|

市場調査レポート

商品コード

1444740

陸上C4ISR:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Land Based C4ISR - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 陸上C4ISR:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 105 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

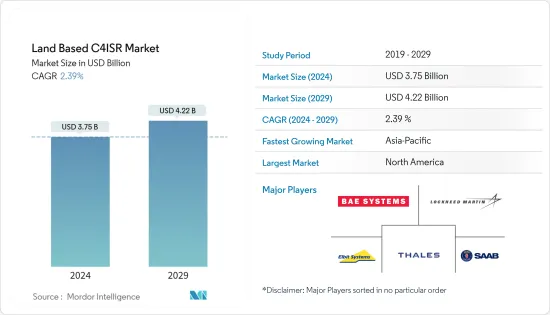

陸上C4ISR市場規模は2024年に37億5,000万米ドルと推定され、2029年までに42億2,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に2.39%のCAGRで成長します。

COVID-19のパンデミックは、C4ISRシステムの一部の重要な部品やコンポーネントに課せられた制限や一時的なコスト増加の結果、生産量の減少を引き起こしたため、世界の陸上設置型C4ISR市場に若干の悪影響を及ぼしました。しかし、着実に増加する防衛費により、先進的なC4ISRシステムの採用が促進され、これが市場の主な推進力となりました。これに関して、世界の国防支出は2021年に2兆米ドルを超えました。

地政学的な緊張と過激派の活動の高まりにより、世界中の国防軍が軍事資産の連携を容易にし、非対称戦争と戦う能力を向上させる統合ソリューションをイントロダクションする方法を模索する中、C4ISRシステムの導入につながりました。地理空間インテリジェンス、無人地上車両(UGV)、地上配備型C2、および展開部隊の状況認識を向上させ、戦場で戦術的優位性を獲得するためのISRシステムを開発する取り組みが、C4ISRシステムの需要の急速な成長を促進しています。脅威検出システムの急速な近代化と、情報を直接入手する競争により、世界中の複数の地域でC4ISRシステムの需要が飛躍的に増加しました。

陸上C4ISR市場動向

C4システムは予測期間中に最高の成長率を示すことが予想されます

C4システム部門は、予測期間中に大幅に成長すると予想されます。この成長は、国防支出の増加と、さまざまな軍事作戦のための指揮、制御、高度な通信システムの調達の増加によるものです。中国による軍事侵略の激化を受けて、米国はC4ISR能力の向上に投資しています。さらに、近隣諸国間の政治紛争、進行中のロシアとウクライナの戦争、中国と台湾の間の緊張の高まりにより、欧州とアジア諸国からの国防支出が増加しました。これらの国は、次世代兵器システムの調達を通じた防衛力の強化に注力しています。例えば、

2022年 4月、米国に本拠を置く防衛メーカーであるノースロップグラマンコーポレーションは、軍事サービスや領域を越えた重要な情報の転送をサポートするために、5G通信技術を使用した新しいデジタル戦闘ネットワークを開発するためにAT&Tと提携しました。この通信システムは、統合全ドメイン指揮制御(JADC2)システムを支援すると期待されています。

2022年 2月初め、ロッキード・マーチン社は、5G通信ネットワークインフラストラクチャのテストベッドを開発するためのプロトタイププロジェクト契約(PPA)を米国国防総省から獲得しました。このテストベッドは、陸、海、空、宇宙、サイバー領域全体で5Gテクノロジーを迅速に実装し、統合することを目的としています。また、領土紛争が続いているため、装甲車両や地上部隊の装備の調達が必要となっており、その結果、陸上電子戦の装備やシステムとともに、より優れた高度な戦術通信リンクに対する需要がさらに高まることが予想されます。したがって、そのようなテクノロジーへの投資は、予測期間におけるこの部門の成長を促進すると予想されます。

アジア太平洋が予測期間中に市場をリードすると予想される

アジア太平洋は、予測期間中に最も高い成長を示すと予測されています。アジア太平洋地域の国々は、国防力の急速な近代化によって根本的な変革を経験しています。中国とインドは現在の国防軍能力の強化に向けて大きく前進しており、それによって陸上配備型C4ISRシステムを含む現代技術を軍隊に強化し統合するために多大な資金とその他の資源を費やしています。例えば、中国は、重要性を強調する現代の戦争の動向への対応として、人民解放軍(PLA)の指揮、統制、通信、コンピューター、諜報、監視、偵察(C4ISR)システムの近代化を引き続き重視しています。迅速な意思決定と情報の共有と処理。人民解放軍は、ますます洗練された兵器を使用して、近距離および遠方の戦場で複雑な統合作戦を指揮できるよう、技術力と組織構造の向上を目指しています。 PLAは現在、統合指揮プラットフォームなどの高度な自動指揮システムを全軍の下位階層の部隊に配備しています。同様のプログラムが地域内の他の軍隊でも実施されており、それによって予測期間中に市場に注目が集まります。

陸上C4ISR業界の概要

陸上C4ISR市場は本質的に適度に細分化されており、いくつかのプレーヤーが市場で大きなシェアを占めています。著名な市場参加者には、Elbit Systems Ltd.、BAE Systems plc、Saab AB、THALES、Lockheed Martin Corporation、およびNorthrop Grumman Corporationなどがあります。ただし、他のメーカーも陸上プラットフォーム用のC4ISRソリューションを提供しています。

C4ISRシステムの技術の進歩と多機能システムの需要により、メーカーは費用対効果の高いソリューションの研究開発への投資を推進しています。有利な政府政策と既存の世界の安全保障シナリオにより、地域と世界の市場プレーヤー間の戦略的協力が促進され、技術力を統合し、高度な地上ベースのC4ISRシステムを共同開発しています。合弁事業(JV)や合併・買収(M&A)により、予測期間中に市場の統合が起こる可能性があります。たとえば、THALESとRaytheon Technologies Corporationの合弁事業であるThalesRaytheonSystemsは、技術を組み合わせて優れたISRシステムを開発し、他の市場プレーヤーに対する競争上の優位性を獲得してきました。ただし、テクノロジーの急速な近代化により、他のプレーヤーが同様の、またはさらに優れた機能を備えた製品を開発することは確実であるため、競争上の優位性は長続きしない可能性があります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- タイプ

- C4システム

- ISR

- 電子戦

- 地域

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他中東およびアフリカ

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- THALES

- Saab AB

- Elbit Systems Ltd.

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- BAE Systems plc

- CACI International Inc.

- Kratos Defense &Security Solutions Inc.

- Sabre Systems Inc.

- L3Harris Technologies Inc.

- Rheinmetall AG

第7章 市場機会と将来の動向

The Land Based C4ISR Market size is estimated at USD 3.75 billion in 2024, and is expected to reach USD 4.22 billion by 2029, growing at a CAGR of 2.39% during the forecast period (2024-2029).

The COVID-19 pandemic had a minor negative impact on the global land-based C4ISR market because it caused production to decline as a result of imposed restrictions and temporary cost increases for some crucial parts and components of C4ISR systems. However, a steadily growing defense expenditure fostered the adoption of advanced C4ISR systems, which was the primary market driver. On this note, the global defense expenditure crossed USD 2 trillion in 2021.

The rise of geopolitical tensions and extremist activities led to the introduction of C4ISR systems, as defense forces around the world looked for ways to adopt integrated solutions that would make it easier for military assets to work together and improve their ability to fight asymmetric wars. Initiatives to develop geospatial intelligence, unmanned ground vehicles (UGVs), land-based C2, and ISR systems to improve the situational awareness of deployed forces and gain a tactical advantage on the battlefield are driving the rapid growth in the demand for C4ISR systems. The rapid modernization of threat detection systems, along with the race to gain information firsthand, has exponentially driven the demand for C4ISR systems across multiple geographies around the world.

Land Based C4ISR Market Trends

C4 Systems Are Anticipated to Showcase Highest Growth Rate During the Forecast Period

The C4 Systems segment is expected to grow significantly during the forecast period. The growth is due to increased defense spending and the rising procurement of command, control, and advanced communications systems for various military operations. Owing to the rising military aggression by China, the US has been investing in improving its C4ISR capabilities. Furthermore, the political disputes among neighboring countries, the ongoing Russia-Ukraine war, and the growing tension between China and Taiwan led to increased defense expenditure from European and Asian countries. These countries are focusing on enhancing their defense capabilities through the procurement of next-generation weapons systems. For instance,

In April 2022, Northrop Grumman Corporation, a US-based defense manufacturer, entered into a partnership with AT&T to develop a new digital battle network using 5G communications technology to support the transfer of critical information across military services and domains. The communication systems are anticipated to aid the Joint All-Domain Command and Control (JADC2) system.

Earlier in February 2022, Lockheed Martin Corporation was awarded a prototype project agreement (PPA) from the US Department of Defense to develop a 5G communications network infrastructure testbed.The testbed will aim to field and integrate 5G technology rapidly across the land, water, air, space, and cyber domains. Also, ongoing territorial conflicts necessitate the procurement of armored vehicles and ground force equipment, which, in turn, is expected to generate more demand for better and more advanced tactical communication links, along with land-based electronic warfare equipment and systems. Hence, investments in such technologies are anticipated to propel the growth of the segment in the forecast period.

Asia-Pacific is Anticipated to Lead the Market During the Forecast Period

Asia-Pacific is projected to show the highest growth during the forecast period. Countries in Asia-Pacific are undergoing a radical transformation driven by the rapid modernization of their defense forces. China and India are taking huge strides toward strengthening the current capabilities of their defense forces and are thereby expending significant financial and other resources to empower and integrate their armies with modern technologies, including land-based C4ISR systems. For instance, China continues to place a high priority on modernizing the People's Liberation Army's (PLA's) command, control, communications, computers, intelligence, surveillance, and reconnaissance (C4ISR) system as a response to trends in modern warfare that emphasize the importance of rapid decision-making and information sharing and processing. The PLA is seeking to improve its technological capabilities and organizational structure to command complex joint operations on near and distant battlefields with increasingly sophisticated weaponry. The PLA is currently fielding advanced automated command systems, such as its Integrated Command Platform, with units at lower echelons across the force. Similar programs have been undertaken by other armed forces in the region, thereby driving the market into focus during the forecast period.

Land Based C4ISR Industry Overview

The land-based C4ISR market is moderately fragmented in nature, with several players holding significant shares in the market. Some prominent market players are Elbit Systems Ltd., BAE Systems plc, Saab AB, THALES, Lockheed Martin Corporation, and Northrop Grumman Corporation. However, several other manufacturers provide C4ISR solutions for the land platform.

Technological advancements in C4ISR systems and the demand for multi-functional systems are propelling the investments of manufacturers in the research and development of cost-effective solutions. Favorable government policies and the existing global security scenario are fostering strategic collaboration between regional and global market players to merge their technological prowess and jointly develop sophisticated land-based C4ISR systems. Consolidation of the market may occur during the forecast period on account of joint ventures (JVs) and mergers and acquisitions (M&As). For instance, ThalesRaytheonSystems, a joint venture between THALES and Raytheon Technologies Corporation, has been combining technologies to develop superior ISR systems and gain a competitive advantage over the other market players. However, with the rapid modernization of technology, the competitive advantage may be short-lived, as other players would surely develop products with similar or even superior capabilities.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 C4 Systems

- 5.1.2 ISR

- 5.1.3 Electronic Warfare

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Rest of Latin America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 United Arab Emirates

- 5.2.5.3 South Africa

- 5.2.5.4 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 THALES

- 6.2.2 Saab AB

- 6.2.3 Elbit Systems Ltd.

- 6.2.4 Lockheed Martin Corporation

- 6.2.5 Northrop Grumman Corporation

- 6.2.6 BAE Systems plc

- 6.2.7 CACI International Inc.

- 6.2.8 Kratos Defense & Security Solutions Inc.

- 6.2.9 Sabre Systems Inc.

- 6.2.10 L3Harris Technologies Inc.

- 6.2.11 Rheinmetall AG