|

市場調査レポート

商品コード

1851120

航空エンジン用複合材料:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Aeroengine Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空エンジン用複合材料:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月17日

発行: Mordor Intelligence

ページ情報: 英文 124 Pages

納期: 2~3営業日

|

概要

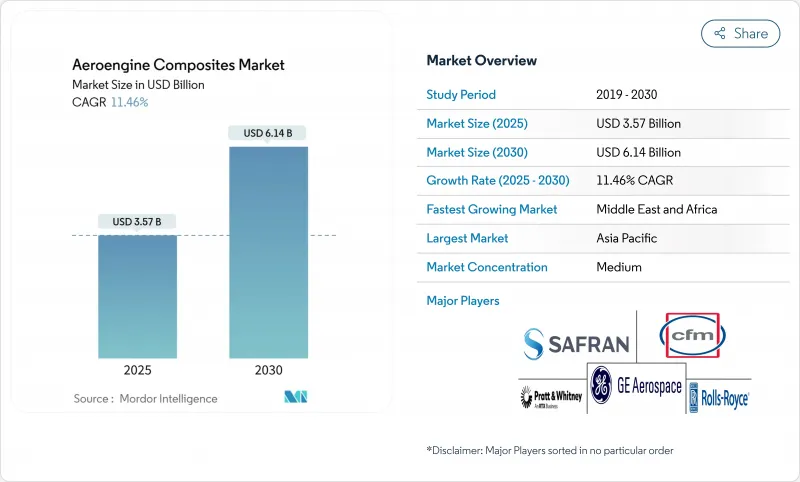

航空エンジン用複合材料市場の2025年の市場規模は35億7,000万米ドルで、2030年には61億4,000万米ドルに達し、CAGR 11.46%で成長すると予測されています。

航空機の更新の増加、脱炭素化の義務化、燃料価格の上昇により、航空会社やエンジンメーカーは、より厳しい排出規制を満たしながら燃料消費を最大20%削減する、より軽量な推進システムを求めています。セラミック・マトリックス複合材料(CMC)は、現在では1,300℃に耐えられるようになり、コア温度の上昇と熱効率の改善が可能になりました。自動化された繊維配置とオートクレーブ外での硬化により、1ポンド当たりのコストが30%近く低下し、複合材がナローボディ・プログラムで経済的に実行可能なものとなっています。GEエアロスペースが2024年に10%の納期不足に陥ったことで、高圧タービンブレード調達のボトルネックが露呈したため、サプライチェーンの弾力性は依然として重要です。

世界の航空エンジン用複合材料市場の動向と洞察

軽量で燃料効率の高い推進システムへのシフト

航空会社は、変動する燃料価格を相殺するために15~20%の燃料節減を必要としており、ナセルの重量を削減しバイパス比を高める複合材への急速な軸足を動かしています。GEエアロスペースのRISEオープンファン実証機は、バイパス比60までの炭素繊維ファンブレードを使用し、20%のCO2削減を目標としています。エアバスは、100%持続可能な航空燃料と組み合わせる炭素繊維強化熱可塑性プラスチック構造の飛行試験を行っており、20%の燃料消費削減を約束しています。月産100機を超えるナローボディの生産量は、スケーラブルで自動化された複合材生産の緊急性を高めています。

LEAPと次世代航空機エンジンの生産量拡大

4,000機以上の航空機がLEAPエンジンを搭載して飛行しているため、サフランはブリュッセル、ハイデラバード、ケレタロ、カサブランカにある新しいMRO施設に10億ユーロ(11億6,000万米ドル)を投資し、2028年までに年間1,200件の工場訪問に対応します。GEは6,400万ユーロ(7,405万米ドル)を、LEAPとGE9Xプログラムをサポートする欧州のテストセルと工具に充当しました。高圧タービンブレードを中心とする部品不足は、269億米ドルの商業収益にもかかわらず、2024年のエンジン納入を10%削減し、多様な複合材サプライチェーンの必要性を浮き彫りにしました。

CMCの脆さと検査の複雑さ

CMCファンブレードは、そのセラミック微細構造が衝撃荷重で割れる可能性があるため、異物損傷のリスクがあります。従来の超音波法やX線法ではマイクロクラックの検出が困難なため、OEMはCTスキャンや専門家トレーニングへの投資を余儀なくされています。多結晶ダイヤモンド工具を使用する新しい機械加工法は、加工時間を70%短縮するため、資本コストが上昇し、小規模なサプライヤーにとっては採用が難しくなっています。

セグメント分析

商用エンジンは、2024年に航空エンジン用複合材料市場シェアの70.05%を占めるが、これは何千ものLEAPとGEnxユニットが複合材ファンブレードとケースを統合し、最大20%の燃料節約を実現しているためです。軍事プログラムに関連する航空エンジン用複合材料市場規模は、XA100クラスの推進力と極超音速実証機がCMCシュラウドを採用するため、2030年までのCAGRが12.74%で最も急速に拡大します。

ビジネスジェット機やリージョナル航空機の運航会社は、技術の下流への移行に伴い、複合材を多用したエンジンの改修を始めています。GEエアロスペース社やクレイトス・ディフェンス社のようなパートナーシップは、CMCタービンと手頃な生産方法を組み合わせた小型クラスのエンジンを計画しており、顧客ベースを広げています。これにより、民間予算と防衛予算にまたがるリスクが分散され、サプライヤーの受注安定性が向上します。

ファンブレードは2024年の売上高の37.98%を占め、これはカーボンファイバー構造が高剛性対重量を実現し、慣性を減らして推力応答を改善するためです。ファンケースは13.48%のCAGRで成長すると予測され、規制の格納テストでは複合材シェルが好まれるため、格納ハードウェアの航空エンジン用複合材料市場規模を引き上げます。

シュラウド、ガイドベーン、Oリングシールをモノリシック複合材構造に統合することで、部品点数と組立時間を削減し、マージンを健全に保つことができます。AFP機能を持つサプライヤーは、複雑なエアロコイルを1回のパスで加工でき、性能の一貫性を高めることができます。

地域分析

中国がC919用のCJ-1000や推力35トンのCJ-2000のような土着プログラムを加速させたため、アジア太平洋は2024年に32.18%のシェアを占めました。中国のタービンブレードは現在、単結晶鋳造と3Dプリンターによる冷却チャンネルによって1,700℃に耐えられるようになっています。日本と韓国は高強度ファイバーとプリプレグを供給し、インドのワイドボディの受注がこの地域の需要を押し上げています。

北米は依然として技術リーダーです。GEエアロスペースの2024年における269億米ドルの商用エンジンの売上は、複合材をふんだんに使ったLEAPとGEnxプログラムに起因するものだが、材料不足で納入が10%減少しました。NASAのHyTECイニシアチブは、単通路の効率を上げるためにCMC翼をコーティングしており、研究開発パイプラインを維持しています。

中東・アフリカは、湾岸キャリアが複合材を多用したエンジンを追加し、地域勢力が次世代戦闘機に投資するため、CAGR13.15%と最も速い成長が予測されます。サフランMTUのEURAエンジンは、欧州のヘリコプターのアップグレードの中核となり、EUクリーンアビエーションのオープンファン実証機は、大口径複合材ファンによる20%のCO2削減をサポートします。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 軽量で低燃費の推進システムへのシフト

- LEAPとGEnxエンジンの生産量拡大

- 脱炭素ロードマップが高温CMC需要を牽引する

- アフターマーケットの消費は複合補修部品にシフトしている

- 製造工程の自動化によるコスト削減

- 極超音速および第6世代戦闘機製造のための資金増加

- 市場抑制要因

- CMCの脆さと検査の複雑さ

- 限られた高温樹脂供給ベース

- 新ラインへの設備投資を延期する不安定な建設率

- FAA/EASAパート21規則による5~7年にわたる材料/プロセス適格性確認サイクル

- バリューチェーン分析

- 規制とテクノロジーの展望

- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 用途別

- 民間航空機

- ナローボディ

- ワイドボディ

- リージョナルジェット

- 軍用機

- 一般航空機

- ビジネスジェット

- その他

- 民間航空機

- コンポーネント別

- ファンブレード

- ファンケース

- ガイドベーン

- シュラウド

- その他の部品

- 素材タイプ別

- ポリマーマトリックスコンポジット(PMC)

- セラミック・マトリクス・コンポジット(CMC)

- エンドユーザー別

- OEM

- アフターマーケット

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 南米

- ブラジル

- その他南米

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- GE Aerospace(General Electric Company)

- CFM International

- Rolls-Royce plc

- Pratt & Whitney(RTX Corporation)

- Safran SA

- GKN Aerospace

- FACC AG

- Spirit AeroSystems Inc.

- Hexcel Corporation

- Toray Industries, Inc.

- Solvay

- Albany International Corp.

- Meggitt PLC

- General Dynamics Corporation

- SGL Carbon

- Renegade Materials Corporation

- Materion Corporation

- IHI Corporation

- MTU Aero Engines AG