|

市場調査レポート

商品コード

1437610

射撃統制システム:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Fire Control System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 射撃統制システム:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

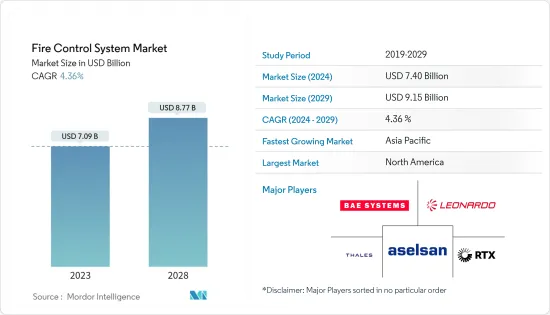

射撃統制システム市場規模は、2024年に74億米ドルと推定され、2029年までに91億5,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に4.36%のCAGRで成長します。

主なハイライト

- 射撃統制システムは、軍事および防衛産業で幅広い用途に使用できます。軍事における精密兵器の需要の高まり、遠隔操作兵器(ROP)ステーションの数の増加、および国防支出の増加により、射撃統制システムの世界市場は急速に成長しています。

- 指向性エネルギー兵器(DEW)の出現は軍事用途に計り知れない可能性を秘めており、攻撃兵器と防御兵器の両方の開発と運用にかかるコストを大幅に削減できる可能性があります。 DEWの広範な採用は、市場力学に根本的な変化を引き起こす可能性があります。

- 抑止力などの技術的な制限やアクティブ保護システムの使用の増加は、システム設計者にとって課題となっています。最新の電子システムはコストが高いため、火災安全基準に準拠する必要性が高まっています。

射撃統制システム市場動向

射撃統制システム市場の空挺プラットフォームセグメントは大幅に成長すると推定されている

射撃統制システムは、戦闘機において空対空任務で目標を正確に攻撃するために重要です。世界中のすべての戦闘機とヘリコプターには射撃統制システムが装備されています。空挺プラットフォームも、さまざまな作戦を実行できる複数任務の戦闘機械をサポートするために開発されました。これらのプラットフォームは、防空、近接航空支援、爆撃、指揮統制、制空権、偵察などのさまざまな任務に利用できます。

2023年9月、米国海軍は、2028年に運用開始予定のデルタ・システム・ソフトウェア構成(DSSC)E-2Dプラットフォームについて、8億4,550万米ドルで米国海軍航空システム司令部(NAVAIR)と契約を締結しました。グラスコックピットのほか、海軍統合射撃管制(NIFC)の一部である協力交戦(CEC)機能や飛行中の給油機能も含まれます。

これらのプラットフォームは、指揮統制、防空、爆撃、制空、近接航空支援、偵察、その他の任務を実行できます。同様に、2023年6月、エアバス・ヘリコプターズはエルビット・システムズに対し、ドイツ空軍のCH-53GS/GE輸送ヘリコプターに空挺電子戦自己防護(AEWS)システムを供給する新たな契約を締結しました。この契約には、ヘリコプターの運用効率とミッションの成功を向上させるためのデジタルレーダー警報受信機(DRW)、電子戦コントローラー(EWC)、および対策分配システム(CMDS)が含まれています。これらの発展は、この部門の成長を促進すると予想されます。

予測期間中に北米が市場を独占する

この地域の主要な防衛主体である米国は、武力戦争の先駆者であり、先進的な兵器システムの調達における着実な成長を通じて自らを軍事的優位の頂点に位置づけています。

戦争の性質の変化は、米国国防総省が軍隊のより優れた武器の装備に向けて支出を増加させている主な理由の1つです。 2023年11月、L3ハリス・テクノロジーズは、米国軍と世界中の同盟軍が戦場で優位に立つことを支援するロケット発射ロケットの射撃統制システムを開発およびアップグレードする契約を獲得しました。それぞれ1億2,400万米ドル相当の契約により、L3ハリスは共通の射撃統制システムを提供できるようになります。

新しい武器は、信頼性の高い動作を保証し、新たに統合された設計変更による性能向上のレベルを推定するために広範なテストを受けます。たとえば、2022年 7月、ゼネラルダイナミクスの事業部門であるゼネラルダイナミクスミッションシステムズは、コロンビア級およびドレッドノート級弾道ミサイルの開発、製造、および設置をサポートするために2億7,990万米ドル相当の米国海軍契約を獲得しました。ミサイル潜水艦。

たとえば、この地域の他の主要軍隊では、2022年 11月にスウェーデンのエイムポイントがカナダ国防総省(DoD)に一連のFCS13-RE射撃統制システム(FCS)およびTH-60サーマルサイトを供給する契約を獲得しました。配備された作戦では、FCS 13-REは、カナダの運用不能なサーブ(サーブM3)84mmカール・グスタフ兵器の主要昼夜制御システム(FCCS)として使用されます。

さらに、精密誘導兵器の配備、研究開発投資の増加、防衛産業における近代化への取り組みへの注目の高まりにより、この地域における射撃統制システムの世界市場はさらに拡大すると思われます。

射撃統制システム業界の概要

この市場は本質的に半統合的であり、特にLeonardo SpA、RTX Corporation、BAE Systems plc.、Rheinmetall AG、ASELSAN AS、THALESなどの大手企業が存在します。市場は競争が激しく、著名なプレーヤーがより大きな市場シェアを目指して競争しています。

防衛分野における厳格な安全性と規制政策により、新規参入企業は制限されることが予想されます。さらに、テクノロジーベースのプラットフォームの売上は、主に、米国やアジア太平洋などの主要市場における経済状況の影響を受けます。したがって、景気低迷期には購入が延期またはキャンセルされ、導入率が比較的遅くなる可能性があり、その結果、市場力学に悪影響を及ぼす可能性があります。

さらに、契約には相殺条項が含まれることが多く、プロジェクトが適時に完了するリスクが高まります。技術的側面に関するリスクが伴うため、活動のスケジュールおよびコストはマクロ経済的要因に基づいて変更される可能性があり、その後、契約の関連当事者の関連利益に影響を及ぼします。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- システム

- 目標獲得・指導体制

- インターフェースシステム

- ナビゲーションシステム

- その他のシステム

- プラットホーム

- 地上波

- 航空写真

- 海軍

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東とアフリカ

- アラブ首長国連邦

- サウジアラビア

- エジプト

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- ASELSAN AS

- BAE Systems plc

- Elbit Systems Ltd.

- General Dynamics Corporation

- Indra Sistemas, SA

- Leonardo SpA

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- RTX Corporation

- Rheinmetall AG

- Saab AB

- Safran SA

- THALES

- Ultra Electronics

第7章 市場機会と将来の動向

The Fire Control System Market size is estimated at USD 7.40 billion in 2024, and is expected to reach USD 9.15 billion by 2029, growing at a CAGR of 4.36% during the forecast period (2024-2029).

Key Highlights

- Fire control systems can be used by the military and defense industry for a wide range of applications. The global market for fire control systems is growing rapidly due to the increasing demand for precision weapons in the military, the increasing number of remotely operated weapon (ROP) stations, and the increase in defense spending.

- The emergence of directed energy weapons (DEW) possesses immense potential for military applications and could dramatically reduce the cost associated with the development and operation of both offensive and defensive weaponry. Widespread adoption of DEWs can trigger a radical change in market dynamics.

- Technological limitations, such as deterrents, and the increasing use of active protection systems pose a challenge to system designers. Due to the high cost of modern electronic systems, the need to comply with fire safety standards has increased.

Fire Control System Market Trends

The Airborne Platform Segment of the Fire Control System Market is Estimated to Grow Significantly

Fire control systems are critical in combat aircraft for accurately hitting targets in air-to-air missions. Every other fighter aircraft and helicopter in the world is outfitted with fire control systems. Airborne platforms have also been developed to support multi-mission warfare machines that can carry out a variety of operations. These platforms can be utilized for a variety of tasks, including air defense, close air support, bombing, command and control, air dominance, and reconnaissance.

In September 2023, the US Navy awarded a contract for USD 845.5 million to the US Naval Air Systems Command (NAVAIR) for a delta system software configuration (DSSC) E-2D platform scheduled to enter service in 2028. The platform is equipped with a glass cockpit, as well as the capability of cooperative engagement (CEC), which is part of the Naval Integrated Fire Control (NIFC) as well as the in-flight refueling capability.

These platforms are capable of command and control, air defense, bombing, air domination, close air support, reconnaissance, and other missions. Similarly, in June 2023, Airbus Helicopters awarded Elbit Systems a new contract to supply Airborne Electronic warfare self-protection (AEWS) systems for German air force CH-53GS/GE transport helicopters. The contract covers Digital Radar Warning Receivers (DRW), Electronic Warfare Controllers (EWC) and Countermeasure Dispensing Systems (CMDS) to improve the helicopter's operational efficiency and mission success. These developments are expected to aid the segment growth.

North America to Dominate the Market During the Forecast Period

The major defense player in the region, the US has been the pioneer of armed warfare and has positioned itself at the apex of military dominance through a steady growth in the procurement of advanced weapon systems.

The changing nature of warfare is one of the prime reasons for the US DoD's increased spending toward arming its armed forces with better weapons. In November 2023, L3Harris Technologies won contracts to develop and upgrade fire control systems for rocket launch vehicles that assist the United States Army and allied forces worldwide in achieving battlefield superiority. The contracts, valued at USD 124 million each, will enable L3Harris to provide a common fire control system.

New weapons are subjected to extensive testing to ensure reliable operation and estimate the level of performance enhancement due to a newly integrated design change. For instance, In July 2022, General Dynamics Mission Systems, a business unit of General Dynamics was awarded a U.S. Navy contract worth USD 279.9 million to support the development, production, and installation of fire control systems for the Columbia- and Dreadnought classes of ballistic missile submarines.

Other major armed forces in the region for instance, in November 2022, Sweden's Aimpoint was awarded a contract to supply the Canada Department of Defence (DoD) with a range of FCS13-RE Fire Control System (FCS) and TH-60 thermal sight .On deployed operations, the FCS 13-RE will be used as the main day and night control system (FCCS) on Canada's in-operable Saab (Saab M3) 84mm Carl Gustav weapons.

In addition, the increased focus on the deployment of precision-guided weapons, increased research and development investments, and modernization initiatives in the defense industry will further expand the global market for fire control systems in the region.

Fire Control System Industry Overview

The market is semi-consolidated in nature with a presence of major players such as Leonardo S.p.A., RTX Corporation and BAE Systems plc., Rheinmetall AG, ASELSAN A.S., and THALES among others. The market is highly competitive, and the prominent players are competing for a larger market share.

The stringent safety and regulatory policies in the defense segment are expected to restrict the entry of new players. Furthermore, the sales of technology-based platforms are primarily influenced by the prevalent economic situations in dominant markets such as the US and Asia-Pacific. Hence, in periods of economic downturn, purchases may be subjected to deferral or cancellation and a relatively slower rate of adoption, which in turn, can adversely affect the market dynamics.

Moreover, the contracts are often subjected to include offset clauses which enhances the risks of timely completion of the project. Since the associated risks regarding the technical aspects, scheduling of activities and costs are subject to change based on macroeconomic factors and subsequently influence the associative profits of the associated parties in a contract.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 System

- 5.1.1 Target Acquisition and Guidance System

- 5.1.2 Interface System

- 5.1.3 Navigation System

- 5.1.4 Other Systems

- 5.2 Platform

- 5.2.1 Terrestrial

- 5.2.2 Aerial

- 5.2.3 Naval

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Egypt

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 ASELSAN A.S.

- 6.2.2 BAE Systems plc

- 6.2.3 Elbit Systems Ltd.

- 6.2.4 General Dynamics Corporation

- 6.2.5 Indra Sistemas, S.A.

- 6.2.6 Leonardo S.p.A.

- 6.2.7 Lockheed Martin Corporation

- 6.2.8 Northrop Grumman Corporation

- 6.2.9 RTX Corporation

- 6.2.10 Rheinmetall AG

- 6.2.11 Saab AB

- 6.2.12 Safran SA

- 6.2.13 THALES

- 6.2.14 Ultra Electronics