|

市場調査レポート

商品コード

1435861

低GWP冷媒:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Low GWP Refrigerant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 低GWP冷媒:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

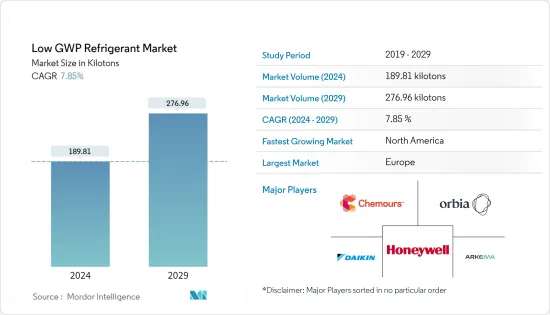

低GWP冷媒市場規模は2024年に18万9,810トンと推定され、2029年までに27万6,960トンに達すると予測されており、予測期間(2024年から2029年)中に7.85%のCAGRで成長します。

低GWP冷媒市場は、新型コロナウイルス感染症(COVID-19)のパンデミックによって悪影響を受けました。しかし、医薬品、住宅、商業用などの用途の増加により、市場は2021年に大幅に回復しました。

主なハイライト

- 環境への影響が少なく、厳しい規制が中期的に低GWP冷媒市場の成長の主な原動力となる可能性があります。

- しかし、可燃性やその他の毒性特性が高いため、低GWP冷媒市場の成長は制限されると予想されます。

- それにもかかわらず、低GWP冷媒を促進するための開発により、すぐに世界市場に有利な成長機会が生まれる可能性があります。

- 欧州が最大の市場であり、最大の消費国はドイツ、英国などです。

低GWP冷媒市場動向

市場を独占する業務用冷凍機

- 地球温暖化係数(GWP)の低い冷媒ソリューションは、空調および冷凍用途での需要が高まっています。これらの低GWP冷媒はエネルギー消費を増加させ、安全上のリスクをもたらし、大幅な機器の改造を必要とします。

- さらに、これらは主に、サービス機器のエネルギー消費と炭素排出量をHFCおよびCFCと比較して50%削減するために使用されます。

- 地球温暖化係数(GWP)の低い冷媒ソリューションは、空調および冷凍用途での需要が高まっています。これらの低GWP冷媒はエネルギー消費を増加させ、安全上のリスクをもたらし、大幅な機器の改造を必要とします。

- 低GWP冷媒の使用は、特に乳製品、食肉、漁業、および効率的なコールドチェーンネットワーク(業務用冷凍庫および冷蔵庫)に依存するその他の食品産業における食品の安全性を含む、さまざまな用途を含む業務用冷凍部門で増加しています。製薬業界の保存、業務用エアコン。

- 日本空調冷凍協会が2022年 6月に発表したデータによると、2021年の世界の業務用エアコン需要は大幅に増加し、1,488万台に達しました。同年は北米地域が前年実績を上回る合計737万台で首位となった。

- ハイアールスマートホームによると、アジアのエアコン小売台数は2022年に1億3,230万台に達し、2024年までに1億4,740万台に達すると推定されています。

- さらに、OEA(インド)によると、エアコンの卸売価格指数は2022年に119.4に達しました。

- 冷凍食品の需要が増大し、利益率が低い競争の激しい市場に伴い、ほとんどの食品加工業者、流通業者、小売業者は、手動で操作する時代遅れの施設から、商業用冷蔵設備が広く採用されている高層冷凍倉庫に移行しつつあります。

- さらに、多国籍企業による小売食品チェーンの拡大と(貿易自由化による)国際貿易の成長により、コールドチェーンプロセスの需要が増加しています。これにより、世界中で業務用冷凍機の需要が増大しています。

ドイツが欧州市場を制覇へ

- ドイツ経済は欧州最大であり、世界でも第5位です。ドイツは、特に機械と自動車の分野で強力な製造部門を持っています。これにより、この国は国際貿易における競争力を維持し、海外投資を呼び込むことができました。

- 2022年 6月に日本の空調冷凍工業会が発表したデータによると、ドイツの業務用エアコンの販売は2021年に大幅に増加し、需要は5万台に達しました。この需要の急増は、前年に比べて顕著な増加を示しました。

- ドイツの食品および飲料産業は最大の産業分野です。食品加工は国内の食品および飲料業界の主要な活動の1つであり、冷蔵の大きな必要性が生じます。この国の食品および飲料の輸出事業は726億ユーロ(約796億米ドル)を超えています。

- 国内で加工される主な食品には、肉やソーセージ製品、乳製品、焼き菓子、菓子類が含まれます。これらの製品のほとんどは、賞味期限を延ばすために冷蔵保存が必要であり、さらに冷蔵需要が生じています。

- 連邦食糧農業省(BMEL)によると、ドイツの一人当たりの肉消費量は2022年に77.5キログラムに達しました。

- ドイツは世界最大の清涼飲料消費国の一つで、一人当たりの清涼飲料水の消費量は120リットルを超えています。現在のドイツ市場では、カフェイン中心の飲料が最も活発です。これにより、スプライト、ファンタ、デルタ、メゾミックス、コカ・コーラなどの企業の売上が増加しました。これらの冷たい飲み物を冷蔵保存する必要があるため、冷蔵需要が大幅に増加しています。

- さらに、より優れた極低温装置の使用と冷凍食品の需要の増加により、国内の低GWP冷凍市場は今後数年間で成長率が高まると見込まれています。

- ただし、食品加工のアフターマーケットからの需要は大きく、今後数年間で自動車業界からの冷媒の需要が増加すると予想されます。

低GWP冷媒業界の概要

低GWP冷媒市場は本質的に部分的に統合されており、調査対象市場のわずかなシェアを占める企業が存在します。市場の主要企業としては、Honeywell International Inc.、The Chemours Company、Orbia、Arkema、DAIKIN INDUSTRIES, Ltd.などが挙げられます(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 環境への影響が少ない

- 厳しい規制

- その他の 促進要因

- 抑制要因

- より高い可燃性およびその他の毒性特性

- その他の拘束具

- 業界のバリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替製品やサービスの脅威

- 競合の程度

第5章 市場セグメンテーション

- タイプ

- 無機物

- 炭化水素

- フルオロカーボンおよびフルオロオレフィン(HFCおよびHFO)

- 応用

- 業務用冷凍庫

- 産業用冷凍装置

- 家庭用冷蔵庫

- その他の用途

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他

- 南米

- ブラジル

- アルゼンチン

- その他

- 中東とアフリカ

- サウジアラビア

- 南アフリカ

- その他

- アジア太平洋

第6章 競合情勢

- 合併と買収、合弁事業、コラボレーション、および契約

- 市場ランキング分析

- 有力企業が採用した戦略

- 企業プロファイル

- A-Gas

- Arkema

- DAIKIN INDUSTRIES, LTD.

- Danfoss

- engas Australasia

- GTS SPA

- HARP International

- Honeywell International Inc

- Linde

- Messer Group

- Orbia

- Tazzetti SpA

- The Chemours Company

第7章 市場機会と将来の動向

The Low GWP Refrigerant Market size is estimated at 189.81 kilotons in 2024, and is expected to reach 276.96 kilotons by 2029, growing at a CAGR of 7.85% during the forecast period (2024-2029).

The low GWP refrigerant market was negatively impacted by the COVID-19 pandemic. However, the market recovered significantly in 2021, owing to rising applications in pharmaceuticals, residential, commercial, and others.

Key Highlights

- The low environmental impact and stringent regulations are likely to be the main driver of the low GWP refrigerant market's growth over the medium term.

- However, the higher flammability and other toxicity characteristics are expected to limit the growth of the low GWP refrigerant market.

- Nevertheless, developments for promoting low GWP refrigerants are likely to create lucrative growth opportunities for the global market soon.

- Europe represents the largest market,with the largest consumption coming from countries such as Germany,United Kingdom, etc.

Low GWP Refrigerant Market Trends

Commercial Refrigeration to Dominate the Market

- Low global warming potential (GWP) refrigerant solutions have been in greater demand for air conditioning and refrigeration applications. These low-GWP refrigerants increase energy consumption, introduces safety risks, and require significant equipment modifications.

- Moreover, these are primarily used to reduce service equipment energy consumption and carbon emissions by 50% compared to HFCs and CFCs.

- Low global warming potential (GWP) refrigerant solutions have been in greater demand for air conditioning and refrigeration applications. These low-GWP refrigerants increase energy consumption, introduces safety risks, and require significant equipment modifications.

- The usage of low GWP refrigerants is increasing, especially in the commercial refrigeration segment that includes varied applications, including food safety in dairy, meat, fisheries, and other food industries that rely on efficient cold chain networks (commercial freezers and refrigerators), cold chain preservation in the pharmaceutical industry, commercial air conditioners.

- Based on data published by the Air Conditioning and Refrigeration Association of Japan in June 2022, the worldwide demand for commercial air conditioners experienced a significant increase in 2021, reaching 14.88 million units. The North America region took the lead with a total of 7.37 million units in the same year, surpassing previous years figures.

- According to The Haier Smart Home, Asia's air-conditioners retail unit volume has reached 132.3 million units in 2022 and is estimated to reach 147.4 million units by 2024.

- Furthermore, according to OEA (India), the wholesale price index of air conditioners reached 119.4 in 2022.

- With the increasing demand for frozen food products and a highly competitive market with low margins, most food processors, distributors, and retailers are shifting from manually operated obsolete facilities to the high bay deep-freeze warehouses, where commercial refrigeration are widely employed.

- Moreover, the expansion of retail food chains by the multinational companies and the growth in international trade (due to trade liberalization) have led to an increase in the demand for the cold chain processes. This, in turn, is augmenting the demand for commercial refrigeration across the world.

Germany to Dominate the Europe Market

- The German economy is the largest in Europe and the fifth-largest in the world. Germany has a strong manufacturing sector, particularly in the areas of machinery and automotive. This has helped the country maintain a competitive edge in international trade and attract foreign investment.

- Based on the data published by the Association of Air Conditioning and Refrigeration Industry in Japan in June 2022, the sales of commercial air conditioning units in Germany experienced a significant increase in 2021, with the demand reaching 50 thousand units. This surge in demand marked a notable rise compared to previous years.

- The German food and beverage industry is the largest industry sector. Food processing is one of the major activities in the domestic food and beverage industry, which creates a significant need for refrigeration. The country's food and beverage export business exceeds more than EUR 72.6 billion (~USD 79.6 billion).

- Some of the major foods processed in the country include meat and sausage products, dairy products, baked goods, and confectionery. Most of these products need cold storage in order to increase their shelf life, further creating a demand for refrigeration.

- According to The Federal Ministry of Food and Agriculture( BMEL), Germany's per capita consumption of meat has reached 77.5 kilograms in 2022.

- Germany is one of the world's largest consumers of soft drinks with more than 120 liters of per-capita consumption. Caffeine-oriented drinks are the most dynamic in the present German market. This has given a boost to the sales of companies, such as Sprite, Fanta, Delta, Mezzo Mix, and Coca-Cola. The need for cold storage of these cold drinks has created a significant demand for refrigeration.

- Furthermore, with the use of better cryogenic equipment and the increased demand for frozen foods, the low GWP refrigeration market is poised to witness an increasing growth rate in the coming years in the country.

- However, there is significant demand from the food processing aftermarket, which is expected to increase the demand for refrigerants from the automotive industry in the coming years.

Low GWP Refrigerant Industry Overview

The low GWP refrigerants market is partially consolidated in nature, with players accounting for a marginal share of the market studied. A few major companies in the market (not in particular order) include Honeywell International Inc., The Chemours Company, Orbia, Arkema, and DAIKIN INDUSTRIES, Ltd., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Low Environmental Impact

- 4.1.2 Stringent Regulations

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Higher Flammability and Other Toxicity Characteristics

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Inorganics

- 5.1.2 Hydrocarbons

- 5.1.3 Fluorocarbons and Fluoro-olefins (HFCs and HFOs)

- 5.2 Application

- 5.2.1 Commercial Refrigeration

- 5.2.2 Industrial Refrigeration

- 5.2.3 Domestic Refrigeration

- 5.2.4 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 A-Gas

- 6.4.2 Arkema

- 6.4.3 DAIKIN INDUSTRIES, LTD.

- 6.4.4 Danfoss

- 6.4.5 engas Australasia

- 6.4.6 GTS SPA

- 6.4.7 HARP International

- 6.4.8 Honeywell International Inc

- 6.4.9 Linde

- 6.4.10 Messer Group

- 6.4.11 Orbia

- 6.4.12 Tazzetti S.p.A

- 6.4.13 The Chemours Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Developments for Promoting Low GWP Refrigerants

- 7.2 Other Opportunities