タレットシステムの市場機会、成長促進要因、産業動向分析と2025年~2034年予測

Turret System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773479

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

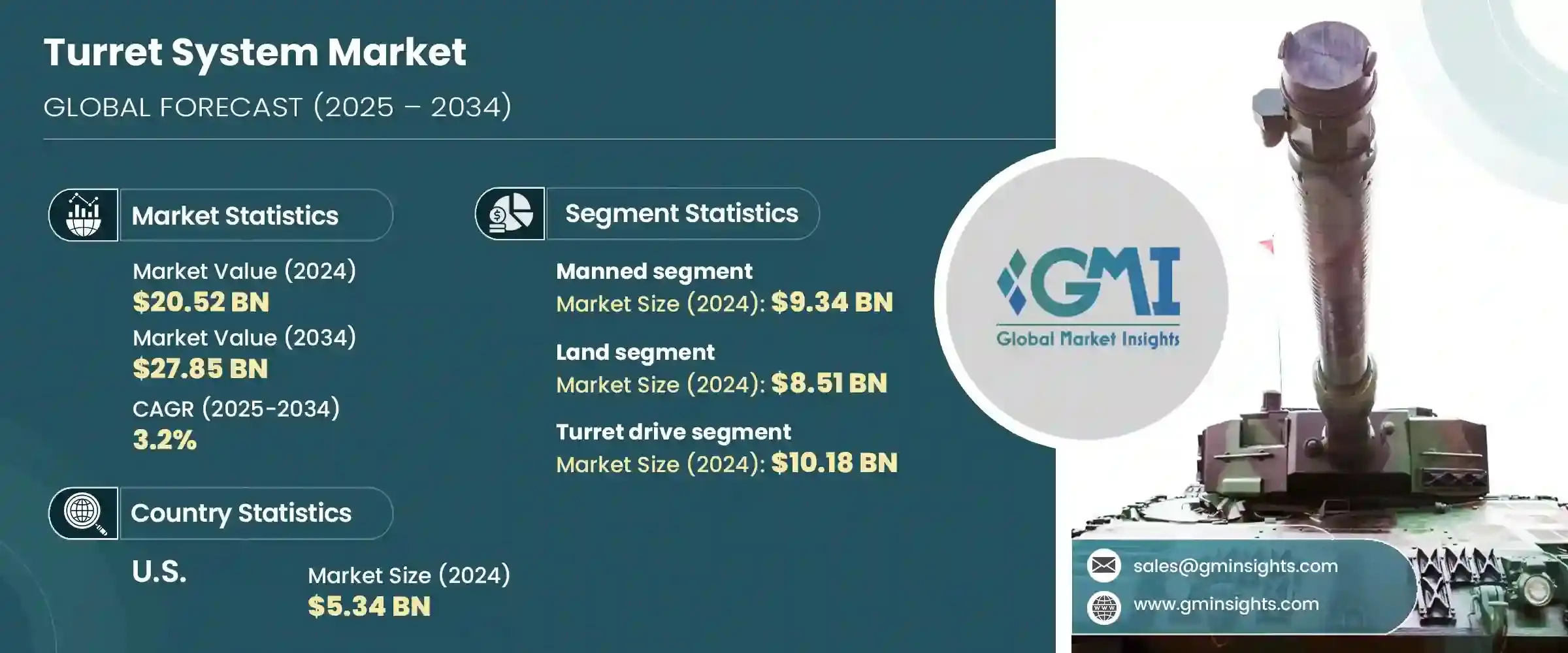

タレットシステムの世界市場は、2024年には205億2,000万米ドルとなり、CAGR 3.2%で成長し、2034年には278億5,000万米ドルに達すると予測されています。

この成長は、世界の軍事費の増加によるところが大きく、北米、欧州、アジア太平洋などの地域からの需要が大きいです。国防予算が拡大し続ける中、焦点は軍の近代化と戦闘準備態勢の強化に移っています。先進的な砲塔システム、特に無人砲塔システムは、任務遂行能力を高め、人員に対するリスクを軽減し、動的な作戦環境における戦略的効率を可能にする能力により、支持を集めています。

政府筋からの防衛研究開発への投資の増加は、特にAI、自動化、感覚統合などのタレットシステム技術の革新を推進しています。これらの進歩は、ロボットシステムや車両搭載型砲塔が達成できる限界に課題しており、その結果、契約締結が早まり、民間防衛企業による生産が増加しています。自律航行やAIベースの脅威認識といった技術は、戦場を再構築しています。これらはリアルタイムの状況認識、インテリジェントな意思決定、自律的な操縦を提供し、危険な任務への人間の関与を最小限に抑え、さまざまな地形やシナリオで作戦効果を最大化するために不可欠なものです。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 205億2,000万米ドル |

| 予測金額 | 278億5,000万米ドル |

| CAGR | 3.2% |

有人タレットシステムセグメントは、2024年に93億4,000万米ドルを生み出しました。これらのシステムは、人間の判断が極めて重要である複雑なリアルタイム状況での運用適応性により、引き続き優位を占めています。有人砲塔の信頼性は実証済みであり、多くの軍隊は、有人砲塔をそのまま置き換えるのではなく、既存の装甲車隊を次世代有人ソリューションでアップグレードすることを選択しています。市街地戦闘や対反乱作戦など、高度な状況認識を必要とする任務では、今後も有人システムに大きく依存することが予想されます。

陸上砲塔セグメントは、2024年に85億1,000万米ドルを生み出しました。世界の防衛支出の増加と、進化する脅威への迅速な対応の必要性の高まりにより、陸上車両は有人・無人プラットフォームともに先進的な砲塔システムを装備するようになっています。無人地上車両(UGV)の配備の増加は、遠隔操作が可能な砲塔システムの必要性を高めています。自動化、高精度センサー、AI駆動制御システムの革新により、陸上タレットプラットフォームの致死性、精度、コスト効率が向上しています。

ドイツタレットシステム2024年の市場規模は9億5,000万米ドル。インダストリー4.0とデジタル主権に向けた国家的推進により、自律型および半自律型軍事システムへの投資が拡大。これには、陸上車両と空中防衛プラットフォームの両方で使用される高度な砲塔システムの調達増加も含まれます。武器輸出大国であるドイツは、世界の競争力を維持するために技術革新の強化を続けています。監視や国境防衛などの任務でAIを搭載したロボット工学への依存が高まっていることは、安全保障上の要求の変化や運用の複雑性に適応する準備ができていることを裏付けています。

市場情勢を形成している主要企業には、BAE Systems、Elbit Systems、General Dynamics Land Systemsなどがあります。タレットシステム市場の主要企業は、無人化およびAI統合砲塔技術の革新を推進するため、研究開発に多額の投資を行っています。防衛省や政府機関との戦略的協力関係は、長期調達契約の確保に役立っています。競争力を強化するため、メーカーは生産能力を拡大し、モジュール式砲塔アーキテクチャを最適化し、性能を維持しながら軽量化するために最先端の素材を取り入れています。また、合併、買収、提携により、新たな地域市場を開拓し、製品ポートフォリオを多様化しています。さらに、企業は完全な置き換えよりも、次世代機能を備えたレガシー・プラットフォームのアップグレードに重点を置いており、既存の防衛関係の顧客との関係を維持し、ライフサイクル・サポートやシステムの改修を通じて継続的な収益を確保するのに役立っています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 主要部品の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 国防予算の増加と軍事近代化

- 技術革新と自動化

- 地政学的緊張と安全保障上の脅威

- 安全保障・防衛インフラの拡大

- アプリケーションの多様化

- 業界の潜在的リスク&課題

- 開発と調達費が高め

- 急速な技術陳腐化

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021-2034

- 主要動向

- 有人

- 無人

第6章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- 砲塔駆動装置

- 砲塔制御

- 安定化ユニット

第7章 市場推計・予測:プラットフォーム別、2021-2034

- 主要動向

- 土地

- 移動体/車両

- 固定式/据置型

- 空挺

- 攻撃ヘリコプター

- 戦闘機

- 特殊任務航空機

- 無人航空機(UAV)

- 海軍

- 駆逐艦

- フリゲート艦

- オフショア支援船(オースト)

- コルベット

- 哨戒・機雷掃海艇

- 水陸両用船

- 潜水艦

- 無人水上車両(米国)

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- BAE Systems

- Elbit Systems Ltd.

- General Dynamics Corporation

- Leonardo S.p.A.

- Lockheed Martin Corporation

- Moog Inc.

- Northrop Grumman

- RAFAEL Advanced Defense Systems Ltd.

- Rheinmetall AG

- Thales

目次

The Global Turret System Market was valued at USD 20.52 billion in 2024 and is estimated to grow at a CAGR of 3.2% to reach USD 27.85 billion by 2034. This growth is largely fueled by increasing global military expenditures, with significant demand coming from regions like North America, Europe, and Asia-Pacific. As defense budgets continue to expand, the focus shifts toward military modernization and enhanced combat readiness. Advanced turret systems, especially unmanned ones, are gaining traction due to their ability to enhance mission performance, reduce risks to personnel, and enable strategic efficiency in dynamic operational environments.

Increased investments in defense R&D from government sources are propelling innovation in turret system technologies, particularly in AI, automation, and sensory integration. These advancements are pushing the boundaries of what robotic systems and vehicle-mounted turrets can achieve, resulting in faster contract awards and increased production from private defense firms. Technologies like autonomous navigation and AI-based threat recognition are reshaping the battlefield. They provide real-time situational awareness, intelligent decision-making, and autonomous maneuvering-all critical for minimizing human involvement in dangerous missions and maximizing operational effectiveness across varied terrains and scenarios.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $20.52 Billion |

| Forecast Value | $27.85 Billion |

| CAGR | 3.2% |

The manned turret system segment generated USD 9.34 billion in 2024. These systems continue to dominate due to their operational adaptability in complex, real-time situations where human judgment remains crucial. Manned turrets offer proven reliability, and instead of replacing them outright, many armed forces are opting to upgrade existing armored fleets with next-gen manned solutions. Missions requiring heightened situational awareness-such as urban combat or counterinsurgency operations-are expected to continue relying heavily on manned systems.

The land-based turret segment generated USD 8.51 billion in 2024. With global defense spending on the rise and the growing need for rapid response to evolving threats, land vehicles are being equipped with advanced turret systems for both manned and unmanned platforms. The rise in deployment of Unmanned Ground Vehicles (UGVs) has amplified the need for turret systems capable of remote operation. Innovations in automation, precision sensors, and AI-driven control systems are making land turret platforms more lethal, accurate, and cost-effective.

Germany Turret System Market generated USD 950 million in 2024. A national push toward Industry 4.0 and digital sovereignty has led to expanded investment in autonomous and semi-autonomous military systems. This includes increased procurement of advanced turret systems for use in both land vehicles and aerial defense platforms. As one of the top arms-exporting countries, Germany continues to boost innovation to remain competitive globally. A growing reliance on AI-powered robotics for tasks like surveillance and border defense underlines the nation's readiness to adapt to shifting security demands and operational complexity.

Key players shaping the Turret System Market landscape include BAE Systems, Elbit Systems, and General Dynamics Land Systems. Leading companies in the turret system market are investing heavily in R&D to drive innovation in unmanned and AI-integrated turret technologies. Strategic collaborations with defense ministries and government agencies help secure long-term procurement contracts. To strengthen their competitive position, manufacturers are expanding production capabilities, optimizing modular turret architectures, and incorporating cutting-edge materials to reduce weight while maintaining performance. Mergers, acquisitions, and partnerships also allow players to tap into new regional markets and diversify their product portfolios. Furthermore, companies are focusing on upgrading legacy platforms with next-gen capabilities rather than full replacements, helping them maintain relationships with established defense clients and ensure recurring revenue through lifecycle support and system retrofitting.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the Industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising defense budgets and military modernization

- 3.3.1.2 Technological innovations and automation

- 3.3.1.3 Geopolitical tensions and security threats

- 3.3.1.4 Expansion of security and defense infrastructure

- 3.3.1.5 Diversification of applications

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High development and procurement costs

- 3.3.2.2 Rapid technological obsolescence

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Manned

- 5.3 Unmanned

Chapter 6 Market Estimates and Forecast, By Component, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Turret drive

- 6.3 Turret control

- 6.4 Stabilization unit

Chapter 7 Market Estimates and Forecast, By Platform, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Land

- 7.2.1 Mobile/vehicular

- 7.2.2 Fixed/stationary

- 7.3 Airborne

- 7.3.1 Attack helicopters

- 7.3.2 Fighter aircrafts

- 7.3.3 Special mission aircrafts

- 7.3.4 Unmanned aerial vehicles (UAVs)

- 7.4 Naval

- 7.4.1 Destroyer

- 7.4.2 Frigates

- 7.4.3 Offshore support vessels (Oosts)

- 7.4.4 Corvettes

- 7.4.5 Patrol & mine countermeasure vessels

- 7.4.6 Amphibious vessels

- 7.4.7 Submarines

- 7.4.8 Unmanned surface vehicles (USAs)

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 BAE Systems

- 9.2 Elbit Systems Ltd.

- 9.3 General Dynamics Corporation

- 9.4 Leonardo S.p.A.

- 9.5 Lockheed Martin Corporation

- 9.6 Moog Inc.

- 9.7 Northrop Grumman

- 9.8 RAFAEL Advanced Defense Systems Ltd.

- 9.9 Rheinmetall AG

- 9.10 Thales

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日