|

市場調査レポート

商品コード

1687294

スマートコーティング-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Smart Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スマートコーティング-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

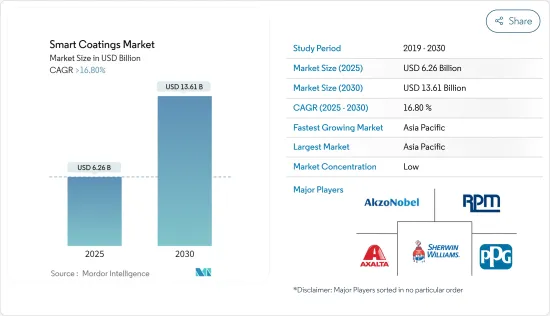

スマートコーティング市場規模は2025年に62億6,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは16.8%以上で、2030年には136億1,000万米ドルに達すると予測されます。

COVID-19パンデミックは市場にマイナスの影響を与えたが、パンデミック後は、世界の建設、自動車、航空宇宙、防衛など様々なエンドユーザー産業の成長により、予測期間中に市場は安定的に成長すると予測されます。

主要ハイライト

- 短期的には、従来の塗料よりも優れた特性と建設産業からの需要の高まりが市場を牽引すると予想されます。

- その一方で、スマートコーティングのコストが高いことが市場を抑制し、成長の妨げになると予想されます。

- 機能性を向上させるためにナノ粒子の使用が増加していることや、様々なエンドユーザー産業において従来のコーティングに代わってスマートコーティングが使用される機会が増えていることは、今後数年間で市場に機会をもたらすと予測されます。

- 予測期間中、アジア太平洋が市場を独占し、最も高い成長率を示すと予想されます。

スマートコーティング市場の動向

建築・建設産業で需要が拡大

- セルフクリーニングのようなスマートコーティングは、特に高層商業ビルやオフィスビルで、メンテナンスを容易にするために建物のガラス壁に使用されています。抗菌コーティングは、病院、キッチン、公衆浴場などで幅広く利用されています。防錆コーティングはインフラや工業用建物にも使用されています。

- アジア太平洋の建設セクターは世界最大です。人口の増加、中間所得層の増加、都市化により、健全なペースで増加しています。

- 中国国家統計局によると、同国の建設工事の生産額は、2022年の31兆2,000億人民元(4兆3,700億米ドル)に対し、2023年には31兆5,900億人民元(4兆4,300億米ドル)となり、市場の需要を高めています。

- 住宅建設とは別に、アジア太平洋は近年オフィススペース市場として活況を呈しており、商業建設産業では最大市場のひとつです。

- 米国国勢調査局によると、建物・建設産業は米国経済の重要なコンポーネントであり、745,000以上の企業が関与しています。2023年の建設支出は全体で1兆9,800億米ドルに上り、前年比7.4%増となります。

- 欧州委員会が発表したデータによると、2023年12月の建設生産の伸びは、2022年12月と比較して、ユーロ圏全体で1.9%、欧州連合全体で2.4%でした。2023年の建設生産の対2022年比の平均増加率は、ユーロ圏で0.2%、欧州連合で0.1%であり、これにより国内の様々な建設用途でのスマートコーティングの消費が促進されました。

- したがって、このような建設活動の堅調な成長が市場の需要を促進しています。

中国がアジア太平洋を支配する見込み

- アジア太平洋は、市場シェアで世界のスマートコーティング市場を独占しています。建設活動の増加や自動車産業の成長といった要因が市場を後押ししています。

- スマートコーティングは、中国の建築・建設産業でますます使用されるようになっています。中国は世界最大の建設産業です。さらに、いくつかの大規模な建設プロジェクトが進行中であることから、中国は当面最大の建設産業としての地位を維持すると予想されます。

- 中国は、経済成長に支えられた豊富な住宅・商業建設開発が大きな原動力となっています。中国では、香港の住宅当局が低価格住宅の建設を推進するため、いくつかの施策を開始しました。当局は、2030年までに10年間で30万1,000戸の公共住宅を供給することを目指しています。

- インドの建設産業は、2025年までに1兆4,000億米ドルに成長すると予測されています。2030年までに推定6億人が都心部に住むようになり、その結果、2,500万戸の中・超高級住宅が追加で必要となります。国家投資計画(NIP)のもと、インドのインフラ投資予算は1兆4,000億米ドルで、24%が再生可能エネルギー、道路・高速道路、都市インフラ、12%が鉄道に割り当てられています。

- インドでは、GDP全体に対する自動車産業の貢献度は7.1%です。製造業GDPの49%を占め、年間売上高は7兆5,000億インドルピー、輸出額は3兆5,000億インドルピーです。

- また、2022年には5,457万台だった自動車生産台数は、2023年には5,851万台となります。

- 国連貿易開発会議(UNCTAD)によると、2022年初の日本の商業フリートの重量トンは4,026万3,340トンで、2021年初の3,931万2,530トンと比べて2.42%の成長率を記録し、それによって国内のスマートコーティング需要が増加しています。

- 予測期間中、上記のすべての要因が市場を拡大すると予想されます。

スマートコーティング産業概要

スマートコーティングの世界市場は半固体化しています。同市場の主要企業には、Akzo Nobel NV、PPG Industries Inc.、The Sherwin-Williams Company、RPM International Inc.、Axalta Coating Systems, LLCが含まれます(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 従来のコーティングよりも優れた特性

- 建設産業からの需要の高まり

- 抑制要因

- スマートコーティングのコスト高

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 機能

- 防汚

- 抗菌

- 防錆

- 氷結防止

- セルフクリーニング

- カラーシフト

- その他

- エンドユーザー産業

- 建築・建設

- 自動車

- 海洋

- 航空宇宙・防衛

- その他

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- その他

- 南米

- 中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Akzo Nobel NV

- Axalta Coating Systems LLC

- Dupont

- Hempel AS

- Jotun

- NEI Corporation

- PPG Industries Inc.

- RPM International Inc.

- The Sherwin-Williams Company

第7章 市場機会と今後の動向

- 機能性向上のためのナノ粒子利用の増加

- 様々なエンドユーザー産業で従来のコーティングを置き換えるスマートコーティングの機会が増加

The Smart Coatings Market size is estimated at USD 6.26 billion in 2025, and is expected to reach USD 13.61 billion by 2030, at a CAGR of greater than 16.8% during the forecast period (2025-2030).

The COVID-19 pandemic had a negative impact on the market; however, post-pandemic, the market is projected to grow steadily during the forecast period owing to growth in various end-user industries like construction, automotive, aerospace, and defense worldwide.

Key Highlights

- In the short term, superior properties over traditional coatings and rising demand from the construction industry are expected to drive the market.

- On the other hand, the high cost of smart coatings is expected to restrain the market and hinder its growth.

- The increasing use of nanoparticles to improve functionality and opportunities for smart coatings to replace conventional coatings in various end-user industries are projected to create an opportunity for the market in the coming years.

- Asia-Pacific is expected to dominate the market and witness the highest growth rate during the forecast period.

Smart Coatings Market Trends

The Building and Construction Industry is Experiencing a Growing Demand

- Smart coatings like self-cleaning are used on glass walls in buildings for easier maintenance, especially for high-rise commercial and office buildings. Anti-microbial coatings have extensive applications in hospitals, kitchens, and public bathrooms. Anti-corrosion coatings are also used in infrastructure and industrial buildings.

- The construction sector in Asia-Pacific is the largest in the world. It is increasing at a healthy rate, owing to the rising population, increase in middle-class income, and urbanization.

- According to the National Bureau of Statistics of China, the output value of construction works in the country was CNY 31.59 trillion (USD 4.43 trillion) in 2023 compared to CNY 31.2 trillion (USD 4.37 trillion) in 2022, thereby enhancing the demand in the market.

- Apart from residential construction, Asia-Pacific has been a thriving market for office spaces in recent years and is one of the largest markets in the commercial construction industry.

- According to the United States Census Bureau, the buildings and construction industry is a key component of the United States economy, with more than 745,000 businesses involved. In 2023, the overall expenditure on construction climbed to USD 1.98 trillion, signifying a 7.4% rise compared to the year before.

- As per the data released by the European Commission, growth in construction production in December 2023 compared to December 2022 was 1.9% across the euro area and 2.4% across the European Union. The Y-o-Y average increase in construction production in 2023 compared to 2022 was 0.2% for the euro area and 0.1% for the European Union, thereby enhancing the consumption of smart coatings from various construction applications in the country.

- Hence, such robust growth in construction activities is fuelling the demand in the market.

China is Expected to Dominate the Asia-Pacific Region

- Asia-Pacific dominated the global smart coatings market in terms of market share. Factors such as increasing construction activities and the growth of the automotive industry are favoring the market.

- Smart coatings are increasingly used in China's building and construction industry. China has the world's largest construction industry. Moreover, with several major construction projects in progress, China is expected to maintain its status as the largest construction industry in the foreseeable future.

- China has been majorly driven by ample residential and commercial construction developments supported by the growing economy. In China, the housing authorities of Hong Kong launched several measures to push start the construction of low-cost housing. The officials aim to provide 301,000 public housing units in 10 years by 2030.

- India's construction industry is projected to grow to USD 1.4 trillion by 2025. By 2030, an estimated 600 million people will live in urban centers, resulting in a need for 25 million additional mid- and ultra-luxury units. Under the National Investment Plan (NIP), India has an infrastructure investment budget of USD 1.4 trillion, with 24% earmarked for renewable energy, roads and highways, urban infrastructure, and 12% for railways.

- In India, the automobile industry's contribution to the overall GDP stands at 7.1%. It is 49% of the manufacturing GDP, with an annual turnover of INR 7.5 lakh crore (USD 0.010 million) and an export of INR 3.5 lakh crore (USD 0.0047 million).

- In addition, in 2023, 58.51 million vehicles were produced in the country, compared to 54.57 million units in 2022.

- According to the UN Conference on Trade and Development (UNCTAD), Japan's merchant fleet accounted for 40,263.34 thousand dead-weight tons at the start of 2022, registering a growth rate of 2.42%, compared to 39,312.53 thousand dead-weight tons at the beginning of 2021, thereby, increasing the demand for smart coatings in the country.

- All the above-mentioned factors are expected to augment the market during the forecast period.

Smart Coatings Industry Overview

The global market for smart coatings is semi-consolidated. Major players in the market include Akzo Nobel NV, PPG Industries Inc., The Sherwin-Williams Company, RPM International Inc., and Axalta Coating Systems, LLC (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Superior Properties Over Traditional Coatings

- 4.1.2 Growing Demand from the Construction Industry

- 4.2 Restraints

- 4.2.1 High Cost of Smart Coatings

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size In Revenue)

- 5.1 Function

- 5.1.1 Anti-fouling

- 5.1.2 Anti-microbial

- 5.1.3 Anti-corrosion

- 5.1.4 Anti-icing

- 5.1.5 Self-cleaning

- 5.1.6 Color-shifting

- 5.1.7 Other Functions

- 5.2 End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Automotive

- 5.2.3 Marine

- 5.2.4 Aerospace and Defense

- 5.2.5 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Akzo Nobel NV

- 6.4.3 Axalta Coating Systems LLC

- 6.4.4 Dupont

- 6.4.5 Hempel AS

- 6.4.6 Jotun

- 6.4.7 NEI Corporation

- 6.4.8 PPG Industries Inc.

- 6.4.9 RPM International Inc.

- 6.4.10 The Sherwin-Williams Company

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing use of Nanoparticles to Improve Functionality

- 7.2 Increasing Opportunities for Smart Coatings to Replace Conventional Coatings in Various End-user Industries