense budgets across various countries and the need to reassess the operational readiness of the armed forces globally. The world military expenditure rose by 3.7% in 2022 from the previous year to reach a record high of USD 2.2 trillion. The Russia-Ukraine war was a major driver of the growth in spending in 2022. The five biggest spenders in 2022 were the United States, China, Russia, India, and Saudi Arabia, accounting for 63% of the global military spending.

According to its 30-year shipbuilding plan, the US envisions procuring 55 new ships to achieve an effective fleet size of 314 ships by 2024. In Asia-Pacific, prominent countries such as China and India are also enhancing their naval fleet size and capabilities to achieve technological superiority over their rival countries. Such induction programs are envisioned to drive the demand for actuators and valves in designing and constructing new naval vessels for defense platforms.

North America to Dominate the Market during the Forecast Period

The market is driven by the procurement of advanced weaponry by the US Navy to achieve military dominance in the region, besides ensuring internal peace and security. The United States has invested its vast technological prowess toward the indigenous development of several weapon systems to foster its military prowess over all dominion - land, air, and water.

In the FY2023 budget proposal, the US Navy proposed a total budget request of USD 230.8 billion, including USD 180.5 billion for the Navy and USD 50.3 billion for the Marine Corps. As part of the country's naval expansion projects, the US Navy, in its FY2023 budget, proposed plans to modernize its fleet with the exclusion and inclusion of various warships and carrier fleets in the Navy. The USS Nimitz is to be removed from the battle force by the FY2025, gradually accepting the Gerald R Ford-class carriers to be inducted readily into the fleet of agile force.

The country caters to the demand from its military partners for advanced weaponry, such as guided rockets, ballistic missiles, armed UAVs, submarines, and surface warships. The program entails Serco providing repair and overhauls to the SubHDR Antenna Pedestal Group (APG), including evaluation and repair services to related sub-components. Such induction and MRO programs are envisioned to drive the demand for actuators and valves in the region to facilitate and enable seamless integration with other control systems installed in the fleet of naval vessels.

Naval Actuators And Valves Industry Overview

The naval actuators and valves market is semi-consolidated in nature. Some prominent players in the market include MOOG Inc., Honeywell International Inc., Rotork PLC, Emerson Electric Co., and Curtiss-Wright Corporation.

The emerging security environment, fueled by the growing geopolitical unrest in several countries, is resulting in the growing demand for advanced naval systems. To gain long-term contracts and expand their global presence, players are investing significantly in the procurement of new naval assets.

Continuous R&D has been fostering the advancements of accuracy and efficiency of subsystems and other technologies integrated onboard naval vessels. The competition between the players is expected to increase with the surge in defense expenditure.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Actuator Type

- 5.1.1 Mechanical

- 5.1.2 Hydraulic

- 5.1.3 Pneumatic

- 5.1.4 Electrical

- 5.1.5 Hybrid

- 5.2 Platform

- 5.2.1 Defense

- 5.2.2 Commercial

- 5.3 Material

- 5.3.1 Aluminum

- 5.3.2 Stainless Steel

- 5.3.3 Alloy-based

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Russia

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 Latin America

- 5.4.4.1 Mexico

- 5.4.4.2 Brazil

- 5.4.4.3 Rest of Latin America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Egypt

- 5.4.5.4 Israel

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 MOOG Inc.

- 6.2.2 Honeywell International Inc.

- 6.2.3 Rotork PLC

- 6.2.4 Emerson Electric Co.

- 6.2.5 Curtiss-Wright Corporation

- 6.2.6 Flowserve Corporation

- 6.2.7 IMI PLC

- 6.2.8 Diakont

- 6.2.9 Schlumberger Limited

- 6.2.10 Wartsila Corporation

- 6.2.11 AUMA Riester GmbH & Co. KG

- 6.2.12 Bosch Rexroth AG (Robert Bosch GmbH)