|

市場調査レポート

商品コード

1406113

砲塔システム:市場シェア分析、産業動向・統計、成長予測、2024年~2029年Turret Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 砲塔システム:市場シェア分析、産業動向・統計、成長予測、2024年~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

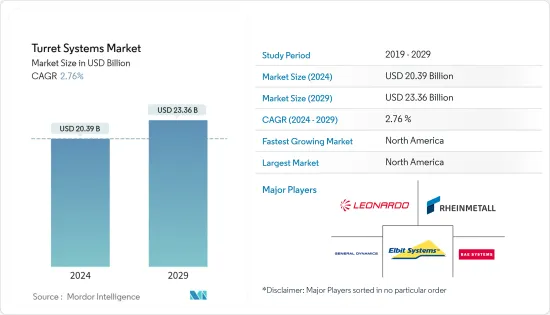

砲塔システム市場規模は2024年に203億9,000万米ドルと推定され、2029年には233億6,000万米ドルに達すると予測され、予測期間(2024-2029年)のCAGRは2.76%で成長する見込みです。

この市場を牽引しているのは、主に各国の国防費の伸びと、軍事力強化のための最新技術兵器の近代化・調達プログラムへの注目の高まりです。これらのシステムは、軍の火力と状況認識を強化する上で極めて重要であり、多額の投資を集めています。さらに、機動性と迅速な対応が不可欠な市街戦シナリオにおける砲塔システムの需要の高まりが、市場の成長をさらに後押ししています。

国境警備や対テロ作戦のニーズの高まりは、さまざまな防衛軍による砲塔システムへの需要を高めています。高度な監視センサーと遠隔操作兵器を装備した砲塔システムは、国境、重要インフラ、機密地域の監視と保護に不可欠です。テロや国境を越えた脅威に関する世界の懸念が続いていることから、継続的な監視と迅速な対応が可能な砲塔システムに対する需要が高まっています。

地域によっては予算上の制約があるため、先進的な砲塔システムの調達には多額の研究開発・導入コストがかかることが多いです。さらに、高度なセンサーや照準システムなどの高度な技術を砲塔システムに統合する際には、既存のプラットフォームとの互換性や、信頼性と安全性のための厳格なテストが必要となるため、その複雑さが課題となる可能性があります。これらの要因は、砲塔システム市場全体の拡大を減速させる可能性があります。

砲塔システム市場の動向

無人セグメントは予測期間中に最も高いCAGRで成長すると予測される

プラットフォームタイプに基づくと、無人セグメントは予測期間中に最も高いCAGRで成長すると予想されます。さまざまなプラットフォーム向けの無人砲塔システムの調達が増加していることから、設置台数の増加とそれに伴う市場収益の増加により、無人セグメントの成長が加速すると予想されます。砲塔システムの技術進歩により無人砲塔が誕生し、現在では地上軍に競争力をもたらしています。無人砲塔システムは、人工知能や機械学習のような最新技術を搭載しており、戦場での有効性を高めています。無人砲塔システムの助けを借りて、軍は武器を遠隔操作することができます。陸、空、海を拠点とする複数の車両に設置された軍備を支援し、軍人を直接露出させることで致命傷を避けることができます。例えば、2021年8月、米国陸軍契約司令部は、ストライカー旅団戦闘チーム(SBCT)を30mm中口径兵器システム(MCWS)、無人砲塔自動砲でアップグレードするために、オシュコシュ・ディフェンスに9,900万米ドルの契約を獲得しました。米国陸軍は2021年6月、ストライカー・ダブルVハル歩兵輸送車(ICVVA1)に30ミリMCWSを搭載する6年間のプログラムにオシュコシュ・ディフェンスを選定しました。このような開発は、予測期間中の同分野の成長に貢献すると予想されます。

北米が予測期間中に市場を独占する

地域別では、北米が予測期間中に市場シェアをリードすると予測されます。北米では、米国が市場を独占すると予測されており、その要因としては、兵器システムに対する政府の高額支出や、米国の軍事力強化のための主要企業による新型砲塔システムの研究開発などが挙げられます。砲塔システムは、1つの目標に照準を合わせるだけでなく、弾丸を発射する武器の乗組員や機構を格納する回転可能な武器マウントであり、同時に武器をある程度仰角をつけて照準し、発射させることができるため、多くの面で有益です。これは陸上だけでなく空中でも陸軍の目的を果たすもので、そのためこの地域の政府は車両の近代化と砲塔システムの搭載に多額の予算を投じています。2023年8月、エルビット・システムズの子会社エルビット・アメリカは、米国陸軍の作戦の致死性と生存性を強化する構えで、ブラッドレー戦闘車用の砲手ハンドステーションの設計・製造契約を獲得しました。砲塔の位置決めや火器管制システムの操作に不可欠なこれらの部品は、米国陸軍の戦場能力をさらに強化することになります。さらに米国は、ウクライナ軍を輸送し、ロシア・ウクライナ戦争後の防衛・攻撃能力を提供するために、ブラッドレー戦闘車両をウクライナに引き渡しました。

砲塔システム産業の概要

砲塔システム市場は断片化されています。砲塔システム市場で著名な企業には、BAE Systems plc、Leonardo S.p.A.、Elbit Systems Ltd.、Rheinmetall AG、General Dynamics Corporationなどがあります。いくつかの企業は軍隊と長期的なパートナーシップを結び、軍隊の砲塔システムをアップグレードし強化しています。企業はまた、軍がライバルに対して戦術的に優位に立てるような先進的な砲塔システムを革新するための研究開発にも多額の投資を行っています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- プラットフォーム

- 航空

- 海上

- 陸上

- タイプ

- 有人

- 無人

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- イスラエル

- 南アフリカ

- その他中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Rheinmetall AG

- BAE Systems plc

- Elbit Systems Ltd.

- Leonardo S.p.A.

- Denel SOC Ltd.

- General Dynamics Corporation

- Kongsberg Gruppen ASA

- Textron Inc.

- John Cockerill S.A.

- Moog Inc.

- Rafael Advanced Defense Systems Ltd.

- Electro Optic Systems(EOS)

第7章 市場機会と今後の動向

The Turret Systems Market size is estimated at USD 20.39 billion in 2024, and is expected to reach USD 23.36 billion by 2029, growing at a CAGR of 2.76% during the forecast period (2024-2029).

The market is primarily driven by the growth in defense spending by various countries and the growing focus on the modernization and procurement programs for the latest technology weapons to increase military strength. These systems are crucial in enhancing a military's firepower and situational awareness, attracting substantial investments. Moreover, the rising demand for turret systems in urban warfare scenarios, where maneuverability and quick response are vital, further boosts the market growth.

The increasing need for border security and counter-terrorism operations is increasing the demand for turret systems by various defense forces. Turret systems equipped with advanced surveillance sensors and remotely operated weapons are essential in monitoring and protecting borders, critical infrastructure, and sensitive areas. The ongoing global concerns related to terrorism and cross-border threats have led to a higher demand for turret systems capable of providing continuous surveillance and rapid response.

Budget constraints in certain regions can hinder the procurement of advanced turret systems, as they often involve substantial research, development, and implementation costs. Additionally, the complexity of integrating sophisticated technologies, such as advanced sensors and targeting systems, into turret systems can pose challenges, as it requires compatibility with existing platforms and rigorous testing for reliability and safety. These factors may slow down the overall expansion of the turret systems market.

Turret Systems Market Trends

The Unmanned Segment is Expected to Grow with the Highest CAGR During the Forecast Period:

Based on the platform type, the unmanned segment is expected to grow with the highest CAGR during the forecast period. With the growing procurement of unmanned turret systems for various platforms, the unmanned segment is expected to grow faster due to increased installations and the corresponding market revenues. The technological advancement in turret systems has given rise to unmanned turrets, which now provide a competitive edge to the ground forces. The unmanned turret systems are being powered with the latest technologies like artificial intelligence and machine learning, which increase their effectiveness on the battlefield. With the help of unmanned turret systems, militaries can operate the weapon remotely. They can avoid fatalities by exposing their army personnel directly, helping their installations over several land, air, and sea-based vehicles. For instance, in August 2021, the US Army Contracting Command was awarded a USD 99 million contract to Oshkosh Defense to upgrade an additional Stryker Brigade Combat Team (SBCT) with the 30 mm Medium Caliber Weapon System (MCWS), an unmanned turreted autocannon. In June 2021, the US Army selected Oshkosh Defense for a six-year program to integrate the 30 mm MCWS onto the Stryker Double V Hull Infantry Carrier Vehicle (ICVVA1). Such developments are expected to help the segment's growth during the forecast period.

North America is Projected to Dominate the Market During the Forecast Period:

In terms of geography, North America is projected to lead the market share during the forecast period. In North America, the United States is expected to dominate the market owing to factors such as high spending by the government on weapon systems and the research and development of new turret systems by the major players to enhance the military power of the US. The inclusion of the turret system is beneficial in many aspects as it not only aims at one single target, as it is a rotatable weapon mount that houses the crew or mechanism of a projectile-firing weapon and, at the same time, lets the weapon be aimed and, fired in some degree of elevation. This serves the army's purpose not only on land but also in the air, which is why the government in the region is spending heavily on modernization and the inclusion of turret systems in their vehicles. In August 2023, in a move poised to strengthen the lethality and survivability of the US Army operations, Elbit Systems subsidiary Elbit America won a contract to design and manufacture the gunner hand stations for the Bradley Fighting Vehicle. These components, critical for positioning turrets and enabling fire control systems operation, are set to further strengthen US Army battlefield capabilities. Moreover, the US also delivered Bradley Fighting Vehicles to Ukraine to help transport Ukrainian troops and provide defensive and offensive capabilities following the Russian-Ukraine war. Such developments are expected to enhance the market prospects in the region during the forecast period.

Turret Systems Industry Overview

The turret systems market is fragmented. Some prominent companies in the Turret System market are BAE Systems plc, Leonardo S.p.A., Elbit Systems Ltd., Rheinmetall AG, and General Dynamics Corporation, among others. Several companies have formed long-term partnerships with the armed forces to upgrade and enhance the turret systems of the militaries. Companies are also investing heavily in research and development to innovate advanced turret systems that may help the militaries have a tactical advantage over the rivals. For instance, in August 2023, The British Army's AS90 turret training system reached a significant milestone by firing 100,000 simulated rounds. AS90 is procured and supported by UK Defence Equipment & Support (DE&S). DE&S develops operational practices and skillsets of the commander, gunner, and loader of the 155mm self-propelled howitzer. Similarly, In May 2021, Rheinmetall received a contract worth USD 807 million from the British Ministry of Defence to upgrade the fleet of Challenger 2 main battle tanks (148 units) with the 120mm smoothbore main armament. The contract is expected to run till 2027. Such developments are expected to help the advent of newer technologies into the market during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Plaform

- 5.1.1 Air

- 5.1.2 Sea

- 5.1.3 Land

- 5.2 Type

- 5.2.1 Manned

- 5.2.2 Unmanned

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Russia

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Mexico

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Israel

- 5.3.5.4 South Africa

- 5.3.5.5 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Rheinmetall AG

- 6.2.2 BAE Systems plc

- 6.2.3 Elbit Systems Ltd.

- 6.2.4 Leonardo S.p.A.

- 6.2.5 Denel SOC Ltd.

- 6.2.6 General Dynamics Corporation

- 6.2.7 Kongsberg Gruppen ASA

- 6.2.8 Textron Inc.

- 6.2.9 John Cockerill S.A.

- 6.2.10 Moog Inc.

- 6.2.11 Rafael Advanced Defense Systems Ltd.

- 6.2.12 Electro Optic Systems (EOS)