|

市場調査レポート

商品コード

1444675

3Dプリンティング材料:市場シェア分析、業界動向と統計、成長予測(2024~2029年)3D Printing Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 3Dプリンティング材料:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

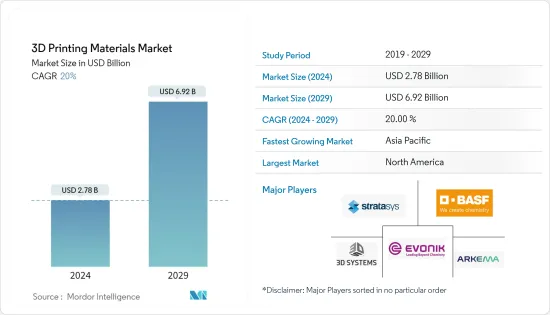

3Dプリンティング材料市場規模は2024年に27億8,000万米ドルと推定され、2029年までに69億2,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に20%のCAGRで成長します。

COVID-19のパンデミックの発生により、サプライチェーンの混乱により3Dプリンティング材料市場は打撃を受け、その結果、いくつかのプロジェクトに遅れが生じました。さらに、さまざまな国での資金の流れの混乱と厳格なロックダウンにより、生産ライン労働者の欠勤が増加し、市場に悪影響を及ぼしました。しかし、自動車業界からの需要の増加により、2021年に市場は回復しました。

主なハイライト

- 市場の成長を牽引する主な要因は、製造アプリケーションの需要の急増、3Dプリンティングに関連するマスカスタマイゼーション、および自動車アプリケーションの需要の急増です。

- 一方で、設備や材料のコストが高く、材料の入手可能性が限られていることが、市場の成長を妨げる可能性があります。

- グラフェンのような新素材の導入は新たな用途を開拓し、家庭用印刷における3Dプリンティング技術の採用は3Dプリンティング材料市場に新たな機会を生み出すことが期待されています。

3Dプリンティング材料市場動向

自動車産業でのアプリケーションの増加

- 3Dプリンティング材料は、自動車業界でテスト用の縮尺モデルを製造するために広く使用されています。これらは、ベローズ、フロントバンパー、空調ダクト、サスペンションウィッシュボーン、ダッシュボードインターフェイス、オルタネーター取り付けブラケット、バッテリーカバーなどのコンポーネントにも使用されます。自動車OEMメーカーは、ラピッドプロトタイピングに3Dプリンティング材料を使用しています。

- 3Dプリンティングプロセスには、低コスト、製造時間の短縮、材料の無駄の削減などの利点があるため、自動車メーカーはこのプロセスに移行しつつあります。アウディ、ロールスロイス、ポルシェ、ハッロッドなどの世界最大手の自動車メーカーは、スペアパーツや金属プロトタイプの製造にこれらの材料を使用しています。

- 中国の自動車製造産業は世界最大です。中国汽車工業協会(CAAM)によると、2023年3月の自動車生産台数は258万4,000台、販売台数は245万1,000台で、前月比ではそれぞれ27.2%、24%増加し、前年同月比では24%増加しました。前年同期比ではそれぞれ15.3%、9.7%増加しました。

アジア太平洋は最速の速度で成長すると予想される

- アジア太平洋は世界で最も急速に成長している経済国の一つであり、その中には中国も含まれており、人口、生活水準、一人当たり所得の上昇により、ほぼすべてのエンドユーザー産業が成長しています。

- この地域は、自動車分野で注目すべき生産を行う複数の国で構成されています。さらに、電気自動車の出現により、3Dプリンティング材料市場に大きな成長機会がさらに提供されると予想されます。

- 2022年には、インド、インドネシア、マレーシア、ベトナムなどのいくつかの国で自動車生産が大幅に成長すると予想されています。例えば、国際自動車工業機構(OICA)によると、2022年のインドとインドネシアの自動車総生産台数はそれぞれ545万6,857台と147万146台で、前年比24%、31%の成長を示しました。年。

- 2022年9月20日、財務省(MOF)、工業情報化省(MIIT)、国家税務局(STA)は共同で、2023年1月から12月までの新エネルギー車(NEV)の購入を発表しました。 2023年には自動車取得税が免除されます。これにより、中国における新型電気自動車の需要と販売が支えられています。

- さらに、3D印刷における層ごとの堆積プロセスにより、センサー、アンテナ、その他の機能電子機器をプラスチック部品、金属表面、ガラスパネル、セラミック材料上に直接印刷できます。

- 中国情報通信技術院の報告書によると、2022年の最初の2カ月間、エレクトロニクス製造業界は着実な拡大を維持しました。 2022年1月から2月までの大手電機メーカーの付加価値は年率12.7%増加。ただし、同期間の産業全体の成長率は7.5%でした。

- 中国は、新技術や建設用の革新的な材料の使用に関して最も急速に成長している市場の一つです。中国が世界の建設の中心地として支配的な役割を果たしていることから、家庭用印刷分野における3Dプリンティングの開発が加速することで、住宅建物から記念碑に至るまで幅広い用途で、同国の伝統的な建設業界に革命を起こす可能性が高いです。この国は住宅やその他の大規模構造物の3Dプリントに成功し、他のすべての国が建設における3Dプリンティングの可能性を検討するようになりました。

- 建設分野での3Dプリンティングには、建築開発者からの信頼の欠如や、この技術の使用に関する適切な規制がないなど、いくつかの制限があります。しかし、新しいテクノロジーとその利点に対する認識が高まるにつれ、組織や個人はコストを節約できる代替手段を検討するようになっています。これにより、国内の3Dプリンティング材料市場の需要が高まっています。

- 上記のすべての要因により、アジア太平洋における3Dプリンティング材料の需要が調査対象の市場を牽引すると予想されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 製造アプリケーションでの使用の増加

- 3Dプリントに関連したマスカスタマイゼーション

- 自動車用途における需要の急増

- 抑制要因

- 高い設備費と材料費

- 利用できる材料の種類が限られている

- 業界のバリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替製品やサービスの脅威

- 競合の程度

第5章 市場セグメンテーション

- 材料の種類

- プラスチック

- アクリロニトリル・ブタジエン・スチレン(ABS)

- ポリ乳酸(PLA)

- ナイロン

- ポリアミド

- ポリカーボネート

- その他のプラスチック

- セラミックス

- 金属

- 他の材質タイプ

- プラスチック

- 形状

- 粉

- フィラメント

- 液体

- エンドユーザー産業

- 自動車

- 医学

- 航空宇宙と防衛

- 家電

- その他のエンドユーザー産業

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- シンガポール

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- ロシア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東とアフリカ

- サウジアラビア

- 南アフリカ

- その他中東およびアフリカ

- アジア太平洋

第6章 競合情勢

- 合併と買収、合弁事業、コラボレーション、および契約

- 市場シェア(%)**/ランキング分析

- 有力企業が採用した戦略

- 企業プロファイル

- 3D Systems, Inc.

- Arkema

- BASF SE

- CRP TECHNOLOGY Srl

- CRS Holdings, LLC

- ENVISIONTEC US LLC

- EOS

- Evonik Industries AG

- General Electric

- Henkel AG &Co. KGaA

- Hoganas AB

- Materialise

- Sandvik AB

- Solvay

- Stratasys

第7章 市場機会と将来の動向

- グラフェンなどの新素材のイントロダクションより新たな用途が開拓される

- 家庭用印刷における3Dプリンティング技術の採用

The 3D Printing Materials Market size is estimated at USD 2.78 billion in 2024, and is expected to reach USD 6.92 billion by 2029, growing at a CAGR of 20% during the forecast period (2024-2029).

With the outbreak of the COVID-19 pandemic, the 3D printing materials market suffered due to the disruption in the supply chain, resulting in delays in several projects. Moreover, disrupted financial flows and strict lockdowns in various countries, resulting in growing absenteeism among production line workers, affected the market adversely. However, the market rebounded in 2021 due to increased demand from the automotive industry.

Key Highlights

- The major factors driving the market growth are the surge in demand for manufacturing applications, mass customization associated with 3D printing, and the surge in demand for automotive applications.

- On the flip side, high equipment and material costs and limited materials availability will likely hinder the market's growth.

- Introducing new materials, like graphene, opens up new applications, and adopting 3D printing technology in home printing is expected to create new opportunities for the 3D printing materials market.

3D Printing Materials Market Trends

Increasing Applications in the Automotive Industry

- 3D printing materials are extensively used in the automotive industry to manufacture scaled models for testing. They are also used for components, such as bellows, front bumper, air conditioning ducting, suspension wishbone, dashboard interface, alternator mounting bracket, battery cover, etc. Automotive OEM manufacturers are using 3D printing materials for rapid prototyping.

- Due to the advantages of the 3D printing process, such as low cost, less manufacturing time, reduced material wastage, etc., automotive manufacturers are moving toward this process. Some of the largest automotive manufacturers in the world, such as AUDI, Rolls Royce, Porsche, Hackrod, and many others, are using these materials for manufacturing spare parts and metal prototypes.

- The Chinese automotive manufacturing industry is the largest in the world. According to the China Association of Automobile Manufacturers (CAAM), In March 2023, the production and sales of automobiles accounted for 2.584 million and 2.451 million units, respectively, with an increase of 27.2% and 24% respectively on the month every month and an increase of 15.3% and 9.7% respectively on a year-on-year basis.

- According to the China Association of Automobile Manufacturers (CAAM), from January to March of 2023, passenger cars production and sales accounted for 5.262 million and 5.138 million units, respectively, with an increase of 4.3% and 7.3%, respectively, on a year-on-year basis. Similarly, commercial vehicle production and sales accounted for 948000 and 938000 units, respectively, with an increase of 3.9% and 2.9% year-on-year.

- According to the International Organization of Motor Vehicle Manufacturers(OICA), the world's total passenger car production in 2022 was 61,598,650; in 2021, it was 57,054,295 units. The demand for vehicles is expected to rise due to several factors, such as increased demand for private mobility and exponential growth in electric vehicles during the forecast period.

- The demand for 3D printing materials in the automotive industry is expected to grow due to the above factors.

Asia-Pacific is Expected to Grow at a Fastest Rate

- Asia-Pacific is among the fastest-growing economies globally, comprising China as one of the fastest-growing countries globally, and almost all the end-user industries have been growing due to the rising population, living standards, and per capita income.

- The region comprises several countries with noteworthy production in the automotive sector. Moreover, the emergence of electric vehicles is expected to further provide substantial growth opportunities in the 3D printing materials market.

- In 2022, several countries, such as India, Indonesia, Malaysia, and Vietnam, were expected to grow tremendously in automotive production. For instance, according to the International Organization of Motor Vehicle Manufacturers (OICA), in 2022, the total production of motor vehicles in India and Indonesia stood at 5,456,857 and 1,470,146 units, respectively, showing growth of 24% and 31% compared to the previous year.

- On September 20, 2022, the Ministry of Finance (MOF), the Ministry of Industry and Information Technology (MIIT), and the State Taxation Administration (STA) jointly announced that the purchase of new energy vehicles (NEVs) from January 2023 to December 2023 would be exempt from the vehicle purchase tax. This supports the demand for and sales of new electric vehicles in China.

- Furthermore, the layer-by-layer deposition process in 3D printing allows sensors, antennas, and other functional electronics to be printed directly onto plastic components, metal surfaces, glass panels, and ceramic materials.

- According to a report by the China Academy of Information and Communications Technology, during the first two months of 2022, the electronics manufacturing industry maintained a steady expansion. The added value of major electronics manufacturers from January to February 2022 increased by 12.7% yearly; however, overall industrial growth stood at 7.5% during the same period.

- China is among the fastest-growing markets regarding new technologies and using innovative materials for construction. With China's dominating role as a global construction center, the accelerated development of 3D printing in the home printing sector is likely to revolutionize the traditional construction industry in the country, with applications ranging from residential buildings to monuments. The country managed to 3D print homes and other large-scale structures, making every other country look into the possibilities of 3D printing in construction.

- There are a few limitations to 3D printing in the construction sector, such as a lack of confidence from building developers and the absence of proper regulations for using this technology. However, with increasing awareness of new technologies and their advantages, organizations, and individuals are increasingly considering cost-saving alternatives. This, in turn, is driving demand in the 3D printing materials market in the country.

- Owing to all the abovementioned factors, the demand for 3D printing materials in Asia-Pacific is expected to drive the market studied.

3D Printing Materials Industry Overview

The 3D printing materials market is consolidated, with few players holding the major share in the market. Key players in the 3D printing materials market (not in any particular order) include Stratasys, BASF SE, Evonik Industries AG, Arkema, and 3D Systems Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Usage in Manufacturing Applications

- 4.1.2 Mass Customization Associated with 3D Printing

- 4.1.3 Surge in Demand in Automotive Application

- 4.2 Restraints

- 4.2.1 High Equipment and Material Cost

- 4.2.2 Availability of Limited Types of Materials

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Material Type

- 5.1.1 Plastics

- 5.1.1.1 Acrylonitrile Butadiene Styrene (ABS)

- 5.1.1.2 Polylactic Acid (PLA)

- 5.1.1.3 Nylon

- 5.1.1.4 Polyamide

- 5.1.1.5 Polycarbonates

- 5.1.1.6 Other Plastics

- 5.1.2 Ceramics

- 5.1.3 Metals

- 5.1.4 Other Material Types

- 5.1.1 Plastics

- 5.2 Form

- 5.2.1 Powder

- 5.2.2 Filament

- 5.2.3 Liquid

- 5.3 End-user Industry

- 5.3.1 Automotive

- 5.3.2 Medical

- 5.3.3 Aerospace and Defense

- 5.3.4 Consumer Electronics

- 5.3.5 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Singapore

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3D Systems, Inc.

- 6.4.2 Arkema

- 6.4.3 BASF SE

- 6.4.4 CRP TECHNOLOGY S.r.l.

- 6.4.5 CRS Holdings, LLC

- 6.4.6 ENVISIONTEC US LLC

- 6.4.7 EOS

- 6.4.8 Evonik Industries AG

- 6.4.9 General Electric

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Hoganas AB

- 6.4.12 Materialise

- 6.4.13 Sandvik AB

- 6.4.14 Solvay

- 6.4.15 Stratasys

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Introduction of New Materials, like Graphene Opens Up New Applications

- 7.2 Adoption of 3D Printing Technology in Home Printing