|

市場調査レポート

商品コード

1687101

装甲車アップグレードおよびレトロフィット:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Armored Vehicle Upgrade And Retrofit - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 装甲車アップグレードおよびレトロフィット:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

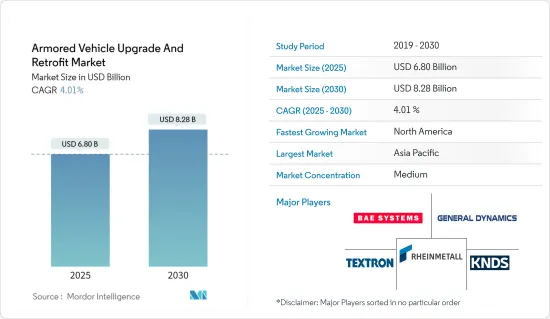

装甲車アップグレードおよびレトロフィット市場規模は2025年に68億米ドルと推定され、予測期間(2025-2030年)のCAGRは4.01%で、2030年には82億8,000万米ドルに達すると予測されます。

陸上戦闘において極めて重要な装甲車は、軍事作戦において攻撃と防御を支援するという二重の役割を担っています。これらの車両は、軍人と貨物を輸送し、さまざまな投射物をそらす武器と装甲を誇り、活発な戦闘に従事します。国家の軍事力の要であり、世界中の防衛軍で広く活用されています。

装甲車アップグレードおよびレトロフィット市場は、世界の防衛予算の拡大が主な要因となっており、進化する戦場のシナリオに合わせて頻繁にアップグレードが行われています。さらに、費用効率の高い装甲ソリューションに対する意欲も高まっています。ストックホルム国際平和研究所(SIPRI)の調査によると、2023年の世界の国防費は過去最高の2兆4,430億米ドルに達します。

世界のテロと紛争の激化により、陸上車両における最先端技術への需要が急増しています。多くの国が装甲車隊の老朽化に直面しており、効率性、殺傷力、接続性を高めるためのアップグレードプログラムにますます目が向けられています。

しかし、特に研究開発コストの高さや、装甲システムの有効性と寿命を低下させる可能性のある高爆発性対戦車(HEAT)弾頭などの兵器の急速な進歩など、課題は山積しています。こうしたハードルが市場拡大の脅威となる一方で、老朽化した装甲車を近代化するための世界の取り組みが進行していることから、今後数年間は市場を推進する構えです。

装甲車アップグレードおよびレトロフィット市場動向

歩兵戦闘車両(IFV)セグメントが予測期間中最大の市場シェアを占める見込み

歩兵戦闘車両(IFV)は、機械化歩兵戦闘車両(MICV)としても知られ、戦闘に歩兵を輸送し、直接射撃支援を提供するために設計された装甲車両です。IFVは、さまざまな弾薬から身を守るため、複合装甲や間隔積層装甲などのモジュラー式追加装甲を備えています。市場の成長は主に、世界の防衛投資の増加と防衛力強化への関心の高まりによってもたらされます。

防衛予算の拡大に伴い、各国は老朽化したIFVの火器管制、火力、全体的な機能をアップグレードしています。また、多くの国が新型車両を調達しており、車両のアップグレードや改修の需要が急増しています。例えば、2024年3月、インド国防省は、歩兵戦闘車両BMP2からBMP2Mへの693の武装アップグレードについて、Armoured Vehicles Nigam Limited(AVNL)と最終契約を締結しました。この大規模なアップグレードは、Buy(インド独自設計・開発・製造)に分類され、夜間有効化、砲手主照準器、指揮官パノラマ照準器、自動目標追尾装置付き射撃統制システム(FCS)が含まれます。

2024年3月、ネクスターはカタールの2030年以降の軍事近代化計画に沿った最新のVBCI歩兵戦闘車両をカタールに披露しました。このプレゼンテーションでは、フランス軍向けに改良されたVBCI IIの契約の可能性が示唆されました。さらに2022年12月、スウェーデンはスロバキア共和国国防省と、BAEシステムズのCV9035歩兵戦闘車152両を13億7,000万米ドルで契約しました。CV90MkIVとして販売されるCV9035は、高度な能力とデジタル技術を誇る。強化された戦場速度、優れたハンドリング、将来を見据えた電子アーキテクチャを備えたこの車両は、現代の戦場における進化する要求に応えるための十分な装備を備えています。こうした現在進行中の近代化努力は、予想されるIFVアップグレードプログラムと並んで、今後数年間におけるこのセグメントの成長を促進する態勢を整えています。

予測期間中、北米が最も高い成長率を示す見込み

装甲車アップグレードおよびレトロフィットの市場では、北米が今後数年間で優位に立つ構えです。この優位性は、同地域の旺盛な国防支出、充実した既存の装甲車保有台数、特に米国とカナダの軍事近代化投資の拡大に根ざしています。ストックホルム国際平和研究所(SIPRI)が2022年に発表した報告書では、米国の国防予算が2023年には9,160億米ドルに達するなど、米国の献身的な姿勢が強調されています。この国防予算の急増は、数多くのアップグレードや改修の構想に拍車をかけ、国の防衛力を強化しました。例えば、2024年5月、米国陸軍は次世代ブラッドレー戦闘車両を強化するため、エルビット・システムズと3,700万米ドルの契約を締結しました。ジェネラル・ダイナミクス・オードナンス・アンド・タクティカル・システムズは、エルビット社のアイアン・フィスト・アクティブ・プロテクション・システム(APS)のブラッドレーM2A4E1への統合を促進しました。

米国陸軍は、主力戦車、装甲兵員輸送車、工兵支援車、地雷防護車など、多様な装甲車両を保有しています。この多様性は、原動機、機動砲兵、軽戦術車から実用車まで、さまざまなトラックにも及んでいます。車両は、70トンを超える重量のエイブラムス主力戦車から、特殊部隊が好んで使用する1トン前後の機敏な軽量戦術全地形対応車まで、幅広いスペクトルを示しています。さらに陸軍は、ダンプトラックやピックアップトラックなど、市販されているさまざまな車両を作戦上のニーズに合わせて創造的に再利用しています。合計すると、米国陸軍の車両数はおよそ36万69台。対照的に、カナダ陸軍は大型兵站車(HLVW)車両に大きく依存しており、戦闘補給、兵員輸送、貨物輸送、予備部品輸送に優れています。こうした力学は、軍の近代化努力の高まりや国防予算の増強と相まって、市場の成長を後押ししています。

装甲車アップグレードおよびレトロフィット産業の概要

装甲車アップグレードおよびレトロフィット市場は半固定的であり、いくつかの世界およびローカルプレーヤーが大きなシェアを占めています。市場の主要企業には、General Dynamics Corporation、Rheinmetall AG、KNDS NV、Textron Inc.、BAE Systems PLCなどがあります。

市場の主要企業は研究開発投資を強化し、装甲車用の最先端ソリューションの導入に注力しています。BMC Otomotiveは2023年4月、Altay MBTの量産前モデル2両を軍に引き渡しました。これらのプロトタイプは、本格的な生産に移行する前に、1年半から2年の大規模な実地試験段階に入ることになっています。注目すべきは、BMCオトモーティブが10両のアルタイMBTのサンプルを製作したことで、それぞれがユニークなエンジンとトランスミッションのセットアップを特徴としています。2024年から2025年の間に戦車を連続生産する予定であり、このような前進は今後数年間の市場を牽引する原動力となると思われます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 車両タイプ別

- 装甲兵員輸送車(APC)

- 歩兵戦闘車(IFV)

- 耐地雷待ち伏せ防護車(MRAP)

- 主力戦車(MBT)

- その他の車両タイプ

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- エジプト

- トルコ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- General Dynamics Corporation

- Rheinmetall AG

- BAE Systems PLC

- Textron Inc.

- Elbit Systems Ltd

- Oshkosh Corporation

- KNDS NV

- FNSS Savunma Sistemleri AS

- THALES

- Ruag International Holding AG

- Patria Group

- Bharat Electronics Limited(BEL)

第7章 市場機会と今後の動向

The Armored Vehicle Upgrade And Retrofit Market size is estimated at USD 6.80 billion in 2025, and is expected to reach USD 8.28 billion by 2030, at a CAGR of 4.01% during the forecast period (2025-2030).

Armored vehicles, pivotal in land combat, play dual roles in military operations, supporting offense and defense. These vehicles transport military personnel and cargo and engage in active combat, boasting weapons and armor to deflect various projectiles. They are the cornerstone of a nation's military might and are widely utilized across defense forces worldwide.

The armored vehicle upgrade and retrofit market is predominantly driven by the escalating defense budgets globally, leading to frequent upgrades to match evolving battlefield scenarios. Moreover, there is a rising appetite for cost-efficient armor solutions. In 2023, global defense spending, as highlighted by the Stockholm International Peace Research Institute (SIPRI), hit a record high of USD 2,443 billion.

Mounting global terrorism and conflicts are driving a surge in demand for cutting-edge technologies in land vehicles. With many nations facing aging armored fleets, they are increasingly turning to upgrade programs to boost efficiency, lethality, and connectivity.

However, challenges persist, especially with the high R&D costs and the swift advancements in weaponry, such as high explosive anti-tank (HEAT) warheads, which can potentially reduce the effectiveness and lifespan of armored systems. While these hurdles pose a threat to market expansion, the ongoing global efforts to modernize aging armored vehicles are poised to propel the market in the coming years.

Armored Vehicle Upgrade And Retrofit Market Trends

The Infantry Fighting Vehicle (IFV) Segment is Expected to Hold the Largest Market Share During the Forecast Period

An infantry fighting vehicle (IFV), also known as a mechanized infantry combat vehicle (MICV), is an armored vehicle designed to transport infantry into battle and provide direct-fire support. IFVs feature modular add-on armor, including composite or spaced laminated armor, to protect against various munitions. The market's growth is primarily driven by increasing global defense investments and a growing focus on enhancing defense capabilities.

As defense budgets expand, nations are upgrading their aging IFVs' fire control, firepower, and overall functionality. Many are also procuring new vehicles, leading to a surge in demand for vehicle upgrades and retrofits. For instance, in March 2024, the Indian Ministry of Defence finalized a deal with Armoured Vehicles Nigam Limited (AVNL) for 693 armament upgrades of infantry combat vehicles BMP2 to BMP2M. This extensive upgrade, categorized as Buy (Indian-Indigenously Designed, Developed, and Manufactured), includes Night Enablement, a Gunner Main Sight, a Commander Panoramic Sight, and a Fire Control System (FCS) with an Automatic Target Tracker.

In March 2024, Nexter showcased its latest VBCI infantry fighting vehicle to Qatar, aligning with the latter's military modernization plans post-2030. The presentation hinted at potential contracts for the VBCI II, a refined version tailored for the French armed forces. Additionally, in December 2022, Sweden secured a USD 1.37 billion deal with the Slovak Republic's Ministry of Defense for 152 CV9035 infantry fighting vehicles from BAE Systems. Marketed as the CV90MkIV, the CV9035 boasts advanced capabilities and digital technology. With enhanced battlefield speeds, superior handling, and a forward-looking electronic architecture, the vehicle is well-equipped to meet the evolving demands of modern battlefields. These ongoing modernization efforts, alongside anticipated IFV upgrade programs, are poised to drive the segment's growth in the coming years.

North America is Expected to Exhibit the Highest Growth Rate During the Forecast Period

In the market for armored vehicle upgrades and retrofits, North America is poised for supremacy in the years ahead. This dominance is rooted in the region's robust defense spending, a substantial existing fleet of armored vehicles, and escalating investments in military modernization, particularly from the US and Canada. A 2022 report by the Stockholm International Peace Research Institute (SIPRI) highlighted the US's dedication, with its defense budget reaching a staggering USD 916 billion in 2023. This surge in defense funding spurred numerous upgrade and retrofit initiatives, enhancing the nation's defense capabilities. For example, in May 2024, the US Army sealed a USD 37 million deal with Elbit Systems to boost the next-gen Bradley fighting vehicle. General Dynamics Ordnance and Tactical Systems facilitated the integration of Elbit's Iron Fist Active Protection System (APS) into the Bradley M2A4E1.

The US Army boasts a diverse armored vehicle fleet, including main battle tanks, armored personnel carriers, engineering support vehicles, and mine-protected variants. This diversity extends to prime movers, mobile artillery, and a range of trucks, from light tactical to utility vehicles. The fleet showcases a broad spectrum, from the hefty 70-plus ton Abrams main battle tank to the agile Lightweight Tactical All-Terrain Vehicle favored by Special Forces, weighing around one ton. Additionally, the Army creatively repurposed various commercially available vehicles, like dump trucks and pickups, to meet its operational needs. In total, the US Army's vehicle count was around 360,069 units. In contrast, the Canadian Army heavily relies on its Heavy Logistics Vehicle Wheeled (HLVW) fleet, excelling in combat supply, troop, cargo, and spare part transportation. These dynamics, coupled with heightened military modernization efforts and bolstered defense budgets, are propelling the market's growth.

Armored Vehicle Upgrade And Retrofit Industry Overview

The armored vehicle upgrade and retrofit market is semi-consolidated, with several global and local players holding significant shares. Some of the key players in the market are General Dynamics Corporation, Rheinmetall AG, KNDS NV, Textron Inc., and BAE Systems PLC.

Key market players are intensifying their R&D investments, focusing on introducing state-of-the-art solutions for armored vehicles. BMC Otomotive, in April 2023, handed over two pre-production models of its Altay MBT to the military. These prototypes are set for an extensive 1.5-2 year field testing phase before moving into full-scale production. Noteworthy is BMC Otomotive's creation of 10 Altay MBT samples, each featuring unique engine and transmission setups. With a tentative timeline for serial tank production between 2024 and 2025, these strides are primed to drive the market in the coming years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Vehicle Type

- 5.1.1 Armored Personnel Carrier (APC)

- 5.1.2 Infantry Fighting Vehicle (IFV)

- 5.1.3 Mine-resistant Ambush Protected (MRAP)

- 5.1.4 Main Battle Tank (MBT)

- 5.1.5 Other Vehicle Types

- 5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 France

- 5.2.2.3 Germany

- 5.2.2.4 Russia

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Rest of Latin America

- 5.2.5 Middle East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 Egypt

- 5.2.5.4 Turkey

- 5.2.5.5 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 General Dynamics Corporation

- 6.2.2 Rheinmetall AG

- 6.2.3 BAE Systems PLC

- 6.2.4 Textron Inc.

- 6.2.5 Elbit Systems Ltd

- 6.2.6 Oshkosh Corporation

- 6.2.7 KNDS NV

- 6.2.8 FNSS Savunma Sistemleri AS

- 6.2.9 THALES

- 6.2.10 Ruag International Holding AG

- 6.2.11 Patria Group

- 6.2.12 Bharat Electronics Limited (BEL)