航空機フライトレコーダー:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Aircraft Flight Recorder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1689687

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

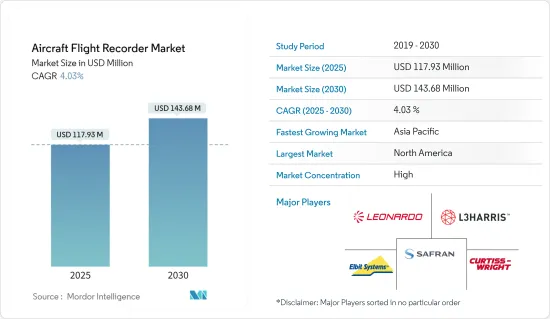

航空機フライトレコーダーの市場規模は2025年に1億1,793万米ドルと推定され、予測期間(2025-2030年)のCAGRは4.03%で、2030年には1億4,368万米ドルに達すると予測されています。

航空機フライトレコーダー市場は、主に新型航空機の需要に左右されます。航空産業は成長しており、新しい航空機の調達は地域間で大規模に行われています。これにより、航空機フライトレコーダーを含む航空機サプライチェーン全体に対する需要が発生する可能性が高いです。

EASAやICAOなどの規制機関による、航空機への新しいフライトレコーダー(水中探知装置や航空機の位置特定装置)の搭載を改正する規制により、複数の航空会社が新規制に準拠することになりました。このため、これらの規制に対応した新製品への主要企業の投資が進み、航空機のOEMや運航会社から新型レコーダーの需要が高まっています。

半導体の好不況サイクルの影響は、半導体の世界サプライチェーン全体に見られます。このような周期的な調整は、供給を減らし、調達に関連するリスクを高めることによって、高信頼性サプライチェーンを不安定にする可能性があります。航空機の飛行を維持するフライトコンピュータは、航空部門にとって極めて重要な半導体によって駆動されています。世界な航空宇宙サプライチェーンは、歴史的にこのようなサイクルに耐えてきましたが、予期的かつ予防的な対策が不可欠であることに変わりはありません。航空機フライトレコーダーにおける半導体のこうした本質的な側面を考慮すると、半導体不足は市場にとって短期的な抑制要因になると推測されます。

航空機フライトレコーダーの市場動向

予測期間中、民間・商業航空セグメントが最大市場を占めると予測

フライトデータレコーダー(FDR)は、航空機の特定の性能パラメータを記録します。FDRは、航空機の各種センサーからデータを収集し、事故に耐えられるように設計された媒体に記録します。航空機納入数の増加により、安全性を高めるための航空機フライトレコーダの需要が生じています。航空機納入数の増加、航空旅客数の増加、民間航空分野における新技術の導入は、最近の市場成長を後押しする重要な要因です。例えば、IATAによると、2023年の世界の旅客キロ収入は2022年比で36.9%増加し、世界の航空輸送量はパンデミック前の94.1%に達しました。

さらに、最近の世界の航空機の受注・納入動向は、民間航空向けの先進的な航空機フライトレコーダー・デバイスの開発を劇的に後押ししています。例えば、2023年にはボーイングが735機、エアバスが528機の民間ジェット機を納入しており、2022年には676機、480機が納入されました。2023年には、エアバスがボーイングより多くの航空機を納入し、5年連続で納入機数の栄冠に輝いた。

また、エアバスが発表した民間航空宇宙市場の20年予測によると、エアバスは旅客と貨物輸送のニーズを満たすため、数値上では40,850機の新規航空機の需要を見込んでいます。これらの航空機のうち、約32,630機が単通路型に分類され、8,220機がワイドボディ型に分類されます。貨物機の需要も2,510機に達する見込みで、そのうち約920機が新たに生産されます。このように、旅客輸送量の増加と民間航空分野における開発の増加は、市場の明るい見通しにつながり、航空機フライトレコーダーシステムは予測期間中、民間航空分野で大きな成長を遂げると思われます。

アジア太平洋地域が予測期間中に最速の成長を示す

航空分野への支出の増加と、特に中国とインドからの新しい航空機への需要が、この地域の市場成長を後押しします。2024年1月、IATAは、アジア太平洋地域の航空会社が2023年通年の国際線トラフィックで2022年比126.1%増を記録し、地域の中で最も堅調な前年比成長率を維持したと発表しました。

また、中国では民間機と軍用機に関して著しい成長が見られました。例えば、ボーイングは2023年11月、今後20年間で世界の航空機需要全体の20%を中国が占めると発表しました。これは、中国が737マックスのような単通路機を約6,500機、ボーイングの787ドリームライナーのような大型の双通路機を1,500機以上必要とすることを意味します。

中国、インド、日本など、この地域の重要な国々が複数の航空機を発注しました。例えば、2023年7月、インディゴは2030年から2035年の間に500機のA320neoを納入する大規模な契約をエアバスに発注しました。同様に、2023年6月、エア・インディアはエアバスに250機、ボーイングに220機を納入する契約を結びました。さらに、2023年9月、中国東方航空は、100億米ドルでC919型機100機を追加納入する契約をコマックに発注しました。これらの航空機は、2024年から2031年にかけて順次納入される予定です。

中国の広西チワン族自治区で起きた中国東方航空のボーイング737型機(132人搭乗)の墜落事故を受け、中国航空業界では航空機フライトレコーダーの生産が大幅に増加しています。日本政府は、日本における大規模な墜落事故を受けて、航空安全への取り組みを強化しています。より耐久性に優れ、極端な温度変化にも耐えられる先進的な航空機フライトレコーダーの設置にますます重点を置くようになったことが、日本の航空当局の主な焦点となっています。

インド、中国、日本による防衛費の増大と次世代戦闘機の調達が市場の成長を後押しします。2023年には、中国とインドがそれぞれ2,960億米ドルと836億米ドルの国防予算で、世界第2位と第4位の国防支出国となりました。アジア太平洋のさまざまな国々による軍用機の調達の増加は、先進的な航空機フライトレコーダーシステムの開発の成長につながります。

例えば、2023年12月、インド国防省は130億米ドルの国産航空機調達を承認しました。この調達には、インド空軍向けのLCA Tejas Mark 1A戦闘機97機と、IAFおよびインド陸軍向けのPrachand攻撃ヘリコプター156機が含まれます。このように、様々な国による民間および軍事部門向けの新しい航空機の調達の増加と、アジア太平洋の様々な国による航空産業への支出の増加は、予測期間中に市場が前向きな見通しと成長を示すことにつながります。

航空機フライトレコーダー産業の概要

航空機フライトレコーダー市場は統合されており、少数のプレーヤーが大きなシェアを占めています。著名な市場プレーヤーは、L3Harris Technologies Inc.、Curtiss-Wright Corporation、Elbit Systems Limited、Safran SA、Leonardo SpAなどです。

市場の主なプレーヤーは、先進的な航空機フライトレコーダーシステムの開発に注力しています。さらに、さまざまなメーカーが現在、極端な状況に耐える航空機フライトレコーダーシステムを構築するために高度な材料を使用しています。先進的な航空機フライトレコーダーを開発するための研究開発と新素材の導入に対する支出の開拓は、予測期間中、市場により良い機会を生み出すと思われます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ

- フライトデータレコーダー(FDR)

- コックピットボイスレコーダー(CVR)

- コックピット・ボイス・データ・レコーダー(CVDR)

- エンドユーザー

- 民間および商用航空

- 軍用航空

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- メキシコ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Aversan Inc.

- L3Harris Technologies, Inc.

- The General Electric Company

- Curtiss-Wright Corporation

- Elbit Systems Ltd.

- Safran SA

- Niron M.S. Systems & Projects Ltd.

- Leonardo S.p.A

- Flight Data Systems

- Honeywell International Inc.

第7章 市場機会と今後の動向

目次

The Aircraft Flight Recorder Market size is estimated at USD 117.93 million in 2025, and is expected to reach USD 143.68 million by 2030, at a CAGR of 4.03% during the forecast period (2025-2030).

The aircraft flight recorder market primarily depends on the demand for new aircraft. The aviation industry is growing, and new aircraft procurement is being done on a large scale across regions. This will likely generate demand for the entire aircraft supply chain, including the aircraft flight recorder.

Regulations amending the installation of new flight recorders (underwater locating devices and aircraft localization) onboard aircraft by regulatory bodies like EASA and ICAO have resulted in several airlines complying with the new regulations. This has led to investments by companies in new products aligning with these regulations and the demand for new recorders from aircraft OEMs and operators.

The effects of semiconductor boom and bust cycles are seen throughout semiconductors' global supply chain. These cyclical adjustments can destabilize the high-reliability supply chain by reducing supply and raising the risks associated with sourcing. The flight computers that keep airplanes in the air are powered by semiconductors, which are crucial to the aviation sector. Although the global aerospace supply chain has historically withstood these cycles, anticipatory and preventative measures remain vital. Considering these essential aspects of semiconductors in aircraft flight recorders, it is presumed that the semiconductor shortage will be a short-term restraint for the market.

Aircraft Flight Recorder Market Trends

The Civil and Commercial Aviation Segment is Projected to Occupy the Largest Market During the Forecast Period

Flight data recorders (FDRs) record specific aircraft performance parameters. The FDRs collect and record data from various aircraft sensors onto a medium designed to survive an accident. The increasing number of aircraft deliveries creates demand for aircraft flight recorders to enhance safety. A growing number of aircraft deliveries, a rise in air traffic passengers, and the introduction of new technologies in the commercial aviation sector are critical factors that have fueled the market's growth in recent times. For instance, according to IATA, in 2023, the global revenue of passenger kilometers rose by 36.9% compared to 2022, and the global air traffic was at 94.1% of the pre-pandemic levels.

Moreover, the number of aircraft orders and deliveries worldwide in recent years has dramatically boosted the development of advanced aircraft flight recorder devices for commercial aviation. For instance, in 2023, Boeing and Airbus delivered 735 and 528 commercial jets, compared to 676 and 480 deliveries in 2022. In 2023, Airbus won the deliveries crown for the fifth year in a row by delivering more aircraft than Boeing.

In addition, according to the 20-year forecast published by Airbus for the commercial aerospace market, in numerical terms, Airbus anticipates a demand for 40,850 new aircraft to meet the needs of passengers and freight transportation. Among these aircraft, around 32,630 will be categorized as single aisle, while 8,220 will fall under the widebody classification. The demand for freighters is also expected to reach 2,510 aircraft, with approximately 920 of the aircraft being newly produced. Thus, growth in air passenger traffic coupled with increasing developments in the commercial aviation space will lead to a positive outlook for the market, and aircraft flight recorder systems will witness significant growth in the commercial aviation segment during the forecast period.

Asia-Pacific to Exhibit Fastest Growth During the Forecast Period

Growing expenditure on the aviation sector and demand for new aircraft, especially from China and India, will boost the market growth across the region. In January 2024, IATA announced that the airlines in the Asia-Pacific recorded a 126.1% rise in full-year international traffic in 2023 compared to 2022 and maintained the most robust Y-o-Y growth rate among the regions.

In addition, there has been significant growth regarding commercial and military aircraft in China. For instance, in November 2023, Boeing announced that China will make up 20% of the total airplane demand worldwide over the next twenty years. This implies that China will require approximately 6,500 single-aisle planes like the 737 Max and over 1,500 larger, twin-aisle planes like Boeing's 787 Dreamliner.

Significant countries in the region, like China, India, and Japan, ordered several aircraft. For instance, in July 2023, Indigo awarded a massive contract to Airbus to deliver 500 A320neo aircraft between 2030 and 2035. Similarly, in June 2023, Air India awarded a contract to Airbus to deliver 250 aircraft and Boeing to 220 aircraft. In addition, in September 2023, China Eastern Airlines awarded a contract to Comac to provide an additional 100 C 919 aircraft for USD 10 billion. The planes will be delivered in batches from 2024 to 2031.

There has been a significant increase in the production of aircraft flight recorder devices in the Chinese aviation industry following the air crash incident in China's Guangxi Zhuang Autonomous Region in which a China Eastern Boeing 737 with 132 people onboard, crashed due to pilot error as pointed out by the data recovered from the aircraft flight recorders. The Japanese government has increased its focus on aviation safety following major crashes in Japan. Increasing focus on installing advanced aircraft flight recorders that are more durable and able to withstand extreme temperature fluctuations is the main focus of aviation authorities in Japan.

Growing defense expenditures and procurement of next-generation fighter jets from India, China, and Japan propel the market's growth. In 2023, China and India were the world's second and fourth-largest defense spenders, with a defense budget of USD 296 billion and USD 83.6 billion, respectively. The increasing procurement of military aircraft by various countries in Asia-Pacific will lead to growth in the development of advanced aircraft flight recorder systems.

For instance, in December 2023, the Indian MoD approved an indigenous aircraft procurement for USD 13 billion. The procurement includes 97 LCA Tejas Mark 1A fighter jets for the Indian Air Force and 156 Prachand attack helicopters for the IAF and the Indian Army. Thus, an increase in the procurement of new aircraft for the commercial and military sectors by various countries and increased spending on the aviation industry by various countries in Asia-Pacific will lead the market to witness a positive outlook and growth during the forecast period.

Aircraft Flight Recorder Industry Overview

The aircraft flight recorder market is consolidated, with few players holding significant shares. Some prominent market players are L3Harris Technologies Inc., Curtiss-Wright Corporation, Elbit Systems Limited, Safran SA, and Leonardo SpA.

The key players in the market are focusing on developing advanced aircraft flight recorder systems. Moreover, various manufacturers are now using advanced materials to build aircraft flight record systems that survive extreme situations. Growing expenditures on research and development and introducing new materials to develop advanced aircraft flight recorders will create better opportunities in the market during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Flight Data Recorder (FDR)

- 5.1.2 Cockpit Voice Recorder (CVR)

- 5.1.3 Cockpit Voice and Data Recorder (CVDR)

- 5.2 End User

- 5.2.1 Civil and Commercial Aviation

- 5.2.2 Military Aviation

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Mexico

- 5.3.4.2 Brazil

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Egypt

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Aversan Inc.

- 6.2.2 L3Harris Technologies, Inc.

- 6.2.3 The General Electric Company

- 6.2.4 Curtiss-Wright Corporation

- 6.2.5 Elbit Systems Ltd.

- 6.2.6 Safran SA

- 6.2.7 Niron M.S. Systems & Projects Ltd.

- 6.2.8 Leonardo S.p.A

- 6.2.9 Flight Data Systems

- 6.2.10 Honeywell International Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日