|

|

市場調査レポート

商品コード

1690127

ゼロトラストセキュリティ-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Zero Trust Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ゼロトラストセキュリティ-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 152 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

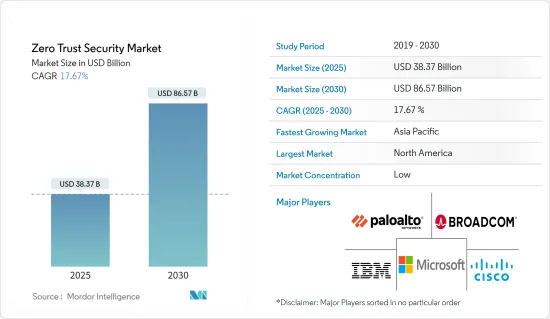

ゼロトラストセキュリティ市場規模は、2025年に383億7,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは17.67%で、2030年には865億7,000万米ドルに達すると予測されます。

クラウドコンピューティングへの移行に伴い、企業はセキュリティ体制を見直す必要に迫られています。ゼロトラストは、クラウドベースのアプリやデータへの安全なアクセスを実現するもので、クラウドファーストの計画に適しています。企業は、GDPRやCCPAのような厳格なデータプライバシー法を遵守するために、堅牢なデータ保護メカニズムを開発する必要があり、ゼロトラストはコンプライアンスを可能にします。企業は基本的なセキュリティ戦略として、さまざまなセグメントでゼロトラストのフレームワークをより広く活用しています。従来の境界ベースのパラダイムは放棄されつつあります。大手技術企業がゼロトラストのセキュリティビジネスを買収し、セキュリティサービスを向上させています。

主要ハイライト

- ゼロトラストセキュリティの導入を成功させるため、企業はサイバーセキュリティベンダーやマネージドセキュリティサービスプロバイダ(MSSP)との提携をますます進めています。こうした提携は、より広範なセキュリティ境界の保護という課題に対処するための知識とリソースを提供するものです。柔軟性、拡大性、コスト効率を提供するクラウドコンピューティングの利用拡大により、企業の機能は完全に変化しています。機密情報や重要なアプリケーションは、もはやオンプレミスのデータセンターに限定されなくなり、セキュリティ境界も拡大しました。

- 企業は多くのクラウドプロバイダを頻繁に利用するため、データやアプリケーションが散在することになります。このようなマルチクラウド戦略では、拡大したセキュリティ境界を確保することがより困難になります。責任共有アプローチでは、クラウドサービスプロバイダ(CSP)がインフラを保護し、顧客はデータとアプリケーションの保護を担当します。この責任分担により、包括的なセキュリティプランの必要性が強調されます。従業員やサードパーティのパートナーは、さまざまな場所やデバイスを使ってクラウドサービスにアクセスします。そのため、継続的なモニタリングと安全なアクセス制御が必要となります。

- データやユーザーが多数の場所やデバイスに分散しているような、変化するセキュリティ境界に適応することは、サイバーセキュリティの将来にとって不可欠です。ゼロトラストセキュリティは、新たな脅威を先取りし、現在の問題に対処するためのスケーラブルなアーキテクチャを記載しています。世界のゼロトラストセキュリティ市場は、このようなシフトに対応して企業がセキュリティ施策を再評価し続け、革新的なソリューションがサイバーセキュリティの展望を継続的に再構築していることから、持続的な成長が見込まれています。

- ゼロトラストセキュリティの導入は、レガシーシステムを持つ企業にとって長い移行期間を必要とします。その結果、徹底したセキュリティ対策の展開が遅れる可能性があります。ゼロトラスト・アプローチに沿うように、過去のシステムをアップグレードしたり置き換えたりするには、時間、費用、労力がかかります。その結果、ゼロトラストの取り組みの採用を思いとどまる企業も出てくる可能性があります。組織が最新のシステムとアプリケーションにゼロトラストセキュリティを使用するようになると、レガシーコンポーネントにセキュリティ上の欠陥が生じ、ネットワークの他の部分でゼロトラストの利点が相殺される可能性があります。

- ゼロトラストセキュリティは、COVID-19以降の環境では、より重要になっています。リモートワーク、クラウド、新たな脅威、コンプライアンス義務によって、柔軟でプロアクティブなセキュリティアプローチの必要性が浮き彫りになっています。ゼロトラストを採用する組織は、ポスト・パンデミック・シナリオの課題に対処し、絶えず進化するデジタル環境で最も重要な資産を保護するためのより良い体制を整えています。

ゼロトラストセキュリティ市場の動向

中小企業が大きな成長を遂げる

- 中小企業は、金融包摂の強化に貢献し、貧困層や十分なサービスを受けていない市場に商品やサービスを供給するなど、経済情勢において中心的な役割を果たしています。これらの企業はイノベーションの重要な推進力であり、高い成長の可能性を秘めています。例えば、欧州委員会によると、欧州連合(EU)には2023年に約2,440万社の中小企業(SME)が存在すると推定されており、中小企業は欧州経済の屋台骨を形成しています。

- ハイブリッドモデルに従っても、ほとんどの中小企業は、将来の職場環境や従業員施策の柔軟性にまだ対応できていないです。在宅勤務の増加、ハイブリッド型勤務形態、家族中心の従業員体制は、より安全な戦略への迅速な移行を支援します。持続可能性を確保するために、中小企業は市場機会と消費者の需要を見極める必要があります。

- クラウドベースの環境は長期的な持続可能性と回復力を保証し、中小企業向けのさまざまなサイバーセキュリティ戦略の需要を促進しています。堅牢で安全な作業環境は、ゼロトラストセキュリティによって保証され、組織のネットワークアーキテクチャにアクセスしようとする試みは、信頼が検証されて初めて成功します。ユーザーがアプリケーションにアクセスすると、ユーザーとデバイスが確認され、信頼が継続的にモニタリングされます。これにより、どのようなユーザー、デバイス、場所からも組織のアプリケーションと環境を保護することができ、これは中小企業の将来の成長に不可欠です。

- 既存のサイバーセキュリティ企業や新興のサイバーセキュリティ企業の多くは、高まる需要に対応するため、中小企業向けにゼロトラストネットワークアクセス(ZTNA)サービスを提供しています。クラウド配信サービスは、クラウドネイティブなビジネスや企業にゼロトラストソリューションを拡大し、クラウドの採用を受け入れ、中小企業に生産性の向上、セキュリティの強化、可視性の向上、攻撃対象の大幅な削減をもたらします。

大きな成長が期待されるアジア太平洋

- アジアの技術力は過去10年間で向上し、多くの企業がデジタルシフトを重要な目標の1つとして掲げています。デジタルトランスフォーメーションの革命はもっと以前から始まっていたが、パンデミックはそのスピードを加速させました。特に、組織がITエコシステムとセキュリティにどのように取り組むかに影響を与えました。

- アジア太平洋は世界の製造業を席巻し、特に中国で最も高い年間成長率を記録すると予想されます。この国は、パンデミック以前のペースと比較して、生産率の大幅な伸びを達成しています。

- 中国はデジタル化を優先し、サイバーセキュリティ態勢を改善し続けています。ZATのソリューションは、そのデジタル業務を保護し、規制基準への準拠を支援します。中国企業はZATソリューションの価値をますます認識するようになっており、中国市場はアジア太平洋における導入の重要な原動力となっています。

- 2023年8月、アジアをリードする通信技術グループであるシングテルは、アジアで初めてZscalerのセキュリティソリューションを提供する戦略的パートナーシップを発表しました。この提携により、SingtelのMSSEは、社内のリソースやスキルが不十分な企業に、サイバー脅威からデジタル資産を保護するオールインワンのデジタルセキュリティソリューションを記載しています。

- シングテルのマネージドセキュリティサービスエッジ(MSSE)は、専任のサイバーセキュリティ専門家によるプリセールスからポストセールスサポート、構築、プラットフォームコンサルテーション、メンテナンス、24時間体制の脅威緩和などのリソースを記載しています。企業のデジタル化がかつてないペースで加速し続ける中、サイバー脅威のリスクも高まっています。

ゼロトラストセキュリティ市場概要

ゼロトラストセキュリティ市場は、Cisco Systems Inc.、Palo Alto Networks Inc.、IBM Corporation Inc.、Broadcom Inc. Symantec Corporation、Microsoft Corporationといった世界的・地域的参入企業が存在し、セグメント化されています。製品の差別化は中程度から高水準で、製品の浸透度は高まっており、市場競争は激しくなっています。一般的に、ソリューションは包装ソリューションとして提供され、統合された提供物は製品のサービスの一部のように見えます。

- 2023年9月、BroadcomはVMwareを買収しました。VMwareの買収により、BroadcomはシマンテックのセキュリティポートフォリオとVMwareのSD-WAN機能を融合させることができます。Symantec、VMware SD-WAN、Carbon Blackのセキュリティ機能の一部を統合することで、Broadcomは単一ベンダーのセキュアアクセスサービスエッジ(SASE)産業に参入し、うまくいけばSASE産業全体のシェアと収益を高めることができます。Broadcomの現在のシマンテック SASEとセキュリティサービスエッジ(SSE)ポートフォリオには、セキュアウェブゲートウェイ(SWG)、データ損失防止(DLP)、クラウドアクセスセキュリティブローカー(CASB)、ゼロトラストネットワークアクセス(ZTNA)、SSL検査、ウェブ分離などのコンポーネントが含まれます。

- 2023年7月、AccentureはPalo Alto Networksと提携し、ゼロトラストセキュリティを強化しました。企業がサイバーセキュリティ態勢を改善し、ビジネス変革イニシアチブの実施を加速できるようにするため、両社は手を組み、SASEソリューションを使用してセキュアなアクセスサービスエッジソリューションを共同で記載しています。Palo Alto NetworksとAccentureは、企業の課題に取り組む包括的なマネージドSASEソリューションを記載しています。世界中の企業は、世界最大のシステムインテグレーターの強みとSASEソリューションを組み合わせることで、ビジネス変革を加速させることができ、ネットワークパフォーマンスの向上、一貫したセキュリティ施策と実装の恩恵を受けることができます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- COVID-19の影響

- 産業バリューチェーン分析

- 技術スナップショット

- ゼロトラストネットワーク

- ゼロトラストデバイス

- ゼロトラストデータ

- ゼロトラスト・ID確認

- ゼロトラストアプリケーション(可視化と分析)

第5章 市場力学

- 市場の促進要因

- データ漏えいの増加

- 組織のセキュリティ境界が職場に限定されないこと

- 市場抑制要因

- ゼロトラストモデルを採用しにくいレガシーなアプリケーション、インフラ、オペレーティングシステム

第6章 市場セグメンテーション

- 展開別

- オンプレミス

- クラウド

- 組織規模別

- 中小企業

- 大企業

- エンドユーザー産業別

- IT・通信

- BFSI

- 製造業

- 医療

- エネルギー電力

- 小売業

- 政府機関

- その他

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Cisco Systems Inc.

- Palo Alto Networks Inc.

- Broadcom Inc.(Symantec Corporation)

- Microsoft Corporation

- IBM Corporation

- Google Inc.

- Check Point Software Technologies Ltd

- Blackberry Limited

- Akamai Technologies Inc.

- Delinea(Centrify Corporation)

- Okta Inc.

- Fortinet Inc.

- Sophos Group PLC

- Cyxtera Technologies Inc.

第8章 投資分析

第9章 市場の将来

The Zero Trust Security Market size is estimated at USD 38.37 billion in 2025, and is expected to reach USD 86.57 billion by 2030, at a CAGR of 17.67% during the forecast period (2025-2030).

Organizations have had to review their security postures due to the move toward cloud computing. Zero Trust facilities secure access to cloud-based apps and data, which fits well with cloud-first plans. Organizations must develop robust data protection mechanisms to comply with strict data privacy laws like GDPR and CCPA, making Zero Trust a compliance enabler. Businesses use the Zero Trust framework in various sectors more widely as a fundamental security strategy. The conventional perimeter-based paradigm is being abandoned. Big technology corporations are buying Zero Trust security businesses to improve security services.

Key Highlights

- To successfully adopt zero-trust security, businesses are increasingly developing alliances with cybersecurity vendors and managed security service providers (MSSPs). These collaborations contribute knowledge and resources to handle the challenges of protecting the wider security perimeter. The growing use of cloud computing, which provides flexibility, scalability, and cost-efficiency, has completely changed how businesses function. Sensitive information and essential applications are no longer restricted to on-premises data centers, which also expanded the security perimeter.

- Businesses frequently use numerous cloud providers, which results in scattered data and applications. The enlarged security perimeter is more difficult to secure with this multi-cloud strategy. Under a shared responsibility approach, cloud service providers (CSPs) secure the infrastructure while customers are in charge of protecting their data and applications. This shared duty emphasizes the necessity of an all-encompassing security plan. Employees and third-party partners use a variety of locations and devices to access cloud services. So, there is a need for continuous monitoring and safe access controls.

- Adapting to the changing security perimeter, where data and users are dispersed across numerous locations and devices, is essential for the future of cybersecurity. Zero-trust security offers a scalable architecture to keep ahead of new threats and address current issues. The global zero-trust security market has been anticipated to experience sustained growth as enterprises continue to reevaluate their security policies in response to these shifts, with innovative solutions continuously reshaping the cybersecurity landscape.

- Adopting zero-trust security requires a longer transition period for organizations with legacy systems. The deployment of thorough security measures may be delayed as a result. It takes time, money, and labor to upgrade or replace historical systems so they align with the zero-trust approach. As a result, some businesses may be discouraged from adopting zero-trust efforts. Legacy components may develop security flaws as organizations progressively use zero-trust security for their contemporary systems and applications, thereby offsetting the advantages of zero trust elsewhere in the network.

- Zero Trust Security has become much more crucial in the post-COVID-19 environment. Remote work, the cloud, emerging threats, and compliance obligations highlight the necessity for a flexible, proactive security approach. Organizations that adopt zero trust are better equipped to deal with the challenges of the post-pandemic scenario and protect their most essential assets in a constantly evolving digital environment.

Zero Trust Security Market Trends

Small and Medium Enterprises to Witness Major Growth

- SMEs play a central role in the economic landscape, helping to strengthen financial inclusion and supplying goods and services to poor and underserved markets. These enterprises are critical drivers of innovation and offer high growth potential. For instance, according to the European Commission, approximately 24.4 million small and medium-sized enterprises (SMEs) were estimated to be in the European Union in 2023, as SMEs form the backbone of the European economy.

- Even following a hybrid model, most small businesses have yet to prepare for flexibility within future work environments and employee policies. Growth in working from home, hybrid modalities, and family-focused employee structures aid quick transition to more secure strategies. To ensure sustainability, MSMEs should identify market opportunities and consumer demands.

- The cloud-based environment ensures long-term sustainability and resilience, driving the demand for various cybersecurity strategies for SMEs. A robust and secure work environment is guaranteed with zero-trust security, and an attempt to access an organization's network architecture can only succeed once trust is validated. When a user accesses an application, the user and device are confirmed, and trust is continuously monitored. This helps secure the organization's applications and environments from any user, device, and location, which is vital for SME's future growth.

- Many established and emerging cybersecurity players offer zero-trust network access (ZTNA) services for small and medium enterprises to cater to the rising demands. The cloud-delivered service extends the company's zero-trust solutions to cloud-native businesses and enterprises, embracing cloud adoption and giving SMEs improved productivity, better security, greater visibility, and a significantly reduced attack surface.

Asia Pacific Expected to Register Significant Growth

- Asia's technological abilities have increased over the past decade, with many businesses concentrating on the digital shift as one of their key goals throughout the pandemic. While the revolutions of digital transformation were set in motion much earlier, the pandemic accelerated their speed. It particularly impacted how organizations approach their IT ecosystem and security.

- Asia-Pacific is anticipated to dominate the global manufacturing industry, recording the highest inter-annual growth rate, especially in China. This country has achieved significant growth in its production rates compared to its pre-pandemic pace.

- China keeps prioritizing digitalization and improving its cybersecurity posture. ZAT solutions safeguard its digital operations and help comply with regulatory standards. Chinese businesses are increasingly realizing the value of ZAT solutions, making the Chinese market a key driver of adoption in the Asia-Pacific region.

- In August 2023, Singtel, Asia's leading telecommunications technology group, announced a strategic partnership to offer Zscaler's security solutions in Asia, a first for the region. Through this partnership, Singtel's MSSE offers businesses impacted by insufficient in-house resources or skill sets an all-in-one digital security solution that helps to protect their digital assets against cyber threats.

- Enterprises in the APAC region will now have seamless access to Zscaler's Zero Trust Exchange, a cloud-based platform, through Singtel's Managed Security Service Edge (MSSE) suite of services, which includes pre-sales to post-sales support from dedicated cybersecurity experts as well as resources such as build implementation, platform consultation, maintenance, and round-the-clock threat mitigation. As the rate of enterprise digitalization continues to accelerate at an unprecedented pace, so does the risk of cyber threats.

Zero Trust Security Market Overview

The zero trust security market is fragmented with the presence of global and regional players such as Cisco Systems Inc., Palo Alto Networks Inc., IBM Corporation Inc., Broadcom Inc. (Symantec Corporation), and Microsoft Corporation. Moderate to high product differentiation, growing levels of product penetration, and high levels of competition characterize the market. Generally, the solutions are offered as a package solution, making the consolidated offering look like a part of the product's service.

- In September 2023, Broadcom acquired Vmware. With its potential VMware acquisition, Broadcom can meld Symantec's security portfolio with VMware's SD-WAN capabilities. By integrating Symantec, VMware SD-WAN, and some of Carbon Black's security capabilities, Broadcom could enter the single-vendor secure access service edge (SASE) industry and boost its overall SASE industry share and revenue if executed well. Broadcom's current Symantec SASE and security service edge (SSE) portfolio includes components such as secure web gateway (SWG), data loss prevention (DLP), cloud access security brokers (CASB), zero-trust network access (ZTNA), SSL inspection, and web isolation.

- In July 2023, Accenture teamed with Palo Alto Networks to bolster Zero Trust Security. In order to enable enterprises to improve their cybersecurity posture and speed up the implementation of business transformation initiatives, they have joined forces to deliver jointly secure access service edge solutions using a SASE solution. Palo Alto Networks and Accenture provide a comprehensive managed SASE solution that tackles organizations' challenges. Enterprises worldwide can accelerate their business transformation by combining the strength of the largest global systems integrator with the SASE solution, benefiting from improved network performance and a consistent security policy and implementation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19

- 4.4 Industry Value Chain Analysis

- 4.5 Technology Snapshot

- 4.5.1 Zero Trust Networks

- 4.5.2 Zero Trust Devices

- 4.5.3 Zero Trust Data

- 4.5.4 Zero Trust Identities

- 4.5.5 Zero Trust Applications (Visibility and Analytics)

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Number of Data Breaches

- 5.1.2 Security Perimeter of an Organization not Being Limited to Workplace

- 5.2 Market Restraints

- 5.2.1 Legacy Applications, Infrastructure, and Operating Systems Not Likely to Adopt Zero Trust Model

6 MARKET SEGMENTATION

- 6.1 By Deployment

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 By Organization Size

- 6.2.1 Small and Medium Enterprises

- 6.2.2 Large Enterprises

- 6.3 By End-user Industry

- 6.3.1 IT and Telecom

- 6.3.2 BFSI

- 6.3.3 Manufacturing

- 6.3.4 Healthcare

- 6.3.5 Energy and Power

- 6.3.6 Retail

- 6.3.7 Government

- 6.3.8 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems Inc.

- 7.1.2 Palo Alto Networks Inc.

- 7.1.3 Broadcom Inc. (Symantec Corporation)

- 7.1.4 Microsoft Corporation

- 7.1.5 IBM Corporation

- 7.1.6 Google Inc.

- 7.1.7 Check Point Software Technologies Ltd

- 7.1.8 Blackberry Limited

- 7.1.9 Akamai Technologies Inc.

- 7.1.10 Delinea (Centrify Corporation)

- 7.1.11 Okta Inc.

- 7.1.12 Fortinet Inc.

- 7.1.13 Sophos Group PLC

- 7.1.14 Cyxtera Technologies Inc.