|

市場調査レポート

商品コード

1405712

装甲車調達・アップグレード:市場シェア分析、産業動向・統計、成長予測、2024年~2029年Armored Vehicle Procurement and Upgrade - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 装甲車調達・アップグレード:市場シェア分析、産業動向・統計、成長予測、2024年~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

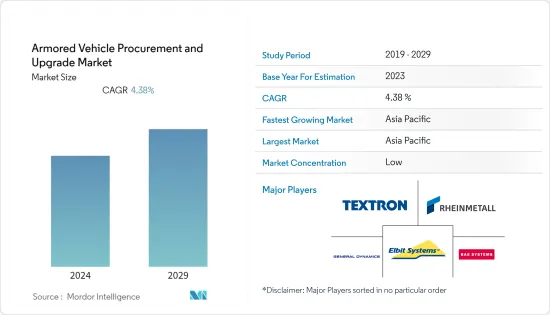

装甲車調達・アップグレード市場は2024年に66億6,000万米ドルと評価され、2029年には82億6,000万米ドルに達すると予測され、予測期間中のCAGRで4.38%の成長が見込まれます。

国家および地域の安全保障に対するニーズがますます高まる中、インド、英国、フランス、米国などの国々が、調査対象市場の主要な中心国になると予想されます。これらの国々の軍事費の増大は、増大する需要を満たすためにこれらの車両の調達に巨額を費やす自由を軍に与え、この点で役立つと予想されます。

広大な陸上国境を持つ国々は、装甲車の有利な市場として浮上しています。陸上車両の調達は、特にアジア太平洋と欧州で増加しています。その背景には、近隣諸国間の政治的緊張の高まりと、この地域における敵対的活動の増加があります。加えて、こうした要因により、陸上車両に最新技術を取り入れる必要性が高まっています。ひいては、アップグレードやレトロフィット活動の主要な推進力となっています。

既存の装甲車をアップグレードする需要は、兵器システム、通信、その他車両保護や兵器庫に関連する新素材の開発によって誘発されます。装甲のアップグレードと改修の分野で市場機会が生まれると予想されます。

装甲車調達・アップグレード市場動向

歩兵戦闘車(IFV)セグメントが市場シェアを独占

IFVに対する需要は、高い火力を持つ車両への要求から、世界中の軍隊で最近増加しています。IFVはMBTよりも安価で、メンテナンスも容易です。また、IFVはMBTよりも高い機動性を含むように設計されています。さらに、IFVはAPCのような人員保護も可能で、射撃能力も高いため、APCの代用として使用されています。人気の高まりに後押しされ、最近ではIFVの調達やアップグレードが増加しています。例えば、英国陸軍は、エイジャックス(装甲騎兵)およびボクサー(機械化歩兵)車両による装甲車両の近代化を進めています。Nasmyth Group Limitedは、ボクサー・プログラムに精密機械加工・製造部品を提供する契約を獲得しました。エイジャックスは完全にデジタル化された先進的な陸上車両で、英国陸軍の将来の装甲車両に変革をもたらします。エイジャックス車両システムは、強化された殺傷力、機動性、生存性、全天候型インテリジェンス、監視、目標捕捉、認識能力を提供します。2022年、エイジャックス車両は騒音と振動のテストを受け、2023年に最初の車両納入が予定されています。

予測期間中、アジア太平洋地域が市場を独占すると予測される

地域別では、アジア太平洋地域が2023年に最も高い市場シェアを占めました。同地域はまた、中国やインドなどの国々からの需要増加に牽引され、予測期間中に最も高いCAGRで推移すると予測されています。中国の生産能力は、装甲兵員輸送車、突撃車両、砲兵システムおよび砲弾、防空砲兵システム、主戦闘戦車および軽戦闘戦車など、地上システムのほぼすべてのカテゴリーで進んでいます。中国北方工業集団公司(Norinco)はここ数年、国産装甲車の増産と販売に力を入れています。これらの車両は、寿命を延ばすための更新が必要です。そのため、中国では、改修・近代化市場が大きな成長を遂げると予想されています。さらにインドも、国境を接する国々との問題から装甲車の戦力を増強しています。老朽化した装甲車の近代化が大きな焦点となっています。例えば、マヒンドラ・ディフェンス・システムズ(MDS)は2021年3月、インド国防省(MoD)から1億2,740万米ドルの契約を獲得し、インド陸軍向けに1300台の装甲戦術車(LSV)を納入しました。マヒンドラの装甲戦術車は、機関銃、自動擲弾発射機、対戦車誘導ミサイルの運搬媒体として利用されます。

同様に2021年12月、オーストラリアはハンファ・ディフェンスに対し、オーストラリア陸軍向けに自走榴弾砲30基と装甲弾薬補給車15台、軍用車両を納入する10億米ドルの契約を発注しました。さらに、2023年7月には、オーストラリア陸軍がハンファ防衛に60億米ドルの契約を発注し、ラインメタルのライバルである歩兵戦闘車「リンクス」よりもハンファの「レッドバック」IFVを選択しました。このような計画により、今後数年間、アジア太平洋市場全体の見通しが高まると予想されます。

装甲車調達・アップグレード産業の概要

装甲車調達・アップグレード市場は断片化されており、多くの世界のプレーヤーやローカルプレーヤーが製造、MRO、アップグレード能力で競争しています。General Dynamics Corporation、BAE Systems plc、Rheinmetall AG、Textron Inc.、Elbit Systems Ltd.などが、この市場における著名なプレーヤーです。この市場では、過去10年間に地元企業の数が増加しました。アジア太平洋、中東・アフリカでは装甲車両の老朽化が進んでおり、これらの地域の現地プレーヤーが能力を開発するのに必要な機会を与え、現地市場で大きなシェアを獲得するのに役立った。各国は現在、独自の第3世代および第4世代MBTやその他の装甲車を現地生産することができます。このような競合環境において、世界プレイヤーは、より高い収益を享受している米国と欧州連合(EU)以外の主要プレイヤーであり続けるために、政策と納品約束を改善する必要に迫られています。また、今後数年間は、世界プレーヤーが地元メーカーと競争するために価格を引き下げる可能性もあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場の課題と抑制要因

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 車両タイプ

- 装甲兵員輸送車(APC)

- 歩兵戦闘車(IFV)

- 耐地雷・伏撃防護車両(MRAP)

- 主力戦車(MBT)

- その他

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- トルコ

- 南アフリカ

- その他中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- General Dynamics Corporation

- Rheinmetall AG

- BAE Systems plc

- Textron Inc.

- Elbit Systems Ltd.

- RUAG International Holding Ltd.

- KNDS N.V.

- Oshkosh Corporation

- THALES

- The CMI Group, Inc.

- FNSS Savunma Sistemleri A.S.

- IVECO S.p.A

- BMC Otomotiv Sanayi ve Ticaret A.S.

- Streit Group

第7章 市場機会と今後の動向

The Armored Vehicle Procurement and Upgrade Market is valued at USD 6.66 billion in 2024 and is expected to reach USD 8.26 billion by 2029, registering a CAGR of 4.38% during the forecast period.

With the ever-increasing need for national and regional security, countries such as India, the United Kingdom, France, and the United States are anticipated to be the primary centers in the market studied. Growing military expenditure of these countries is expected to help in this regard by giving freedom to the militaries to spend huge amounts for the procurement of these vehicles in order to satisfy the increasing demand.

Countries with vast land-based borders are emerging as lucrative markets for armored vehicles. The procurement of land-based vehicles is increasing, particularly in Asia-Pacific and Europe. It is due to the growing political tensions between the neighboring countries and increasing hostile activities in the regions. In addition, these factors are increasing the need for incorporating the latest technologies into the land vehicles. It, in turn, is a major driver for upgrade and retrofit activities.

The demand for upgrading existing armored vehicles will be triggered by the development of weapon systems, communication, and other new materials related to vehicle protection and armory. It is expected to generate market opportunities in the area of armor upgrades and retrofitting.

Armored Vehicle Procurement & Upgrade Market Trends

The Infantry Fighting Vehicle Segment to Dominate Market Share

The demand for IFVs increased in the recent past from armies worldwide due to the requirement for vehicles with high firepower. IFVs are less expensive and easier to maintain than MBTs. Also, IFVs are designed to include higher mobility than MBTs. In addition, IFCs also provide personnel protection like APCs with greater firing capabilities, and thus, they are used as substitutes for APCs. Driven by their growing popularity, there is an increase in the procurement and upgrades of IFVs in recent times. For instance, the UK Army is in the process of modernizing its armored vehicles with Ajax (Armoured cavalry) and Boxer (mechanized infantry) vehicles. Nasmyth Group Limited won a contract to provide precision machined and fabricated components for the Boxer program. Ajax is a fully digitalized, advanced land vehicle that delivers transformational change in the UK army's future armored fleet. The Ajax vehicle system offers enhanced lethality, mobility, survivability, all-weather intelligence, surveillance, target acquisition, and recognition capabilities. In 2022, Ajax vehicle was tested for noise and vibrations, and the first round of deliveries of vehicles is planned for 2023.

Similarly, in August 2023, the Polish Government announced a partnership between the Polish Armaments Agency (AA) and the Polish Armaments Group (PGZ) to deliver 400 'Polonised' Kia Light Tactical Vehicles (KLTVs). Moreover, the Polish Armaments Group (PGZ) also gave the contract to Huta Stalowa to deliver wheeled infantry fighting vehicles (IFVs) with comprehensive logistics and training packages. Such procurement and upgrade requirements are expected to increase the revenues for the segment in the years to come.

Asia-Pacific is Projected to Dominate the Market During the Forecast Period

In terms of geography, the Asia-Pacific region accounted for the highest market share in 2023. The region is also projected to witness the highest CAGR during the forecast period, driven by the increasing demand from countries like China and India, among others. China's production capacity is advancing in almost every category of ground systems, like armored personnel carriers, assault vehicles, artillery systems and pieces, air defense artillery systems, and main and light battle tanks. China North Industries Corporation (Norinco) is focusing on increasing the production and sales of domestically manufactured armored vehicles for the past few years. These vehicles require an update to extend their lifespan. Hence, the market for retrofit and modernization is expected to witness immense growth in China. In addition, India is also increasing its armored vehicle strength due to its issues with land-border-sharing countries. A significant focus is on the modernization of its aging armored vehicle fleet. For instance, in March 2021, Mahindra Defence Systems (MDS) won a USD 127.4 million contract from the Indian Ministry of Defence (MoD) to deliver 1,300 Armoured Tactical Vehicles (LSV) for the Indian Army. Mahindra's Armoured Tactical Vehicles will be utilized as a medium of carriage for machine guns, automatic grenade launchers, and anti-tank guided missiles.

Similarly, in December 2021, Australia awarded a USD 1 billion contract to Hanwha Defense to deliver 30 self-propelled howitzers and 15 armored ammunition resupply vehicles and military vehicles for the Australian Army. Moreover, in July 2023, the Australian Army awarded a USD 6 billion contract to Hanwha Defense, where it selected Hanwha's "Redback" IFV over Rheinmetall's rival "Lynx" infantry Fighting Vehicle. Such plans are expected to increase the prospects for the market in Asia-Pacific as a whole in the years to come.

Armored Vehicle Procurement & Upgrade Industry Overview

The armored vehicle procurement and upgrade market is fragmented, with many global and local players competing with their manufacturing, MRO, and upgrade capabilities. General Dynamics Corporation, BAE Systems plc, Rheinmetall AG, Textron Inc., and Elbit Systems Ltd. are some of the prominent players in the market. The market saw an increase in the number of local players over the last decade. The aging fleet of armored vehicles in Asia-Pacific, the Middle East, and Africa gave the necessary opportunities for the local players in these regions to develop their capabilities, helping them gain significant shares in the local markets. The countries now can produce their own 3rd and 4th generation MBTs and other armored vehicles locally. In such a competitive environment, the global players are compelled to improve their policies and delivery promises to remain major players outside the United States and European Union, where they enjoy higher revenues. Also, in the coming years, global players may cut down on prices to compete with local manufacturers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Challenges and Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Vehicle Type

- 5.1.1 Armored Personnel Carrier (APC)

- 5.1.2 Infantry Fighting Vehicle (IFV)

- 5.1.3 Mine-resistant Ambush Protected (MRAP)

- 5.1.4 Main Battle Tank (MBT)

- 5.1.5 Other Vehicle Types

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 France

- 5.2.2.3 Germany

- 5.2.2.4 Russia

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Australia

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Mexico

- 5.2.4.3 Rest of Latin America

- 5.2.5 Middle East & Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 Turkey

- 5.2.5.4 South Africa

- 5.2.5.5 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 General Dynamics Corporation

- 6.2.2 Rheinmetall AG

- 6.2.3 BAE Systems plc

- 6.2.4 Textron Inc.

- 6.2.5 Elbit Systems Ltd.

- 6.2.6 RUAG International Holding Ltd.

- 6.2.7 KNDS N.V.

- 6.2.8 Oshkosh Corporation

- 6.2.9 THALES

- 6.2.10 The CMI Group, Inc.

- 6.2.11 FNSS Savunma Sistemleri A.S.

- 6.2.12 IVECO S.p.A

- 6.2.13 BMC Otomotiv Sanayi ve Ticaret A.S.

- 6.2.14 Streit Group