|

市場調査レポート

商品コード

1687384

砲兵システム- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Artillery Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 砲兵システム- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

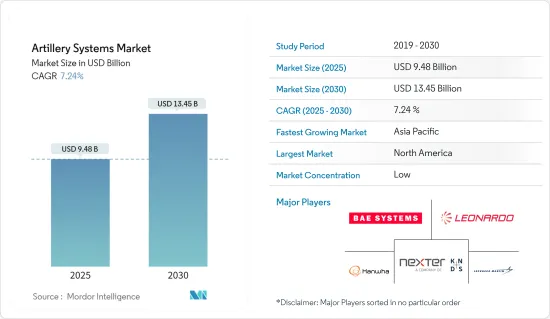

砲兵システム市場規模は2025年に94億8,000万米ドルと推定され、予測期間(2025年~2030年)のCAGRは7.24%で、2030年には134億5,000万米ドルに達すると予測されます。

主なハイライト

- COVID-19パンデミックは2つの重要な点で市場に影響を与えました。第一に、世界のサプライチェーンと製造施設の混乱により、砲兵システムの生産と納入に遅れが生じ、各国の調達スケジュールに影響が出た可能性があります。第二に、各国政府がパンデミックの当面の課題に対処するために多大な資源を割り当てているため、国防予算が再配分されたり、制約を受けたりした可能性があり、新しい砲兵システムへの投資に影響を及ぼす可能性があります。

- 新興諸国の軍事費の増加は、新型・先進砲兵システムの開発投資を後押ししています。洗練された大砲を開発するための兵器近代化プログラムの開始は、より新しい世代の大砲の採用を強化し、したがって、今後数年間の市場の見通しを強化すると予想されます。地域紛争と地政学的緊張の激化により、精密な攻撃と迅速な対応が可能な高性能砲兵システムへの需要が高まっています。また、戦争の性質が変化し、巻き添え被害を最小限に抑えながら友軍を支援するための高精度武器・弾薬に対する需要が高まっていることも、砲兵システム市場の需要を高めています。

砲兵システム市場の動向

砲兵システム市場の成長を支える国防費の増加

- 国際戦略情勢の大きな変化により、国際安全保障システムの構成は、覇権主義、一国主義、パワーポリティクスの高まりによって損なわれ、現在進行中のいくつかの世界紛争に拍車をかけています。中東におけるサウジアラビアとイランの冷戦のように、多くの国々の間に存在する領土権の不確実性は、地政学的な情勢を乱す大きな原因のひとつです。

- この点で、各国政府の最も一般的な反応は、自国の安全保障を向上させるために軍事費を増やすことです。米国、英国、中国、インドなどの軍事大国は、軍事火力と戦争能力の増強に注力してきました。既存の防衛システムの戦闘即応性を確保するため、軍隊が使用する兵器システムを近代化するための開発・調達計画が現在進行中です。また、国産化を同時に推進することで、こうしたシステムの現地開発を進めている国もあります。現在、国防予算の増加がこれらのプログラムを支えています。

- ウクライナ侵攻は、中欧・西欧の軍事費決定に直ちに影響を与えました。これには、複数の政府による複数年にわたる支出増計画が含まれていました。世界の軍事費は2022年に8年連続で増加し、史上最高の2兆2,400億米ドルとなりました。支出が最も急増したのは欧州で(13%増)、ロシアとウクライナの支出が大部分を占めました。しかし、ウクライナへの軍事援助やロシアの脅威の高まりに対する懸念は、東アジアの緊張と同様に、他の多くの国の支出決定に強い影響を与えました。

- 米国は依然として世界最大の軍事支出国です。米国の軍事費は2022年に8,770億米ドルに達し、これは世界の軍事費全体の39%を占め、世界第2位の中国の軍事費の3倍に相当します。

- 各国が軍事近代化のために多額の投資を行っていることが、予測期間中の砲兵システム市場の成長を支える可能性があります。各国は、戦場での戦術的優位性を獲得するため、長距離射撃能力の開発に注力しています。長距離精密射撃能力を開発するために、米国のような国々は砲兵システムの調達を開始しています。

- 例えば、2022年12月、リトアニア国防省はフランスのネクスター・グループとシーザー砲18門の購入契約を締結しました。

予測期間中、アジア太平洋が最も高いCAGRで推移する見込み

- アジア太平洋は予測期間中に高いCAGRで推移すると予想されます。この地域の国家間の緊張の高まりが、軍隊の急速な近代化を促しています。中国、インド、オーストラリア、日本、韓国のような国々は、砲兵システムの開発、建設、調達に大きく投資しています。

- 例えば、2022年11月、Kalyani Strategic Systems Limited(インド)は、非紛争地域の友好国に155mm砲を輸出する契約を締結しました。この契約は1億5,500万米ドル相当で、武器は2025年までに輸出されることになっています。カルヤニ・グループは、インドに世界最大の大砲工場を設立するとも伝えられています。2023年5月、中国の人民解放軍戦略支援軍(PLA-SSF)はPLA-SSF西北核技術研究所(NINT)に203ミリ砲を生産する契約を与えました。

砲兵システム産業概要

砲兵システム市場は細分化されており、多くの世界企業やローカル企業が価格競争や技術革新を通じて市場の成長に大きく貢献しています。砲兵システム市場の主要企業には、BAE Systems plc、Lockheed Martin Corporation、Hanwha Group、Leonardo S.p.A、Elbit Systems Ltd.、Nexter Groupなどがあります。各社は市場シェアを拡大するため、主に砲兵システム・ポートフォリオの機能強化に注力しています。

海外の企業は、数十億の長期契約を獲得するために、地元の企業と競争しています。また、顧客基盤を拡大し、技術的専門知識を共有するために、地元企業と提携している企業もあります。東欧、中東、アジア太平洋の緊張が新型砲兵システムの需要を生み出しています。老朽化したシステムを新型砲兵システムに置き換えることで、陸上戦力強化のための空白を埋めようとしている米国でも需要が高まっています。また、過去10年間における海軍力強化への関心の高まりは、フリゲート、コルベット、航空母艦、駆逐艦、海洋艦艇の大幅な新規発注をもたらし、それによって新型砲の必要性が生じています。

例えば、2023年5月、エルビット・システムズは、イスラエル国防省とオランダ国防省間の合意の一環として、オランダ王立陸軍にPULS(Precise &Universal Launching System)砲兵ロケットシステムを供給する3億500万米ドル相当の契約を獲得したと発表しました。

同様に、2022年11月、JPEO A&AとACC-ロックアイランドは、テキサス州に155mm砲金属部品生産ラインを新設するため、ジェネラル・ダイナミクス・オードナンス・アンド・タクティカル・システムズ社に新たなタスクオーダーを発注しました。このラインでは、より高い機械速度とより正確で均一な製品により、柔軟で費用対効果の高い精密な金属成形を実現するフリーフロー成形技術が活用されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- 榴弾砲

- 迫撃砲

- 対空砲

- ロケット砲

- その他のタイプ(海軍および沿岸砲兵)

- 射程距離

- 短距離(5~30キロ)

- 中距離(31~60キロ)

- 長距離(60キロメートル以上)

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- その他のラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- イスラエル

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- BAE Systems plc

- Hanwha Group

- Elbit Systems Ltd.

- Rostec

- Lockheed Martin Corporation

- Avibras Industria Aeroespacial SA

- Nexter Group

- Denel SOC Ltd

- Leonardo S.p.A

- Singapore Technologies Engineering Ltd

- RUAG Group

- Norinco International Cooperation Ltd.

- THALES

- Rheinmetall AG

第7章 市場機会と今後の動向

The Artillery Systems Market size is estimated at USD 9.48 billion in 2025, and is expected to reach USD 13.45 billion by 2030, at a CAGR of 7.24% during the forecast period (2025-2030).

Key Highlights

- The COVID-19 pandemic affected the market in two key ways. Firstly, disruptions in global supply chains and manufacturing facilities may have caused delays in the production and delivery of artillery systems, impacting procurement timelines for various countries. Secondly, with governments allocating significant resources to address the pandemic's immediate challenges, defense budgets might have been reallocated or constrained, potentially affecting investments in new artillery systems.

- The increasing military spending of emerging countries is helping them to invest in the development of new and advanced artillery systems. The initiation of weapon modernization programs to develop sophisticated artillery is anticipated to bolster the adoption of newer generation artillery, thus bolstering the market prospects in the coming years. Escalating regional conflicts and geopolitical tensions have led to a growing demand for sophisticated artillery systems capable of precision strikes and quick response times. Also, the changing nature of warfare and the growing demand for high-precision arms and ammunition to support friendly troops while minimizing collateral damage has bolstered the demand for the artillery systems market.

Artillery Systems Market Trends

Increasing Defense Expenditure Supporting the Growth of the Artillery Systems Market

- On account of the profound changes in the international strategic landscape, the configuration of the international security system has been undermined by the growing hegemonism, unilateralism, and power politics that have fueled several ongoing global conflicts. Uncertainties in territorial rights between many countries, like the Saudi-Iran cold war in the Middle East, are among the major causes disturbing the geopolitical climate.

- The most common reaction of governments, in this regard, is to increase military spending to improve security in their respective countries. Military powerhouses, such as the United States, the United Kingdom, China, and India, have been focused on augmenting their military firepower and warfare capabilities. To ensure combat readiness of existing defense systems, development and procurement programs are currently underway to modernize the weapon systems used by the armed forces. A simultaneous push for indigenization is also driving several countries' local development of such systems. The increase in defense budgets currently supports these programs.

- The invasion of Ukraine had an immediate impact on military spending decisions in Central and Western Europe. This included multi-year plans to boost spending from several governments. World military spending grew for the eighth consecutive year in 2022 to an all-time high of USD 2240 billion. By far, the sharpest rise in spending (+13 percent) was seen in Europe and was largely accounted for by Russian and Ukrainian spending. However, military aid to Ukraine and concerns about a heightened threat from Russia strongly influenced many other states' spending decisions, as did tensions in East Asia.

- The United States remains by far the world's biggest military spender. US military spending reached USD 877 billion in 2022, which was 39 percent of total global military spending and three times more than the amount spent by China, the world's second-largest spender.

- Countries' significant investments to modernize their military may support the artillery systems market growth during the forecast period. Countries are focused on developing long-range fire capabilities to achieve a tactical advantage on the battlefield. To develop long-range precision fire capabilities, countries like the United States are initiating the procurement of artillery systems.

- For instance, in December 2022, Lithuania's Defense Ministry signed a contract with the French group Nexter for the purchase of 18 Caesar artillery guns.

Asia-Pacific is Expected to Witness the Highest CAGR During the forecast period

- Asia-Pacific is expected to register a high CAGR during the forecast period. The escalated tensions between the countries in this region have encouraged the rapid modernization of the armed forces. Countries like China, India, Australia, Japan, and South Korea are significantly investing in the development, building, and procurement of artillery systems.

- For instance, in November 2022, Kalyani Strategic Systems Limited (India) signed a deal to export 155mm artillery guns to a friendly nation in a non-conflict zone. The deal is worth USD 155 million, and the arms are to be exported by 2025. The Kalyani Group is also reported to establish the world's largest artillery factory in India. In May 2023, The People's Liberation Army-Strategic Support Force (PLA-SSF) of China gave a contract to PLA-SSF Northwest Institute of Nuclear Technology (NINT) to produce 203-millimeter artillery guns.

Artillery Systems Industry Overview

The artillery systems market is fragmented, with many global and local players contributing significantly to the growth of the market through competitive pricing and innovation. Some of the major companies in the artillery systems market include BAE Systems plc, Lockheed Martin Corporation, Hanwha Group, Leonardo S.p.A, Elbit Systems Ltd., and Nexter Group. The companies are mainly focusing on enhancing the capabilities of their artillery systems portfolio to increase their market share.

Foreign players are competing with local players to gain multi-billion long-term contracts. Some players have also partnered with local companies to expand their customer base and share technical expertise. Tensions across Eastern Europe, the Middle East, and Asia-Pacific are generating the demand for new artillery systems. The demand is also higher in the US, which is trying to fill in the gaps to strengthen its land forces by replacing the aging systems with new artillery systems. Also, a growing focus on strengthening naval capabilities over the past decade has resulted in significant new orders for frigates, corvettes, aircraft carriers, destroyers, and offshore vessels, thereby generating the need for new artillery guns.

For instance, in May 2023, Elbit Systems announced that as part of an agreement between the Israeli Ministry of Defense and the Netherlands Ministry of Defense, it was awarded a contract worth USD 305 million to supply Precise & Universal Launching System (PULS) artillery rocket systems to the Royal Netherlands Army.

Likewise, In November 2022, JPEO A&A and ACC-Rock Island awarded a new task order to General Dynamics Ordnance and Tactical Systems to build a new 155 mm artillery metal parts production line in Texas that will utilize free-flow forming technology, which delivers flexible, cost-effective, and precise metal forming with higher machine speeds and more accurate, uniform products.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size and Forecast by Value - USD billion, 2018 - 2031)

- 5.1 Type

- 5.1.1 Howitzer

- 5.1.2 Mortar

- 5.1.3 Anti-air Artillery

- 5.1.4 Rocket Artillery

- 5.1.5 Other Types (Naval and Coastal Artillery)

- 5.2 Range

- 5.2.1 Short Range (5-30 kilometers)

- 5.2.2 Medium Range (31-60 kilometers)

- 5.2.3 Long Range (Above 60 kilometers)

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Mexico

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Israel

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 BAE Systems plc

- 6.2.2 Hanwha Group

- 6.2.3 Elbit Systems Ltd.

- 6.2.4 Rostec

- 6.2.5 Lockheed Martin Corporation

- 6.2.6 Avibras Industria Aeroespacial SA

- 6.2.7 Nexter Group

- 6.2.8 Denel SOC Ltd

- 6.2.9 Leonardo S.p.A

- 6.2.10 Singapore Technologies Engineering Ltd

- 6.2.11 RUAG Group

- 6.2.12 Norinco International Cooperation Ltd.

- 6.2.13 THALES

- 6.2.14 Rheinmetall AG