|

市場調査レポート

商品コード

1537593

炭化ケイ素:市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Silicon Carbide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 炭化ケイ素:市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年08月14日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

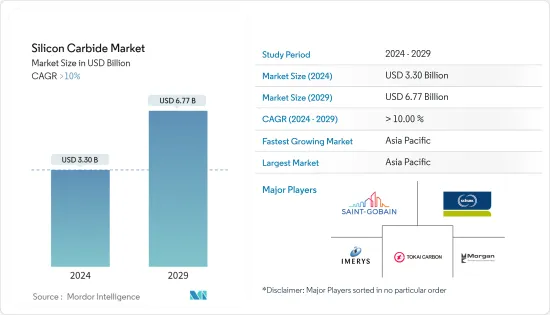

炭化ケイ素市場規模は2024年に33億米ドルと推定され、2029年には67億7,000万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは10%以上で成長する見込みです。

主なハイライト

- 市場を牽引している主な要因は、鉄鋼製造・鉄鋼加工業界の旺盛な需要と、エレクトロニクス業界の急速な需要拡大です。

- 需要を抑制する要因としては、石炭や石油コークスのような原材料コストの変動が挙げられます。さらに、窒化ガリウムのような代替品が入手可能であることも課題となっています。

- 電気自動車の普及率の上昇は、市場の成長にさまざまな機会を提供すると予想されます。

- アジア太平洋地域が世界市場を独占しており、中国、インド、日本などの国々からの消費が最も大きいです。

炭化ケイ素市場の動向

エレクトロニクス・半導体分野での用途拡大

- 炭化ケイ素はケイ素と炭素を含む半導体です。炭化ケイ素の粒を一緒に成形することで、非常に硬いセラミックスを形成することができ、高い耐久性を必要とする用途に使用されます。

- 炭化ケイ素は、高温、高電圧、またはその両方で動作し、フォームファクターが小さいといった特性により、半導体の製造に広く使用されています。

- 世界半導体貿易統計(WSTS)によると、世界半導体市場の売上高は、2023年の5,201億3,000万米ドルを13.12%上回る5,883億6,000万米ドルを記録すると予想されています。この結果、2024年の同セグメントにおける炭化ケイ素の需要は大幅に増加します。半導体は電子機器の最も重要なコンポーネントの1つであるため、予測期間中に市場は大幅な盛り上がりを見せると予想されます。

- 北米、特に米国では、エレクトロニクス産業は緩やかな成長が見込まれています。新しい技術製品への需要の増加が、今後数年間の市場拡大に貢献すると予想されます。

- ドイツの電子産業は欧州最大であり、世界でも第5位です。電気・電子産業はドイツの工業生産全体の11%、国内総生産(GDP)の約3%を占めています。

- 英国は欧州最大のハイエンド家電製品市場であり、英国を拠点とするエレクトロニクス企業は約18,000社にのぼる。

- Canalys社によると、世界のスマートウォッチ市場は、2023年と比較して2024年には金額で17%の成長が見込まれています。電子機器に対する需要の世界の高まりという動向は、予測期間中の市場の成長を促進すると予想されます。

- 炭化ケイ素には上記のような要因があるため、その市場は予測期間中に急成長すると予想されます。

アジア太平洋地域が市場を独占する

- 予測期間中、アジア太平洋地域が炭化ケイ素市場を独占すると予想されます。中国、インド、日本などの国々では、エレクトロニクス、自動車、防衛など様々な分野で高度でアップグレードされた技術に対する需要が増加しているため、炭化ケイ素の需要が増加しています。

- 中国は半導体の主要消費国のひとつであり、半導体生産を拡大しようとしています。半導体は、より付加価値の高い製品の生産を促進することを目的とした政府主導の「メイド・イン・チャイナ2025」計画の主要分野です。中国は2025年までに、使用する半導体の70%を生産することを目指しています。

- 電子情報技術省の報告によると、インドでは毎年2,000個以上の半導体チップが設計されています。半導体の生産が増加することで、将来的に炭化ケイ素市場が促進される可能性があります。

- インド電子・半導体協会(IESA)は、シンガポール半導体産業協会(SSIA)とMoUを締結し、両国の電子・半導体産業間の貿易・技術協力を確立・発展させる。これにより、様々な画期的な半導体製造技術が開発され、インドの半導体製造における炭化ケイ素の消費範囲がさらに拡大することが期待されます。

- インド政府は、電子部品・半導体製造促進スキーム(SPECS)と、生産連動型奨励金(PLI)と並ぶ修正電子機器製造クラスター・スキーム(EMC 2.0)という、インドにおける電子機器製造を促進するための新たなスキームを立ち上げました。PLIスキームによると、政府はメーカーがインドでの生産を増加させた場合、5年間で55億米ドルのインセンティブを提供する可能性があります。これにより、インドのエレクトロニクス生産が促進される可能性が高いです。

- インドの自動車産業は1,000億米ドル以上の価値があり、輸出総額の8%を占め、インドのGDPの2.3%を占めています。2025年には世界第3位になると予想されています。

- 2024年3月、中国は国防予算を7.2%増の約2,330億米ドルにすると発表しました。同国の最近の計画は、2027年までに米国並みの完全な近代軍を構築することです。中国はここ数年、空母やステルス機に投資しています。さらに、北京の裏庭である南シナ海(SCS)を含め、世界中で空母の数を約5~6隻に増やす計画です。

- 上記の要因は、政府の支援と相まって、予測期間中の同地域の需要増加に寄与しています。

炭化ケイ素産業の概要

炭化ケイ素市場は部分的に統合されており、企業が大きな市場シェアを占めています。主な市場企業(順不同)には、Saint-Gobain、Imerys、Tokai Carbon、Schunk Ingenieurkeramik GmbH、Morgan Advanced Materialsなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- エレクトロニクス産業からの旺盛な需要

- アドバンストセラミックス需要の増加

- 抑制要因

- 原材料コストの変動

- 窒化ガリウムなどの代替品の入手可能性

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 製品別

- グリーンSiC

- ブラックSiC

- その他の製品

- 用途別

- 鉄鋼

- エネルギー

- 自動車

- 航空宇宙・防衛

- エレクトロニクス・半導体

- その他の用途

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- ロシア

- トルコ

- スペイン

- ノルディック

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- カタール

- ナイジェリア

- アラブ首長国連邦

- エジプト

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Blasch Precision Ceramics Inc.

- Christy Refractories

- Imerys

- Keith Company

- Morgan Advanced Materials

- NGK Insulators Ltd

- Silcarb Recrystallized Private Limited

- Saint Gobain

- Termo Refractaires

- The Pottery Supply House

- Fiven ASA

- KEYVEST

- Navarro SiC

- Schunk Ingenieurkeramik GmbH

- Superior Graphite

- Tateho Chemical Industries Co. Ltd

- ESD-SIC BV

- ELSID SA

- Zaporozhsky Abrasinvy Combinat

第7章 市場機会と今後の動向

- 電気自動車と自動運転車の普及拡大

- ナノテクノロジーの利用拡大

目次

Product Code: 68929

The Silicon Carbide Market size is estimated at USD 3.30 billion in 2024, and is expected to reach USD 6.77 billion by 2029, growing at a CAGR of greater than 10% during the forecast period (2024-2029).

Key Highlights

- The major factors driving the market studied are strong demand from the steel manufacturing and steel processing industry and rapidly growing demand from the electronics industry.

- Some factors restraining the demand for the market include fluctuating costs of raw materials like coal and petroleum coke. Moreover, the availability of substitutes such as gallium nitride might also cause challenges.

- The rising penetration of electric vehicles is expected to offer various opportunities for the growth of the market.

- Asia-Pacific dominated the market globally, with the most significant consumption from countries such as China, India, and Japan.

Silicon Carbide Market Trends

Increasing Usage in Electronics and Semiconductor Segment

- Silicon carbide is a semiconductor containing silicon and carbon. Grains of silicon carbide can be molded together to form very hard ceramics that are used in applications requiring high endurance.

- Silicon carbide is widely used in manufacturing semiconductors due to its properties, like the ability to work at high temperature, high voltage, or both, and reduced form factor.

- According to the World Semiconductor Trade Statistics (WSTS), the revenue of the global semiconductor market is expected to register USD 588.36 billion, 13.12% higher than USD 520.13 billion in 2023. This will result in a substantial boost in the demand for silicon carbide in the segment in 2024. As semiconductors are one of the most crucial components of electronic devices, the market is expected to witness a substantial boost during the forecast period.

- In North America, especially in the United States, the electronics industry is expected to grow at a moderate rate. An increase in the demand for new technological products is expected to help the market expansion in the coming years.

- The German electronic industry is Europe's biggest and the fifth-largest, globally. The electrical and electronics industry accounted for 11% of the total German industrial production and about 3% of the country's gross domestic product (GDP).

- The United Kingdom is the largest European market for high-end consumer electronics products, with about 18,000 UK-based electronics companies in the market.

- According to Canalys, the global smartwatch market is expected to grow by 17% in value in 2024 compared to 2023. This trend of globally increasing demand for electronics is expected to propel the market's growth during the forecast period.

- Due to all the factors mentioned above for silicon carbide, its market is expected to grow rapidly during the forecast period.

Asia-Pacific to Dominate the Market

- Asia-Pacific is expected to dominate the market for silicon carbide during the forecast period. In countries like China, India, and Japan, due to the increasing demand for advanced and upgraded technology across various sectors, including electronics, automotive, and defense, the demand for silicon carbide has been increasing in the region.

- China is one of the major consumers of semiconductors, and it is trying to ramp up semiconductor production. Semiconductors are a key area of the Made in China 2025 plan, a government initiative that aims to boost the production of higher-value products. China is aiming to produce 70% of the semiconductors it uses by 2025.

- According to reports from the Department of Electronics and Information Technology, over 2,000 semiconductor chips are designed in India every year. The increasing production of semiconductors may propel the silicon carbide market in the future.

- The India Electronics and Semiconductor Association (IESA) signed an MoU with the Singapore Semiconductor Industry Association (SSIA) to establish and develop trade and technical cooperation between the electronics and semiconductor industries of both countries. This is expected to result in the development of various breakthrough semiconductor manufacturing technologies that may further increase the scope for the consumption of silicon carbide in semiconductor manufacturing in India.

- The government launched new schemes to promote electronics production in India: the Scheme for Promotion of Manufacturing of Electronic Components and Semiconductors (SPECS) and the Scheme for Modified Electronics Manufacturing Clusters (EMC 2.0) alongside the Production Linked Incentive (PLI). According to the PLI scheme, the government is likely to offer incentives as manufacturers increase production in India, with USD 5.5 billion available over five years. This is likely to boost the country's production of electronics.

- The Indian automotive industry is worth more than USD 100 billion, contributes 8% of the country's total exports, and accounts for 2.3% of the Indian GDP. It is expected to become the third-largest in the world by 2025.

- In March 2024, China announced a 7.2% increase in its defense budget to about USD 233 billion. The country's recent plans are to build a fully modern military on par with the United States by 2027. The country has been investing in aircraft carriers and stealth aircraft in the past few years. Moreover, it plans to increase the number of aircraft carriers to about five to six worldwide, including Beijing's backyard, the South China Sea (SCS).

- The factors mentioned above, coupled with government support, contribute to the increasing demand in the region during the forecast period.

Silicon Carbide Industry Overview

The silicon carbide market is partially consolidated, with players accounting for a significant market share. Some key market players (not in any particular order) include Saint-Gobain, Imerys, Tokai Carbon Co. Ltd, Schunk Ingenieurkeramik GmbH, and Morgan Advanced Materials.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Strong Demand from the Electronics Industry

- 4.1.2 Increasing Demand for Advanced Ceramics

- 4.2 Restraints

- 4.2.1 Fluctuating Costs of Raw Materials

- 4.2.2 Availability of Substitutes such as Gallium Nitride

- 4.3 Industry Value Chain Analysis

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Product

- 5.1.1 Green SiC

- 5.1.2 Black SiC

- 5.1.3 Other Products

- 5.2 By Application

- 5.2.1 Steel Manufacturing

- 5.2.2 Energy

- 5.2.3 Automotive

- 5.2.4 Aerospace and Defense

- 5.2.5 Electronics and Semiconductor

- 5.2.6 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Turkey

- 5.3.3.7 Spain

- 5.3.3.8 NORDIC

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Qatar

- 5.3.5.4 Nigeria

- 5.3.5.5 United Arab Emirates

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Blasch Precision Ceramics Inc.

- 6.4.2 Christy Refractories

- 6.4.3 Imerys

- 6.4.4 Keith Company

- 6.4.5 Morgan Advanced Materials

- 6.4.6 NGK Insulators Ltd

- 6.4.7 Silcarb Recrystallized Private Limited

- 6.4.8 Saint Gobain

- 6.4.9 Termo Refractaires

- 6.4.10 The Pottery Supply House

- 6.4.11 Fiven ASA

- 6.4.12 KEYVEST

- 6.4.13 Navarro SiC

- 6.4.14 Schunk Ingenieurkeramik GmbH

- 6.4.15 Superior Graphite

- 6.4.16 Tateho Chemical Industries Co. Ltd

- 6.4.17 ESD-SIC BV

- 6.4.18 ELSID SA

- 6.4.19 Zaporozhsky Abrasinvy Combinat

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increase Market Penetration of Electric Cars and Self-driving Cars

- 7.2 Growth of Usage in Nanotechnology