|

市場調査レポート

商品コード

1910678

原子力発電:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Nuclear Power - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 原子力発電:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

概要

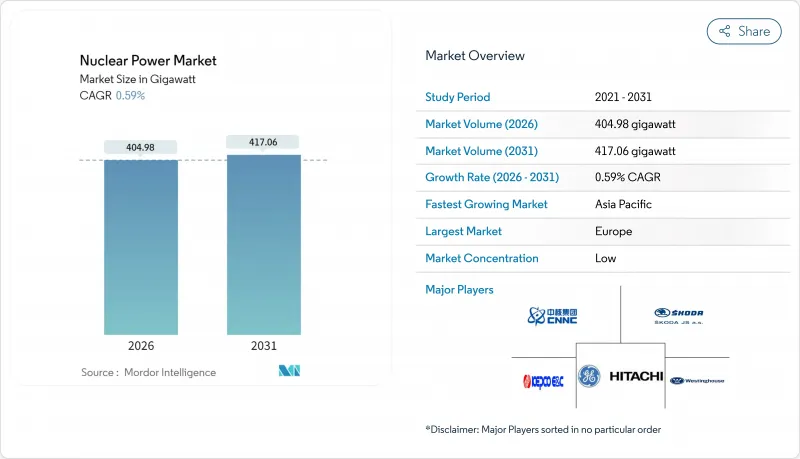

原子力発電市場は、2025年の402.60ギガワットから2026年には404.98ギガワットへ成長し、2026年から2031年にかけてCAGR0.59%で推移し、2031年までに417.06ギガワットに達すると予測されています。

持続的な設備容量の増加は依然として緩やかな水準に留まっていますが、この分野では構造的な転換が進んでおります。小型モジュール炉(SMR)が開発段階から商業展開へと移行する一方で、寿命延長プログラムが既存のベースロード発電を支えるという構造です。開発事業者は建設リスクを軽減するため工場生産モジュールに注力する一方、従来のギガワット級プロジェクトは上昇する資本コスト、長期化するリードタイム、厳格化する資金調達ルールに直面しております。地域別の動向としては、欧州の膨大な既存設備、アジア太平洋地域の急速な建設ペース、北米の運転期間延長への注力が特徴的です。また、産業脱炭素化のニーズからも機会が生まれています。高温の原子力プロセス熱を利用することで、鉄鋼、セメント、化学産業における石炭や天然ガスボイラーを代替できる可能性があります。

世界の原子力発電市場の動向と展望

クリーンなベースロード電力への需要増加

電力部門の脱炭素化目標は引き続き厳格化されており、系統運用者は信頼性を損なうことなく変動性再生可能エネルギー源を大量に統合することに苦労しています。そのため、政府は特に電力使用量が年間15~20%増加するデータセンター集積地向けに、24時間365日稼働するカーボンフリー電源として原子力を見直しています。かつて原子力発電の段階的廃止を計画していた日本や韓国など複数の経済圏では、エネルギー安全保障を確保するため方針を転換しています。容量価値支払いと付帯サービス収益が原子力事業計画に組み込まれるようになり、太陽光や風力との顕在的なコスト差が縮小しています。これにより原子力市場は、スポット電力価格が変動し続ける状況下でも政策的な下支えを確保しています。同時に、規制当局はより厳格な安全マージンを要求しており、これによりライセンシング審査期間が延長される一方、公衆の受容性も強化されています。

運転期間延長・出力向上プログラム

事業者は、40年経過した原子炉を60年、さらには80年稼働させるコストが1kWあたり500~1,000米ドルであるのに対し、新規建設には1kWあたり6,000~1万2,000米ドルが必要であることを認識しています。米国原子力規制委員会はこれまでに95件の運転延長認可を承認しており、フランスでは494億ユーロを投じた大規模改修プロジェクトにより格納容器の強化と主要機器の交換が進められています。タービンや炉心内部機器の出力向上は通常、1基あたり4~7%の出力増加をもたらし、新規立地を巡る争いを伴わずに原子力市場を拡大する最も迅速な手段となっています。事業者様には、原子炉圧力容器の脆化や計装機器の陳腐化への対応が依然として求められます。60年を超える規制の不確実性は長期計画の足かせとなりますが、多くの電力会社様は運転期間延長を、2030年代の次世代原子炉導入への橋渡しと捉えております。

コスト超過と資金調達課題

ジョージア州のヴォグル3-4号機拡張プロジェクトは当初予算の2倍以上となる350億米ドルに膨れ上がり、英国のヒンクリーポイントCは現在430億米ドル近くに達しています。こうした超過は、サプライチェーンの不足、建設中の設計変更、そして数十年にわたる新規建設の停滞による熟練労働者の流出に起因しています。このため、融資機関は資金提供に際し、政府保証、規制された資産担保型モデル、あるいは長期電力購入契約を要求します。開発業者は工期短縮のためモジュール化を推進していますが、初号機となる小型モジュール炉(SMR)は依然として信頼性のあるコスト曲線を示す必要があります。政府の融資保証や税制優遇措置はリスクを軽減しますが、民間主導の原子力プロジェクトは依然として稀です。

セグメント分析

加圧軽水炉は2025年の総容量の74.02%を占め、原子力市場の基幹としての役割を確固たるものにしております。しかしながら、高速増殖炉は中国の600MWe級CFR-600やインドの試作炉プログラムを牽引役として、2031年までにCAGR19.4%の軌道に乗っています。ガス冷却炉や溶融塩炉の概念は依然としてパイロット段階にありますが、その高温処理能力が産業用熱需要顧客の関心を集めています。

したがって原子力市場では、軽水炉設計が中期的にシェアを維持する一方、実証用高速炉が閉鎖型燃料サイクルの知識基盤を構築します。規制当局はナトリウム・鉛冷却システムへの理解を深めていますが、商業化資金調達は安全性と経済性を実証する早期の成功事例に依存します。CFR-600が性能目標を達成すれば、増殖炉技術は2030年代に原子力市場で相当なシェアを獲得する可能性があります。

中規模500~1,000MWeユニットは2025年時点で設置容量の48.12%を占め、成熟した送電網を有する国々において引き続き優先選択肢となります。500MWe未満の小型炉はCAGR19.2%で拡大が見込まれており、これはリスク資本を低減するモジュール式増設への電力会社の関心を反映しています。20MWe未満のマイクロ炉は鉱業や防衛用途をターゲットとしており、オフグリッド環境での耐障害性を提供します。

小型原子炉の経済性において工場生産は極めて重要です。ベンダー各社は標準化を推進しており、10~12基の稼働後には学習曲線効果によるコスト低下がSMR市場規模の拡大に寄与します。一方、1,000MWeを超える大型原子炉はコスト面での逆風と小規模国における系統連系制限に直面しており、中国・インド以外での新規受注は抑制されています。

原子力市場レポートは、原子炉タイプ(加圧軽水減速冷却炉、高速増殖炉など)、原子炉規模(大型、中型、小型)、燃料タイプ(低濃縮ウランなど)、用途別(系統連系電力、工業プロセス用熱・蒸気など)、エンドユーザー別(電力会社・独立系発電事業者、工業・石油化学など)、地域別(欧州、アジア太平洋など)に分析しております。

地域別分析

欧州は2025年においても原子力市場で最大の39.35%のシェアを維持しており、これはフランス国内の電力の65%を供給する56基の原子炉群に支えられています。欧州連合(EU)はグリーンタクソノミーにおいて原子力エネルギーを移行資産として位置付け、持続可能な資金調達経路を開放しています。しかしながら、運転期間延長費用や福島事故後の安全対策強化が事業者の財務を圧迫しており、2023年のドイツの原子力発電所閉鎖により中欧はフランスからの輸入電力への依存度が高まっています。英国では3.2ギガワットのヒンクリーポイントC原子力発電所が推進され、さらに6基の欧州加圧水型炉(EPR)の導入が検討されており、これにより2050年まで国内の原子力技術を維持する見込みです。

アジア太平洋地域は6.6%という最速のCAGRを達成しており、中国で建設中の24基の原子炉計画と、インドの国産重水炉(PHWR)および高速炉プログラムが牽引しています。中国は原子力拡大を2060年までのカーボンニュートラル公約と整合させ、2030年までに120ギガワット(GW)を目標としています。日本では段階的な再稼働により稼働率は向上しているもの、国民の懐疑的な見方が制約要因となっています。一方、韓国は28基の原子炉を維持し、アラブ首長国連邦へAPR-1,400ユニットを輸出しています。ベトナムやインドネシアなどの新興経済国では実現可能性調査が進められていますが、原子力市場への参入には資金調達と規制整備が依然として障壁となっています。

北米では運転延長と選択的新規建設が主流です。米国では総発電量の20%、無炭素電力の50%を原子力に依存。運転延長により老朽化プラントを維持しつつ、連邦税額控除と融資保証によりアイダホ州とワイオミング州で小型モジュール炉(SMR)プロジェクトを推進しています。カナダではCANDU炉の改修を進め、2024年にはダーリントン2号機から881MWeを追加。遠隔地の北極圏コミュニティや重油採掘現場向けの小型モジュール炉実証も推進中です。メキシコはラグナ・ベルデ2基の運転を継続する一方、新規建設の見通しは立っておりません。この地域全体において、先進炉の導入経路は高濃縮ウラン(HALEU)の供給と簡素化されたライセンシング手続きにかかっています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3か月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- クリーンなベースロード電力に対する需要の増加

- 寿命延長及び出力向上プログラム

- 先進小型モジュール炉(SMR)の商業化

- 産業脱炭素化プロセス-熱需要

- 原子力由来水素・アンモニア事業

- 原子力発電によるデータセンターおよび船舶用途の出現

- 市場抑制要因

- コスト超過と資金調達上の課題

- 低コスト再生可能エネルギーとの競合

- 高濃縮ウラン燃料の供給ボトルネック

- 輸出管理及び拡散監視

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の激しさ

第5章 市場規模と成長予測

- 反応炉タイプ別

- 加圧軽水減速冷却炉(PWR)

- 加圧重水減速冷却炉(PHWR)

- 沸騰水型軽水冷却・減速炉(BWR)

- ガス冷却・黒鉛減速炉(GCR)

- 高温ガス炉(HTGR)

- 軽水冷却・黒鉛減速原子炉(LWGR)

- 高速増殖炉(FBR)

- その他

- リアクトルサイズ別

- 大型(1,000 MWe以上)

- 中型(500~1,000 MWe)

- 小型(500 MWe未満;小型モジュール炉(SMR)およびマイクロリアクトルを含む)

- 燃料タイプ別

- 低濃縮ウラン(U-235 5%未満)

- 高アッセイLEU(U-235 5~20%)

- 混合酸化物燃料(MOX)

- トリウム系燃料

- 用途別

- 系統連系電力

- オフグリッド/遠隔地電化

- 工業プロセス熱および蒸気

- 海水淡水化および地域暖房

- 防衛・軍事基地

- エンドユーザーセクター別

- 公益事業および独立系発電事業者(IPP)

- 産業および石油化学

- 鉱業および遠隔操作

- 政府・防衛

- 研究機関

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- スウェーデン

- スペイン

- ウクライナ

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- エジプト

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動き(M&A、合弁事業、資金調達、電力購入契約)

- 市場シェア分析(主要企業の市場順位・シェア)

- 企業プロファイル

- Electricite de France SA(EDF)

- Rosatom State Atomic Energy Corporation

- China National Nuclear Corporation(CNNC)

- Westinghouse Electric Company LLC

- GE-Hitachi Nuclear Energy

- Framatome SA

- Mitsubishi Heavy Industries Ltd

- Korea Hydro & Nuclear Power/KEPCO E&C

- BWX Technologies Inc.

- Bechtel Corporation

- Doosan Enerbility Co. Ltd

- Fluor Corporation(NuScale)

- SKODA JS a.s.

- Holtec International

- TerraPower LLC

- Rolls-Royce SMR Ltd

- X-Energy LLC

- General Fusion Inc.

- Ontario Power Generation

- Babcock International Group

- Bilfinger SE

- Duke Energy Corporation

- Japan Atomic Power Company

- Ansaldo Nucleare