侵入テスト:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Penetration Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 167 Pages

- 納期

- 2~3営業日

- 商品コード

- 2044188

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

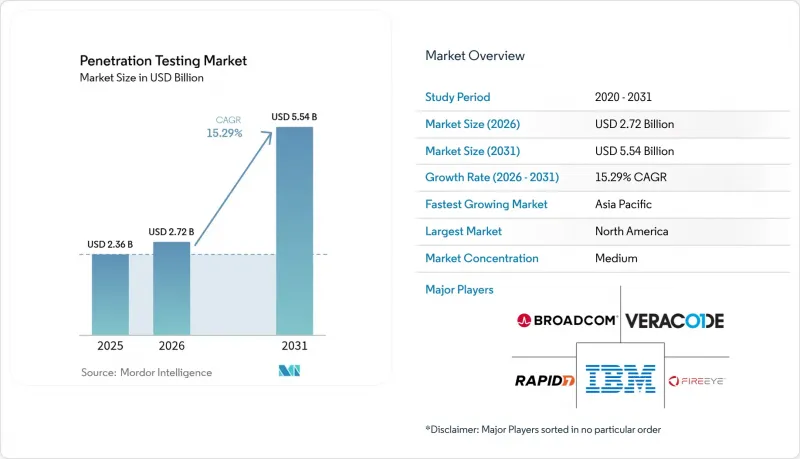

侵入テスト市場の規模は、2025年の23億6,000万米ドル、2026年の27億2,000万米ドルから、2031年までに55億4,000万米ドルへと拡大すると予測されており、2026年から2031年までの年間平均成長率(CAGR)は15.29%となる見込みです。

クラウドワークロードの急速な普及、生成AIを活用した攻撃の急増、および規制遵守期限の短縮により、侵入テストは単発的な監査から常時稼働型の管理へと移行しつつあります。企業は現在、攻撃者が数時間以内に悪用し得る公開された脆弱性に対する不可欠な保険として、予防的な検証を位置づけています。HIPAAやPCI DSSバージョン4.0に基づく年次テストの義務化に加え、欧州連合(EU)の「デジタルオペレーショナルレジリエンス法(DORA)」やNIS2により、内部の意思決定サイクルが短縮され、複数年契約の金額も増加しています。ベンダー各社は、テスト期間を数週間から数日に短縮する自律型レッドチームエージェントでこれに対応しており、CI/CDパイプラインとの統合により、開発者はコミットごとにテストを実行できるようになっています。したがって、競合環境は、継続的なカバレッジ、規制への対応状況の可視化、および詳細なレポート機能を兼ね備えたプラットフォームを有利にしています。

世界の侵入テスト市場の動向とインサイト

全セクターにおけるサイバーセキュリティリスクの高まり

現在、脆弱性が公開されてから数時間以内に公開型エクスプロイトキットが出現しており、防御側の対応時間が短縮され、侵入テストの頻度を高める必要に迫られています。Dragos社の調査によると、2026年には26の脅威グループがオペレーショナルテクノロジー(OT)を積極的に探査しており、産業環境がもはや隠蔽性や安全性を享受できていないことが示されています。ポーランドの電力網に対する組織的な攻撃を受け、CISA(米国サイバーセキュリティ・インフラセキュリティ庁)は重要インフラ事業者に対し四半期ごとのテストを要請し、年次テストサイクルに対する規制当局の忍耐が尽きつつあることを示唆しました。Penteraが500人のセキュリティ責任者を対象に行った調査によると、67%が前年に少なくとも1回の侵害被害を受けており、テスト予算の中央値は18万7,000米ドルに引き上げられました。これは、経営幹部が現在、予防的な検証を監査のための贅沢品ではなく、保険として捉えていることを裏付けています。これらのデータは総合的に、脅威の速度が加速することで、継続的な侵入テストへの需要が直接的に拡大していることを示しています。

セキュリティ評価およびコンプライアンス監査への需要の高まり

多層的な業界フレームワークにより、侵入テストの義務条項が積み重なり、組織は複数の監査を1つのプログラムに統合することを余儀なくされています。2025年3月に発効するPCI DSSバージョン4.0では、すべての加盟店に対して年次テストに加え、以前は任意だったセグメンテーションおよびワイヤレス評価が義務付けられています。FDAの市販前ガイダンスでは、医療機器メーカーに対し、すべての申請にテスト結果を含めること、および市販後の証拠を維持することを義務付けており、その対象範囲は病院からサプライヤーにまで拡大しています。FedRAMP 3.0では、連邦政府のクラウドプロバイダーに対し四半期ごとのスキャンと年次テストが義務付けられており、草案段階の4.0では、影響度の高いシステムについてその頻度を倍増させる提案がなされています。ニューヨーク州の改正された23 NYCRR 500規則では、取締役会が30日以内に侵入テストの結果を審査することが求められており、テストは単なる技術的な演習からガバナンスの成果物へと格上げされています。こうした重複する監査により、企業は単一の契約で複数の規則集に対応できるマネージドサービスプロバイダーを求めるようになっています。

熟練したテスターの不足と高コスト

認定ペネトレーションテスターに対する世界の需要は供給を大幅に上回っており、これにより契約料金が高騰し、プロジェクトの待ち時間が長くなっています。ISC2の調査によると、95%の組織がサイバーセキュリティ人材の不足を報告しており、攻撃的テスト担当者は採用が最も困難な3つの職種の一つに挙げられています。英国では2024年時点で依然として1万1,200人のサイバーセキュリティ人材が不足しており、特に攻撃的役割の採用には最も長い時間がかかっています。高度なOSCP資格の合格率は依然として50%を下回っており、学習曲線が急峻であり、人材パイプラインの成長が鈍いことを示しています。そのため、企業は日常業務の自動化に目を向けていますが、スコープ設定、ソーシャルエンジニアリング、および攻撃後の分析には依然として人間の専門知識が必要です。この根強い人材不足がサービス提供能力を制限し、需要が旺盛であるにもかかわらず市場の成長を抑制しています。

セグメント分析

2025年の侵入テスト市場において、ネットワーク評価は38.23%のシェアを占め、境界防御および横方向の移動防御が引き続き優先されていることを示しています。しかし、マルチクラウドの導入に後押しされたクラウド侵入テストは、2031年までCAGR16.63%で拡大すると予測されており、最も成長の速い分野となる見込みです。この変化は、従来のネットワークの範囲外となるコンテナオーケストレーション、サーバーレス機能、およびAPI中心のアーキテクチャを反映しています。Bishop Foxは2026年にCloudFoxツールキットをGoogle Cloud Platformに拡張し、クラウドネイティブのテスト手法が成熟期に入ったことを示しました。攻撃者がチャネルをまたいでAPIやクレデンシャルスタッフィングの手法を頻繁に再利用するため、モバイルおよびWebアプリケーションのテストは融合しつつあります。ソーシャルエンジニアリング演習では、生成AIによって可能になった動向として、ディープフェイク音声や動画による攻撃がシミュレートされるようになりました。ワイヤレステストの範囲は拡大し、工場や物流拠点におけるWi-Fi 6Eおよび5Gプライベートネットワークも対象となっています。産業用資産の所有者がダウンタイムを回避するためにサンドボックス環境で生産環境を再現するようになるにつれ、IoTおよびオペレーショナルテクノロジー(OT)の評価も増加しています。

ネットワーク、クラウド、アプリケーションの範囲を統合したハイブリッド型侵入テストの市場規模は拡大しています。これは、買い手が複数のフレームワークにまたがる単一の契約を好むためです。コンプライアンスサイクルが厳格化する中、統合ダッシュボードや自動再テストを提供するベンダーが契約を獲得しています。継続的な検証への期待は急速に高まっており、Bishop FoxのCosmos AIは評価時間を40%短縮すると主張し、HackerOneのエージェンティックサービスは数日ではなく数時間以内に結果を報告します。こうした効率化により、セキュリティチームは予算を増やすことなく、より頻繁なテストをスケジュールできるようになります。脅威アクターが公開された脆弱性を数時間で悪用する中、企業は単に脆弱性の存在を確認するだけでなく、実際に悪用可能かどうかを検証する手法へと移行しています。その結果、需要は一時的なネットワークスキャンから、CI/CDパイプラインに直接統合される常時稼働型のクラウドおよびアプリケーションプローブへと移行しています。

2025年時点では、規制対象となる多くの業界が依然としてオンプレミスでの管理を好むため、侵入テスト市場の59.21%をオンプレミス展開が占めていました。しかし、DevSecOpsサイクルに合致した弾力的なスケーリングと迅速な機能更新に後押しされ、クラウド提供プラットフォームは2031年までにCAGR15.61%で成長する見込みです。Aikido Infiniteは、開発者がサーバーをプロビジョニングすることなく、コミットごとに侵入テストを実行できるようにし、SaaS提供の運用上の容易さを示しています。PCI DSS 4.0では、クラウドベースのテストがカード会員データ規則を満たすことが明確化され、長らく残っていた障壁が取り除かれました。現在、ハイブリッド環境がエンタープライズアーキテクチャの主流となっているため、クラウドワークロードとオンプレミス資産の両方に対する可視性が不可欠となっています。

オンプレミス向け侵入テスト市場は、主権に関する規則により外部接続が遮断されているエアギャップ化された政府や防衛ネットワークにおいて、依然として堅調です。そうした環境であっても、ベンダーは、接続が可能になった際に匿名化された調査結果を同期させる仮想アプライアンスを提供しています。より広範な市場においては、サブスクリプション価格体系により、支出が資本支出から運営予算へと移行し、承認プロセスが簡素化されています。マネージドサービスプロバイダーは、取締役会レベルの報告要件を満たす口頭報告を伴うクラウドテストダッシュボードを、ますますバンドル提供するようになっています。また、テスト結果をREST API経由でチケット管理システムに直接取り込むことで、パッチの検証が迅速化される点も、購入者から評価されています。継続的デプロイメントが一般的になるにつれ、組織はクラウドによる提供を単なる選択肢ではなく、法令で禁止されていない限りデフォルトの選択肢と見なすようになっています。

地域別分析

北米は2025年に侵入テスト市場の38.27%を占めました。これは、HIPAA、PCI DSS 4.0、FedRAMPといった成熟した規制枠組みに支えられており、これらは年次または半期ごとのテストサイクルを正式に定めています。米国の金融機関は、脅威主導型のテストをオペレーショナル・レジリエンス・プログラムに組み込んでおり、一方、カナダの医療プライバシーに関する法令は、病院に対し継続的な検証の導入を促しています。メキシコの急成長するフィンテックエコシステムも、侵入テストを国境を越えた決済ライセンスに組み込んでおり、地域的な需要を拡大させています。ベンチャー資金はシリコンバレーとボストンに集中しており、これにより現地のプラットフォームベンダーは、国内の顧客向けにテストサイクルを短縮するAIエージェントの開発を繰り返し行っています。その結果、北米は新しいツールやサービスモデルの基準となる市場であり続けています。

アジア太平洋地域では、2031年までにCAGR16.26%で侵入テスト市場が拡大すると予測されており、これは地域別で最も高い成長軌道です。インドではサイバーセキュリティ人材が30%から50%不足しているため、企業は自動化プラットフォームの導入を促進しています。一方、中国ではデータローカライゼーション規制により、個人情報を扱うすべてのシステムについて国内でのテストが義務付けられています。日本の改正個人情報保護法や韓国の重要インフラに関する規制により、年次テストが企業統治にさらに組み込まれています。インドネシアやフィリピンにおけるデジタル決済の急速な普及は、地域のゲートウェイに接続する小規模な加盟店に対する検証の必要性を浮き彫りにしています。これらの要因が相まって需要が急増しており、世界のベンダーにとっては、地域内のクラウドPoP(ポイント・オブ・プレゼンス)や現地語によるレポート提供を正当化する一因となっています。

欧州では、「デジタル・オペレーショナル・レジリエンス法(Digital Operational Resilience Act)」、「NIS2」、および今後施行される「サイバーレジリエンス法(Cyber Resilience Act)」によってコンプライアンスの最低基準が確立されており、これらにより侵入テストはベストプラクティスから法的義務へと格上げされています。ドイツの連邦情報セキュリティ局(BSI)は2025年に重要インフラ向けのセクター別プレイブックを公表し、フランスはSecNumCloudフレームワークを拡大して、サービスプロバイダーに対する義務的なテストを含めるようにしました。英国の国家サイバーセキュリティセンター(NCSC)は、ブレグジット後の基準を欧州大陸の規範と整合させるため、機密データを扱うすべての企業に対して年次テストを推奨しています。南米、中東・アフリカは、ブラジルのデータ保護法や湾岸諸国の国家サイバープログラムが、ライセンシング制度に攻撃的テストを組み込んでいることから、有力な市場として台頭しています。したがって、全体的な地理的拡大のペースは、各管轄区域において法令が「指針」から「施行」へと移行する速さによって左右されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 全セクターにわたり高まるサイバーセキュリティリスク

- セキュリティ評価およびコンプライアンス監査に対する需要の高まり

- 政府の義務付けおよび業界固有の規制

- DevSecOpsパイプラインには、継続的な侵入テストの統合が必要です

- AIを活用した自律型レッドチーミングにより、継続的な検証が可能になります

- ソフトウェア部品表(SBOM)の義務化により、サプライチェーンの侵入テストの範囲が拡大

- 市場抑制要因

- 中小企業における認識不足

- 熟練テスターの不足と高コスト

- 重要なOT環境における実環境での悪用に対する倫理的制約

- 複数管轄区域にまたがるクラウド環境における法的責任の不明確さ

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- マクロ経済要因が市場に与える影響

第5章 市場規模と成長予測

- テストタイプ別

- ネットワーク侵入テスト

- Webアプリケーション侵入テスト

- モバイルアプリケーションの侵入テスト

- ソーシャルエンジニアリング侵入テスト

- ワイヤレスネットワーク侵入テスト

- クラウド侵入テスト

- その他のテストタイプ

- 展開モデル別

- オンプレミス

- クラウドベース

- 組織規模別

- 大企業

- 中小企業

- サービス提供形態別

- 社内テストチーム

- サードパーティ管理サービス

- エンドユーザー産業別

- 政府・防衛

- 銀行、金融サービス、保険

- IT・通信

- ヘルスケア・ライフサイエンス

- 小売・Eコマース

- 製造業

- エネルギー・公益事業

- その他のエンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動きと資金調達

- 市場シェア分析

- 企業プロファイル

- IBM Corporation

- Rapid7 Inc.

- Synopsys Inc.

- Checkmarx Ltd.

- Acunetix Ltd.

- Broadcom Inc.

- FireEye Inc.

- Veracode Inc.

- Qualys Inc.

- Tenable Holdings Inc.

- Palo Alto Networks Inc.

- Offensive Security LLC

- Core Security Technologies Inc.

- Pentera Security Ltd.

- HackerOne Inc.

- Trustwave Holdings Inc.

- IOActive Inc.

- NCC Group plc

- Cofense Inc.

- Bishop Fox Inc.

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 167 Pages

- 納期

- 2~3営業日