|

市場調査レポート

商品コード

1690129

債権回収ソフトウェア:市場シェア分析、産業動向、成長予測(2025年~2030年)Debt Collection Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 債権回収ソフトウェア:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 183 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

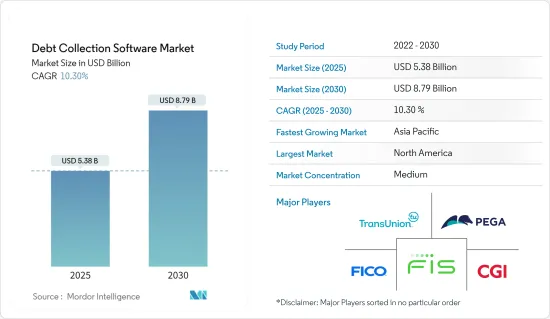

債権回収ソフトウェア市場規模は2025年に53億8,000万米ドルと推計され、予測期間(2025年~2030年)のCAGRは10.3%で、2030年には87億9,000万米ドルに達すると予測されます。

主なハイライト

- 市場成長の主な要因は、AIとMLの統合による顧客体験のパーソナライズ化、消費者の需要に応えるための継続的イノベーション、自動化による債務不履行確率の予測、専門の債権回収会社への債権回収のアウトソーシングなど、債権回収プロセスにおける自動化の進展にあります。

- テクノロジーを駆使した銀行手法の最も大きな受益者は、デジタル融資市場です。データ駆動型テクノロジー、機械学習、その他のコミットメントは、従来の書類作成や手続きからデジタル・レンディングを進化させる重要な要素です。P2P融資、中小企業向け融資、短期融資、クレジットカードなどのモデルがデジタル融資市場を生み出しています。

- 企業は大量の顧客データを利用できるため、顧客に的を絞って融資を行うことができ、これがデジタル融資分野の最も重要な成長要因のひとつとなっています。さらに、決済や金融サービスといったフィンテック分野の他のビジネスモデルと比べ、デジタル・レンディングは利幅が大きいです。

- 与信需要の高まり、金融に関する意識の高まり、手続きがスムーズに進むことへの期待から、デジタル化は銀行にとって必要不可欠なものとなっています。デジタル・レンディングの成長は、債権回収ソフトウェアで効率的に使用できる重要な債務者データやその他のデータを生み出すと分析されています。回収プロセスを自動化する現実的なソリューションは、貸金業者が債務者を効率的に追跡・フォローアップし、債権回収の予測と優先順位付けを行い、より迅速な回収を可能にする債権回収ソフトウェアや回収CRMを使用することです。これが予測期間中の市場成長率を押し上げると分析されています。

- 債権回収活動の管理は、時代遅れの技術、制限された機能、融通の利かないアーキテクチャで表現されるレガシーシステムによって著しく妨げられてきました。このような制限により、債権回収ソフトウェア市場は、進化する複雑な債権管理に対応できる、現代的で機敏かつ適応性の高いソリューションへの需要が急増しています。

- 債権回収ソフトウェアは、COVID-19の大流行によって変貌を遂げました。なぜなら、貸金業者は新しいリスク技術やリスク評価指標を含む最新のリスク手順に適応しなければならないからです。AI技術を利用して様々なリスクソリューションを統一し、全体的な導入プロセスを強化する必要性が、パンデミック後の市場成長を高めています。

債権回収ソフトウェア市場動向

金融機関(銀行とNBFC)が成長する

- 先進技術や分析ベースの債権回収ソフトウェアを通じて回収業務をデジタル化することで、銀行の貸し倒れリスクを軽減するために、金融機関全体で債権回収ソフトウェアを開発することが、金融機関の全体的な収益と収益性の開拓を支援し、市場の成長を後押ししています。

- さらに、不良債権を減らすことを優先する銀行セクターの動向により、金融機関は借り手の返済能力を把握して延滞の多い地域と少ない地域を特定するようになり、より良い回収効率を実現するために金融セクターの回収プロセスを合理化・自動化する延滞管理プラットフォームの機能により、債権回収ソフトウェア市場を牽引しています。

- クラウドベースの債権管理ソフトウェアは、その拡張性と、債権回収パターンを分析するためのBFSI部門のオンプレミスおよびクラウドホストのデータシートを統合する互換性により、市場の成長を後押ししています。金融機関における回収機能のバックエンドアプリケーションでは、融資の回収戦略を設計する際の信頼性と精度を高めるために、クラウド技術、高度な分析、人工知能(AI)、機械学習(ML)技術、すぐに利用できるアプリケーションプログラミングインターフェース(API)の利用が進んでおり、市場の成長を後押ししています。

- ペガシステムズやテメノスAGなどの市場ベンダーは、債権回収を管理するために、デジタル回収、債権分析、訴訟管理、AI主導のインテリジェントオートメーションと機械学習モデルを搭載した回収モバイルアプリを含む債権解決ソリューションの包括的なスイートを導入しており、市場で入手可能な完全な債権回収ソリューションを通じて、ユーザーはより良い回収効率のためにこれらのソリューションを容易に導入できるため、BFSIにおける債権回収ソフトウェアの採用を促進しています。

- 例えば、セキュア・トラスト銀行は2023年6月、EXUS Softwareと提携し、データ主導のゼロ・カスタマイズ・アプローチによって同行の回収業務を最適化しました。同行は、この単一プラットフォームを利用して、業務プロセスの複雑性を軽減し、顧客とのあらゆるコミュニケーションを合理化し、回収プロセスにおける完全なカスタマージャーニーを完全に可視化することを計画しており、BFSIセクターの市場成長を促進することが期待されています。

- 世界銀行の報告書によると、中低所得国の民間部門に対する国内与信は大幅に増加し、2022年度にはGDPを超えました。

アジア太平洋は大幅な成長が見込まれる

- 中国における債権回収の状況は、債権回収の効率性とコンプライアンスを向上させる新しいテクノロジー主導のアプローチにより、ここ数年で著しい変貌を遂げています。さらに、不良債権の増加やエンドユーザー業界における債権回収プロセスの自動化ニーズの高まりを踏まえて、予測期間における市場の成長を分析します。

- 中国における債権回収ソフトウェア市場の成長は、不良債権を最小限に抑え、高度な技術をベースとしたソフトウェアによって債権回収を自動化したいというエンドユーザー業界の需要が高まっていることが大きな要因となっています。同国の金融市場が成長と適応を続ける中、革新的な債権回収ソリューションを提供するベンダーは、エンドユーザー業界の効率的でコンプライアンスに準拠した安全な債権回収プロセスを確保する上で、大きな牽引力を獲得し続けると思われます。

- インドでは近年、債権回収ソフトウェア市場が大きく成長しています。世界市場ベンダーの存在感の大きさ、新たな債権回収ソフトウェアプラットフォームの出現、不良債権の増加、債権回収業務の技術的進歩などにより、今後も成長が見込まれます。現在の経済情勢に伴う課題、特に様々なチャネルでの債権回収管理は、銀行やNBFCの業務非効率や経費増につながり、債権回収ソフトウェアの導入が必要となっています。

- インドの債権回収業界は、パンデミック後に急速にテクノロジーを導入し、大きな勢いを見せています。クレジット需要の高まり、消費者の嗜好の進化、シームレスな体験への期待から、貸金業者は債権回収業務を自動化するためにデジタル化を採用せざるを得なくなりました。これにより、貸金業者における債権回収ソフトウェアの導入が促進され、貸金業者が時間、コスト、リソース、評判を節約すると同時に、顧客体験と顧客維持率を向上させることが期待されます。

- オーストラリア、日本、韓国、ニュージーランドを含むその他アジア太平洋は、予測期間中に債権回収ソフトウェア市場で大きな成長を記録すると予想されます。この成長の背景には、デジタル化の進展と、銀行、債権回収会社、電気通信、政府などのエンドユーザー業界における債権回収の自動化ニーズがあります。不良債権を最小化する必要性の高まりと、地域および世界市場ベンダーの存在感が、この成長をさらに後押ししています。

債権回収ソフトウェア産業の概要

債権回収ソフトウェア市場は、半固定的な様相を呈しており、この地域におけるサプライヤーの存在が大きいため、浸透度は中程度です。これらの企業は、先進的なソリューションを導入するために様々なデジタル技術の新興企業との提携を進めています。この市場の注目すべき企業としては、フィデリティ・ナショナル・インフォメーション・サービシズ(FIS)、CGI Inc.、フェア・アイザック・アンド・カンパニー(FICO)(コンステレーション・ソフトウェアInc.)、トランスユニオンLLC、ペガシステムズInc.などが挙げられます。

- 2024年6月リカーリング・コマースを専門とする先進的な決済企業Acquired.comと、英国の著名な回収テクノロジー・プロバイダであるFlexysは、両社の提携を誇らしげに発表しました。Acquired.comの主な目標は、Flexysのような企業に最先端の決済ツールを提供し、決済プロセスを合理化・強化することです。今回の提携により、Flexysはソリューションをシームレスに統合し、顧客の支払い体験を向上させることができました。

- 2024年3月売掛金向けの会話型AIソリューションで著名なSkit.aiは、最先端のセルフサービス製品群を発表しました。これらは債権回収を合理化するだけでなく、消費者とのやり取りを豊かにするよう設計されています。Skit.aiの最新サービスは、音声、チャット、電子メール、テキスト・チャネルにまたがるジェネレーティブAI技術を活用しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査想定と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の債権回収ソフトウェア市場への影響評価

第5章 市場力学

- 市場促進要因

- 債権回収プロセスの自動化の進展

- 専門の債権回収会社への債権回収のアウトソーシング

- 市場抑制要因

- レガシーシステムの不備

第6章 市場セグメンテーション

- 展開別

- クラウドベース

- オンプレミス

- 組織規模別

- 大企業

- 中小企業

- エンドユーザー別

- 金融機関(銀行およびNBFC)

- 回収業者

- ヘルスケア

- 政府機関

- 電気通信および公益事業

- その他エンドユーザー(不動産、小売)

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- インド

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- コロンビア

- その他のラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Fidelity National Information Services Inc.(FIS)

- CGI Inc.

- Fair, Isaac and Company(FICO)(Constellation Software Inc.)

- TransUnion LLC

- Pegasystems Inc.

- Temenos AG

- Intellect Design Arena Limited

- Nucleus Software Exports Limited

- Chetu Inc.

- AMEYO(Exotel Techcom Pvt. Ltd)

- EXUS Ltd

- KuhleKT Pty Ltd

第8章 投資分析

第9章 市場の将来

The Debt Collection Software Market size is estimated at USD 5.38 billion in 2025, and is expected to reach USD 8.79 billion by 2030, at a CAGR of 10.3% during the forecast period (2025-2030).

Key Highlights

- The growth of the market is majorly attributed to the increasing automation in the debt collection process, such as personalizing customer experience through the integration of AI and ML, Continuous innovations to meet consumer demand, predicting default probability through automation, and outsourcing debt recovery to specialized debt collection agencies.

- The most significant beneficiary of the technology-based banking method has been the digital lending market. Data-driven technology, machine learning, and other commitments are critical elements in the evolution of digital lending from traditional paperwork and formalities. Models such as P2P lending, SME financing, short-term loans, and credit cards generate a digital loan market.

- Companies can target their loans to customers due to the availability of large amounts of customer data, one of the most significant growth drivers in the digital lending sector. Further, compared to other business models in the field of fintechs, such as payments and finance services, digital lending offers greater margins.

- Digitization has become a necessity for banks in view of the growing demand for credit, increased awareness of financial matters, and an expectation that the process will go smoothly. The growth of digital lending is analyzed to create significant borrower data and other data that could be used efficiently in the debt collection software. A practical solution to automating the collection process is using debt collection software or collections CRM that allows lenders to track and follow up with debtors efficiently, predict and prioritize debt recovery, and enable faster collections. This is analyzed to boost the market's growth rate during the forecast period.

- The management of debt collection activities has been significantly hindered by legacy systems, which can be described by out-of-date technology, restricted functionality, and inflexible architecture. These limitations have driven the debt collection software market to witness a surge in demand for modern, agile, and adaptable solutions capable of addressing the evolving complexities of debt management.

- Debt collection software has transformed due to the COVID-19 pandemic because lenders must adapt to the latest risk procedures, including new risk technology and risk-evaluation indicators. The need to unify various risk solutions by using AI technologies and enhance overall implementation processes has enhanced market growth post-pandemic.

Debt Collection Software Market Trends

Financial Institutions (Banks and NBFC) to Witness Growth

- Implementing debt collection software across financial institutions to reduce the banks' risk for loan defaulters by digitizing the collection operation through advanced technology and analytics-based debt collection software is fueling the market's growth by supporting the development of lenders' overall revenue and profitability.

- Additionally, the trend of banking sector priorities in lowering the NPAs has led financial organizations to understand the repayment capacity of a borrower to locate areas for high and low delinquencies, driving the market of debt collection software due to their feature of delinquency management platforms to streamline and automate the collection process in the financial sector for better collection efficiencies.

- The deployment of cloud-based debt management software due to its scalability and compatibility in integrating BFSI sectors' on-premise and cloud-hosted data sheets for analyzing debt collection patterns drives the market's growth. The back-end applications in the collections function in financial institutions are increasingly using cloud technologies, advanced analytics, artificial intelligence (AI), machine learning (ML) techniques, and ready-to-consume application programming interfaces (APIs) for better reliability and accuracy in designing collection strategy for the loans, fueling the growth of the market.

- Market vendors, such as Pegasystems and Temenos AG, are introducing a comprehensive suite of debt resolution solutions, including digital collections, debt analytics, litigation management, and a collection mobile app powered by AI-driven intelligent automation and machine learning models to manage debt collections, which is fueling the adoption of the debt collection software in the BFSIs because, through complete collection solutions available in the market, users can easily implement those solutions for better recovery efficiencies.

- For instance, in June 2023, Secure Trust Bank partnered with EXUS Software to optimize the bank's collections operations through a data-driven, zero-customization approach. The bank has planned to use this single platform to reduce the complexity of business processes, streamline all communications with customers, and gain full visibility of the complete customer journey in collections processes, which is expected to fuel market growth in the BFSI sector.

- The World Bank report stated that the domestic credit to the private sector in low and medium-income countries had increased significantly and crossed their GDP in FY 2022, which showed the increase in the amount of debt in the market and raised the demand for an automated and software-based debt collection systems in the financial institutions.

Asia-Pacific is Expected to Register Significant Growth

- The debt collection landscape in China has undergone a remarkable transformation over the past few years due to new, technology-driven approaches that offer increased efficiency and compliance in debt collection. Additionally, the market's growth over the forecast period is analyzed in light of the rising bad debts and the increasing need to automate debt collection processes in end-user industries.

- The growth of the debt collection software market in China is largely driven by the increasing demand among end-user industries to minimize bad debt and automate debt collection through advanced technology-based software. As the country's financial market continues to grow and adapt, market vendors offering innovative debt collection solutions will continue to gain significant traction in ensuring efficient, compliant, and secure debt collection processes for end-user industries.

- In India, the debt collection software market has witnessed substantial growth in recent years. It is expected to continue growing due to the significant presence of global market vendors, the emergence of new debt collection software platforms, increasing bad loans, and technological advancements in debt collection practices. Challenges associated with the current economic landscape, especially in managing debt collection across various channels, lead to operational inefficiencies and rising expenses for banks and NBFCs, necessitating the adoption of debt collection software.

- The debt collection industry in India swiftly embraced technology post-pandemic, experiencing substantial momentum. The rising demand for credit, evolving consumer preferences, and the expectation of seamless experiences have compelled lenders to adopt digitization to automate debt collection practices. This expectedly boosts the adoption of debt collection software in lending organizations, aiding lenders in saving time, costs, resources, and reputation while simultaneously improving customer experience and retention rates.

- The Rest of Asia-Pacific, including Australia, Japan, South Korea, and New Zealand, is expected to register significant growth in the debt collection software market during the forecast period. This growth is attributed to increasing digitization and the need for automated debt collection in end-user industries such as banks, collection agencies, telecom, and governments. The growing imperative to minimize bad loans, coupled with the substantial presence of both regional and global market vendors, further fuels this growth.

Debt Collection Software Industry Overview

The debt collection software market exhibits a semi-consolidated landscape, with moderate penetration due to the considerable presence of suppliers in the region. These entities are progressively engaging with various digital technology startups to introduce advanced solutions. Among the notable players in this market are Fidelity National Information Services Inc. (FIS), CGI Inc., Fair, Isaac and Company (FICO) (Constellation Software Inc.), TransUnion LLC, and Pegasystems Inc.

- June 2024: Acquired.com, a forward-looking payments firm specializing in recurring commerce, and Flexys, a prominent UK collections technology provider, proudly unveiled their collaboration. Acquired.com's primary goal is equipping enterprises, such as Flexys, with cutting-edge payment tools to streamline and enhance their payment processes. Thanks to this collaboration, Flexys has seamlessly integrated a solution, elevating the payment experience for its customers.

- March 2024: Skit.ai, a prominent player in conversational AI solutions for accounts receivables, unveiled a cutting-edge suite of self-service offerings. These are designed to not only streamline debt collection but also to enrich consumer interactions. Skit.ai's latest offerings harness generative AI technology, spanning voice, chat, email, and text channels.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Impact of COVID-19 on the Debt Collection Software Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Automation in the Debt Collection Process

- 5.1.2 Outsourcing Debt Recovery to Specialized Debt Collection Agencies

- 5.2 Market Restraints

- 5.2.1 Inadequacy of Legacy Systems

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 Cloud-based

- 6.1.2 On-premise

- 6.2 By Organization Size

- 6.2.1 Large Enterprises

- 6.2.2 Small and Medium-sized Enterprises

- 6.3 By End User

- 6.3.1 Financial Institutions (Banks and NBFC)

- 6.3.2 Collection Agencies

- 6.3.3 Healthcare

- 6.3.4 Government

- 6.3.5 Telecom and Utilities

- 6.3.6 Other End Users (Real Estate and Retail)

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 Spain

- 6.4.2.4 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 India

- 6.4.3.3 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Mexico

- 6.4.4.3 Colombia

- 6.4.4.4 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fidelity National Information Services Inc. (FIS)

- 7.1.2 CGI Inc.

- 7.1.3 Fair, Isaac and Company (FICO) (Constellation Software Inc.)

- 7.1.4 TransUnion LLC

- 7.1.5 Pegasystems Inc.

- 7.1.6 Temenos AG

- 7.1.7 Intellect Design Arena Limited

- 7.1.8 Nucleus Software Exports Limited

- 7.1.9 Chetu Inc.

- 7.1.10 AMEYO (Exotel Techcom Pvt. Ltd)

- 7.1.11 EXUS Ltd

- 7.1.12 KuhleKT Pty Ltd