|

市場調査レポート

商品コード

1405728

在宅輸液療法 - 市場シェア分析、産業動向・統計、2024年~2029年成長予測Home Infusion Therapy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 在宅輸液療法 - 市場シェア分析、産業動向・統計、2024年~2029年成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 111 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

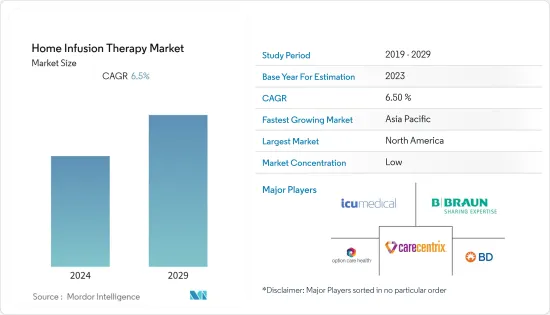

世界の在宅輸液療法市場規模は、2024年の229億米ドルから2029年には314億米ドルに成長し、予測期間(2024年~2029年)のCAGRは6.50%と予測されます。

主なハイライト

- 2020年にCOVID-19の症例が増加するにつれ、代替部位ソリューションの使用需要が高まり、在宅および専門輸液プロバイダーが患者支援に重要な役割を果たしました。しかし、主要市場参入企業による取り組みが市場成長を高めると予想されました。例えば、エイタン・メディカルは2021年7月、顧客基盤を拡大するためにドイツにDACH地域の新オフィスを開設しました。同社のSapphire輸液システムはEU MDR認証を取得し、欧州全域の病院や在宅ケア環境の臨床医にサービスを提供しています。このポンプは、様々な臨床使用事例に対応するため、幅広い治療法を提供できるように設計されています。同様に、アメディシスは2021年1月、オプション・ケア・ヘルスと協力し、COVID-19輸液療法を社会的弱者に提供しました。このような取り組みにより、市場の成長が期待されます。

- 市場の成長は、在宅輸液療法によってもたらされる患者の転帰の改善、コスト効率、患者の利便性に起因します。変形性関節症、麻痺、糖尿病などの運動能力の低下を患うベビーブーマー世代の増加は、在宅輸液療法の需要を押し上げると思われます。入院期間を短縮するニーズの高まりが市場開拓の原動力になると予想されます。アポモルヒネの持続皮下(SC)注入はパーキンソン病(PD)に対する有効な治療法であり、皮下デリバリーを用いたPD治療にはさまざまな製剤が利用可能です。このように、PDの負担の増加に伴い、皮下輸液療法の需要が高まっています。例えば、パーキンソン財団による2022年のデータ更新によると、米国では毎年約9万人がPDと診断されており、2030年までに国内で120万人近くがPDと共存すると推定されています。また、上記の出典にあるように、北米では過去10年間にPDの罹患率が増加しており、女性よりも男性の方がPDの罹患率が高いと推定されています。その結果、自宅やその他のヘルスケア環境で輸液療法を実施する技術が開発されており、これも市場拡大を後押しすると予想されます。病院では、EHR接続、薬剤ライブラリ、投薬安全ソフトウェアなどの魅力的な機能を備えたスマート輸液ポンプの導入が急速に進んでいるにもかかわらず、在宅輸液業者の大半は依然として従来型の輸液ポンプを使用しています。しかし、特に先進諸国では、その需要の増加により、機器のアップグレードの傾向が強まっています。

- さらに2021年12月、バクスター・インターナショナルはヒルロムの買収を完了しました。この買収により、同社は地理的なフットプリントを拡大し、患者ケアの強化、コスト削減、ワークフローの効率化を実現する医療機器技術を統合します。さらに2021年3月、テルモと遠隔患者モニタリング・ソフトウェアおよびモバイル・アプリのGlooko社は、新たな糖尿病データ・ソリューションを世界に提供するための技術統合を発表しました。この提携により、テルモの糖尿病治療機器からのデータをGlookoの糖尿病データ管理プラットフォームdiasendに統合することが可能になります。同様に、2021年6月、アデュカヌマブ(Aduhelm)は米国食品医薬品局(FDA)からアルツハイマー病治療薬として早期承認を取得しました。これはアルツハイマー病の根本的な生物学に対処する初のFDA承認輸液療法です。このように、このような買収や製品の上市は、予測期間中の市場の成長を押し上げると予想されます。しかし、輸液ポンプに関連する高コストが予測期間中の事業成長を妨げる可能性があります。

在宅輸液療法市場の動向

抗感染療法が在宅輸液療法市場を独占

- 抗感染療法分野は、予測期間を通じて世界の在宅輸液療法市場を独占するとみられます。抗感染症療法は、最も処方される在宅輸液療法の1つです。しかし、このような療法には本質的なリスクが少なくなく、慎重な患者選択基準、構造化されたフォローアッププロセス、患者教育の重視と相まって、チームアプローチによってリスクを軽減することができます。

- 感染症治療薬市場の成長の主な要因は、様々な政府機関や非営利団体による啓発活動の高まり、感染症の流行の増加、資金調達の増加と研究開発活動の活発化です。

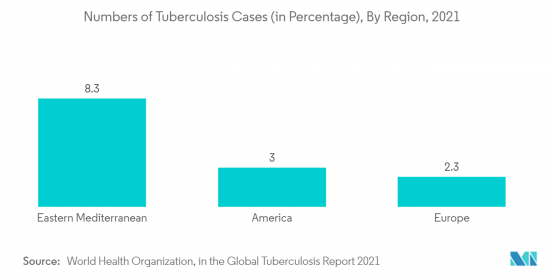

- 例えば、世界保健機関(WHO)が発表した「Global Tuberculosis Report 2021」のデータによると、結核患者の大半はWHOの地域である東南アジア(43%)、アフリカ(25%)、西太平洋(18%)で発見されたと記載されています。同様に、2021年に発表されたWHOのデータによると、マラリア感染の95%がサハラ以南のアフリカで発生しており、この地域は今後もこの病気による負担が大きくなりそうです。このように、先進国市場および新興国市場全体における複数の感染症による負担の増加が、調査対象市場の原動力になると予想されます。

- このように、各国における感染症負担の増加や研究開発活動の活発化は、抗感染症療法に対する需要を増加させ、それによって同分野の成長を後押しすると考えられます。

北米が市場を独占し、予測期間中も同地域の支配が続くと予想される

- 北米は在宅輸液療法市場の主要地域の1つです。慢性疾患の増加、治療費、技術の進歩、製品の発売などの要因が存在するためであり、これらの要因が地域の成長を促進すると予想されます。例えば、2021年から更新された米国がん学会の推計によると、米国だけでも2020年に約180万人のがん患者が新たに報告されました。

- 乳がん、肺がん、前立腺がん、大腸がん、膀胱がん、皮膚がんは、米国で最も流行している悪性腫瘍です。さらに、安価なコストと患者の移動性の向上により、急性期医療から在宅医療への移行が進んでおり、これがさらなる拡大に拍車をかけると予想されています。地域限定商品の需要も、ヘルスケア産業の改善や高度化する医療用品の使用によって後押しされています。

- 一方、在宅医療分野では、在宅輸液に十分な保険が適用されるため、市場の成長が見込まれています。Option Care Enterprises、CHI Healthなど複数の企業が在宅医療現場で輸液療法サービスを提供しており、その費用も保険でカバーされています。

- 2021年5月、スミスメディカルとIvenix, Inc.は、包括的な輸液管理ソリューション群を米国市場で提供するための提携契約を発表しました。この提携により、患者の安全性を向上させる輸液管理の進化が期待されます。このようなパートナーシップは、この地域における市場の成長を後押しすると期待されています。

- このように、上記のような要因によって市場の成長が期待されます。

在宅輸液療法産業の概要

在宅輸液療法市場は競争が激しく、世界企業だけでなく地域企業も複数存在します。技術の進歩により、中小企業は市場浸透に注力し、市場シェアを獲得しています。同市場の主要企業には、B. Braun Melsungen AG、ICU Medica、Becton Dickinson and Company、Option Care Health Inc.、CareCentrix Inc.などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 移動能力の低下に悩む団塊世代の増加

- 院内感染の増加

- 技術の進歩に伴う在宅ヘルスケアの採用増加

- 市場抑制要因

- 輸液ポンプの高コスト

- 輸液ポンプに関連する安全性の問題

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模)

- 製品別

- 輸液ポンプセット

- アクセサリー・消耗品

- 用途別

- 総合非経口栄養療法

- 抗感染療法

- 経腸栄養

- 水分補給療法

- 化学療法

- IVIg/特殊医薬品

- その他の用途

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- B. Braun Melsungen AG

- Baxter International

- Becton Dickinson and Companies

- Catholic Health Initiatives

- Community Surgical Supply

- Eli Lilly and Company

- Fresenius Kabi

- ICU Medical Inc.

- McKesson Medical-Surgical Inc.

- McLaren Health Care

- Nipro Corporation

- Option Care Health Inc.

- Smiths Medical

- Sutter Health

- Terumo Corporation

第7章 市場機会と今後の動向

The global home infusion therapy market size is expected to grow from USD 22.9 billion in 2024 to USD 31.4 billion by 2029, at a CAGR of 6.50% during the forecast period (2024-2029).

Key Highlights

- As cases of COVID-19 increased in 2020, the use of alternate site solutions rose in high demand, and home and specialty infusion providers played a critical role in supporting patients. However, initiatives by key market players were expected to increase market growth. For instance, in July 2021, Eitan Medical opened a new office for the DACH region located in Germany to expand its customer base. Its Sapphire infusion system was EU MDR certified and served clinicians in hospitals and home care environments across Europe. The pump was designed to deliver a wide range of therapies for varied clinical use cases. Similarly, in January 2021, Amedisys collaborated with Option Care Health to deliver COVID-19 infusion therapy to the vulnerable population. Thus, such initiatives were expected to increase market growth.

- The growth of the market is attributed to improved patient outcomes, cost-efficiency, and patient convenience provided by home infusion therapy. The growing number of baby boomers suffering from decreased mobility profiles such as osteoarthritis, paralysis, and diabetes will boost the demand for home infusion therapy. The rising need to reduce the duration of inpatient stays is anticipated to fuel the market development. Continuous subcutaneous (SC) apomorphine infusion is an effective therapy for Parkinson's disease (PD), and various drug formulations are available for treating PD using the subcutaneous mode of delivery. Thus, with the increasing burden of PD, the demand for subcutaneous infusion therapy is rising. For instance, as per the 2022 data update by the Parkinson's Foundation, approximately 90,000 people are diagnosed with PD annually in the United States, and nearly 1.2 million people in the country are estimated to be living with PD by the year 2030. In addition, as per the source above, the incidence of PD has increased in North America in the past decade, and it is estimated that men are associated with a higher incidence of PD than women. As a result, techniques for administering infusion therapy at home or in other healthcare settings have been developed, which is also anticipated to support market expansion. The majority of home infusion providers still use conventional infusion pumps despite hospitals quickly adopting smart infusion pumps with fascinating features like EHR connectivity, drug libraries, and medication safety software. However, there has been a growing trend for the up-gradation of equipment owing to its increasing demand, especially in developed countries.

- Furthermore, in December 2021, Baxter International completed the acquisition of Hillrom. This acquisition will help the company broaden its geographic footprint and integrate medical device technology that will enhance patient care, lower costs, and increase workflow efficiency. Moreover, in March 2021, Terumo and Glooko, a remote patient monitoring software and mobile apps company, announced technological integration to deliver new diabetes data solutions together globally. The partnership will allow the integration of data from Terumo's diabetes care devices into Glooko'sdiasend diabetes data management platform. Similarly, in June 2021, Aducanumab (Aduhelm) received accelerated approval as a treatment for Alzheimer's disease from the United States Food and Drug Administration (FDA). This is the first FDA-approved infusion therapy to address the underlying biology of Alzheimer's disease. Thus, such acquisitions and product launches are expected to boost the growth of the market over the forecast period. However, the high cost associated with the infusion pumps may hamper business growth during the forecast period.

Home Infusion Therapy Market Trends

Anti-infective Therapy Dominates the Home Infusion Therapy Market

- The anti-infective therapy segment is expected to dominate the global home infusion therapy market through the forecast period. Anti-infective therapy is one of the most prescribed home infusion therapies. However, there are few risks intrinsic to such therapy, which can be reduced by a team approach, coupled with careful patient selection criteria, a structured follow-up process, and an emphasis on patient education.

- The major factors for the growth of the infectious disease drugs market are the rising awareness activities by various government and non-profit organizations, the increasing prevalence of infectious diseases, and the rising funding and increasing research and development activities.

- For instance, according to the data published by the World Health Organization (WHO) in the Global Tuberculosis Report 2021, stated that the majority of tuberculosis cases were discovered in the WHO regions of South-East Asia (43%), Africa (25%), and the Western Pacific (18%). Similarly, according to the WHO data published in 2021, with 95% of all malaria infections occurring in Sub-Saharan Africa, this region is likely to continue to experience a heavy burden from the disease. Thus, the rise in the burden of several infectious diseases across developed and emerging markets is expected to drive the market studied.

- Thus, the increasing burden of infectious diseases in various countries and increasing research and development activities are likely to increase the demand for anti-infective therapy, thereby boosting the segment's growth.

North America Dominates the Market and the Region is Expected to Continue the Same during the Forecast Period

- North America is one of the major regions in the home infusion therapy market, owing to the presence of factors such as the increasing prevalence of chronic diseases, treatment costs, technological advancements, and product launches, which are expected to drive regional growth. For instance, according to the estimates of the American Cancer Society updates from 2021, in the United States alone, there were around 1.8 million new cancer cases reported in 2020.

- Breast cancer, lung cancer, prostate cancer, colorectal cancer, bladder cancer, and skin cancer are the most prevalent malignancies in the United States. Furthermore, due to cheap costs and improved patient mobility, there is a growing migration from acute care to home care settings, which is anticipated to spur additional expansion. The demand for regional goods is also being boosted by improvements in the healthcare industry and the use of increasingly sophisticated medical items.

- On the other side, the market has growth prospects in the home healthcare segment owing to sufficient insurance coverage for home infusion. Several companies, such as Option Care Enterprises, CHI Health, etc., provide infusion therapy services in home healthcare settings, and the cost is also covered by insurance coverage.

- In May 2021, Smiths Medical and Ivenix, Inc. announced a partnership agreement to offer a comprehensive suite of infusion management solutions in the United States market. This partnership is expected to evolve infusion management to improve patient safety. Such partnerships are expected to bolster the growth of the market in this region.

- Thus, the abovementioned factors are expected to increase market growth.

Home Infusion Therapy Industry Overview

The market for home infusion therapy is highly competitive and consists of global as well as several regional players. Due to technological advancements, small and mid-sized companies are focusing on market penetration to grab market share. The major players in the market include B. Braun Melsungen AG, ICU Medica, Becton Dickinson and Company, Option Care Health Inc., and CareCentrix Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Number of Baby Boomers Suffering From Decreased Mobility

- 4.2.2 Growing Incidence of Hospital-acquired Infections

- 4.2.3 Increasing Adoption of Home Healthcare Coupled with Technological Advancements

- 4.3 Market Restraints

- 4.3.1 High Cost of Infusion Pumps

- 4.3.2 Safety Issues Associated with Infusion Pumps

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size By Value- USD)

- 5.1 By Product

- 5.1.1 Infusion Pump Sets

- 5.1.2 Accessories and Consumables

- 5.2 By Applications

- 5.2.1 Total Parenteral Nutrition

- 5.2.2 Anti-infective Therapy

- 5.2.3 Enteral Nutrition

- 5.2.4 Hydration Therapy

- 5.2.5 Chemotherapy

- 5.2.6 IVIg/Specialty Pharmaceuticals

- 5.2.7 Other Applications

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 B. Braun Melsungen AG

- 6.1.2 Baxter International

- 6.1.3 Becton Dickinson and Companies

- 6.1.4 Catholic Health Initiatives

- 6.1.5 Community Surgical Supply

- 6.1.6 Eli Lilly and Company

- 6.1.7 Fresenius Kabi

- 6.1.8 ICU Medical Inc.

- 6.1.9 McKesson Medical-Surgical Inc.

- 6.1.10 McLaren Health Care

- 6.1.11 Nipro Corporation

- 6.1.12 Option Care Health Inc.

- 6.1.13 Smiths Medical

- 6.1.14 Sutter Health

- 6.1.15 Terumo Corporation