|

市場調査レポート

商品コード

1851012

弾性床材:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Resilient Floor Covering - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 弾性床材:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月17日

発行: Mordor Intelligence

ページ情報: 英文 156 Pages

納期: 2~3営業日

|

概要

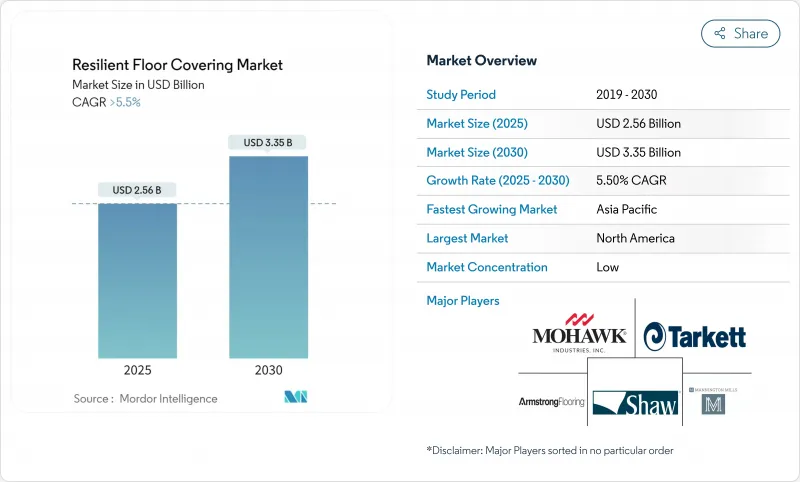

弾性床材市場の2025年の市場規模は25億6,000万米ドルで、CAGR 5.5%を反映して2030年には33億5,000万米ドルに達すると予測されています。

安定した需要は、住宅における高級ビニルタイル(LVT)のアップグレード、アジア太平洋におけるヘルスケア建設のパイプラインの拡大、セラミック、ラミネート、ハードウッドに対して弾力性のある床材の競争力を維持する着実な製品革新に起因します。デジタル印刷、エンボス・イン・レジスター・テクスチャリング、リジッドコア・エンジニアリングはデザインの選択肢を広げ、耐衝撃性を向上させました。米国環境保護庁はDINP可塑剤のリスク評価案を発表し、特定の使用条件下での人体リスクの可能性を指摘しました。北米と欧州におけるニアショア生産へのサプライチェーン・シフトは、関税の影響とリードタイムを削減し、現地在庫の管理を容易にしています。耐水性と容易な衛生を重視する気候主導の建築基準により、弾性床材市場はさらに採用が強化され、より広い仕上げ材セクターの中で信頼できる成長セグメントとして位置づけられています。

世界の弾性床材市場の動向と洞察

住宅リフォームにおけるLVTの急速な採用

住宅リフォームは、依然としてLVTの主要な需要エンジンです。住宅所有者は、リアルなビジュアル、手頃な価格、キッチン、ダイニングエリア、ファミリールームをつなぐオープンプランのレイアウトを簡素化する耐湿性などを理由にLVTを選んでいます。デジタル印刷により、天然素材に匹敵するシャープな木や石のグラフィックが低価格で実現され、クリックロック・プロファイルにより接着剤が不要で施工時間が短縮されます。2024年に住宅着工が停滞した際にも、LVTはカーペットやラミネートを駆逐してシェアを拡大し、不況時の回復力を示しました。この要因は、米国、ドイツ、フランス、オーストラリアでの買い替えプロジェクトを中心に、少なくとも2027年まで弾性床材市場を大きく押し上げます。

衛生的で滑りにくい床を必要とするアジア太平洋地域のヘルスケア構築

中国、インド、インドネシア、ベトナムで建設中の病院や診療所では、微生物の繁殖を抑え、厳格な感染管理を可能にするシームレスな無孔シートが求められています。サプライヤーは現在、進化する衛生基準に適合させるため、一体化されたコーブ・ライズ・ディテール、熱溶着シーム、埋め込み抗菌層を組み合わせています。アジア各国政府は、重症病棟用の特殊床材に補助金を出しており、安定した入札量を生み出しています。インドだけでも2028年まで2,000床以上の公共施設の増床が予定されており、ヘルスケア建設は弾性床材市場に一貫した勢いをもたらしています。

塩ビ原料価格の変動がマージンを圧迫

ポリ塩化ビニルのコストは石油・エネルギー市場とともに変動し、価格表を乱し、特に後方統合を欠く生産者にとっては利幅を圧迫しています。2024年の価格高騰は、大規模な商業入札で急速な再見積もりを余儀なくさせ、流通業者との関係を緊張させました。バイオ原料ビニールを推進する欧州とリサイクル・プログラムを推進する北米が部分的な緩衝材となっているが、予測不能な投入コストは弾性床材市場全体の収益性の足を引っ張り続けています。

セグメント分析

高級ビニルタイルは全体の需要の30.23%を占め、弾性床材市場で最も汎用性の高い製品です。高精細グラフィック、低メンテナンス性、競争力のある価格設定により、引き続き主導権を握っています。石材プラスチック複合材は、凹凸のある基材上でもテレグラフを最小限に抑え、より強い衝撃にも耐える剛性の高いコアが強みで、CAGR 8.33%でさらに急速に拡大しています。ウッド・プラスティック・コンポジットは、価格プレミアムが販売量を抑制しているもの、足元の感触が柔らかく、音響効果に優れているため、住宅用としては上層部での地位を維持しています。従来のビニールシートは、手術室や教育用廊下で使用されており、溶接継ぎ目が衛生面を向上させています。ビニールコンポジションタイルは、施設バイヤーがノーワックスにシフトしているため、減少を続けています。ニッチな代替品であるリノリウム、ゴム、コルクは、持続可能性の評価と特殊な音響ニーズにより、総売上高の約15%に相当します。

SPCの石灰石で補強された背板は、施工業者に熱の変化に耐える寸法安定性のある板を提供し、サンベルト市場やガラス張りの高層ビルでのプロジェクトを支えています。メーカー各社は、LVTとSPCを1つのシフトで交互に使用できるハイブリッド生産ラインを稼働させ、バランスの取れた在庫と迅速な注文サイクルを維持しています。量販店は、清掃が簡単でへこみにくく、生涯コストが低いことを宣伝し、リジッドコアの認知度を拡大し、弾性床材市場規模階層内でのシェア拡大を加速させています。

グルーダウン工法は、2024年の販売量の46.89%を占めています。病院、スーパーマーケット、学校などでは、転がる機器や人の往来が多いため、浮き床では支えきれないせん断荷重がかかるため、恒久的な接着が不可欠だからです。また、溶接による継ぎ目で一枚岩のカバーが形成されるため、衛生管理が容易になります。しかし、請負業者が施工期間の短縮と人件費の削減を求めているため、クリックロック式床板はCAGR 7.79%で成長しています。エッジを軽くたたくだけでロックできるため、施工業者は1日で最大100㎡をカバーすることができ、忙しい家庭のダウンタイムを短縮し、商業施設の改装を迅速に進めることができます。より重いタイルを摩擦と周囲テープで固定するルーズレイ形式は、床下ケーブルへのアクセスが不可欠なデータセンターやオフィスに対応します。多様な設置方法の選択肢は、並行的な成長軌道を維持し、弾性床材市場の全体的な適応性を高めています。

地域分析

欧州は、厳しい室内空気規制、改修補助金、クローズドループリサイクルを奨励する循環経済指令によって支えられており、世界売上高の31.99%を占めています。ドイツとフランスは社会住宅の改修で需要を支えており、スカンジナビアの自治体はバイオベースのリノリウムを学校に採用しています。TarkettのReStart(R)プログラムは、現場の端材や使用済み材料を回収し、材料回収のための地域的な青写真を示しています。建物の外壁を密閉し、低VOC表面を追加する居住者にはエネルギー効率補助金が支給されるため、改修への支出は引き続き活発で、既存の下地に弾力性のある床材を素早く施工できることが好まれています。

アジア太平洋地域はCAGR 9.19%と最も急速に成長しており、巨大都市の住宅タワー、病院の拡張、可処分所得の拡大に支えられています。中国だけでも、数百万平方メートルの弾力性シートが公立病院や大型小売モールに使用されています。インドの都市住宅ミッションでは、モンスーンの湿度に耐える費用対効果の高い防水ソリューションが求められています。日本と韓国は、軽量鉄骨造を補完するために、高級な防音層を要求しています。ASEAN全体では、インドネシア、タイ、ベトナムのインフラ・パイプラインが、建設業者がセラミック・タイルから扱いやすいクリック・ロック・プランクに軸足を移すにつれて消費を拡大し、弾性床材市場のスケールアウト軌道を強化しています。

北米は世界の売上高の約4分の1を占めており、関税措置が急速なオン・ショアリングの引き金となっています。ジョージア州とオンタリオ州に新設されたラインは、現地のディストリビューターをサポートし、出荷時間の短縮と供給の確保を実現しています。カナダの各州は地方施設向けに低VOC製品を指定し、メキシコは自由貿易の枠組みの下で国内住宅と輸出機会に対応する能力を増強しています。同地域では、住宅ストックの老朽化に伴う改修が一貫して行われており、地下室や1階の増築部分における歴史的な湿気の問題を解決するためにSPC板が選ばれることが多いです。一戸建て、集合住宅、軽商用と需要の多様化は、北米の弾性床材市場規模の構造的安定性を高めています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 住宅改修におけるLVTの急速な導入

- アジア太平洋のヘルスケア建設には衛生的で滑りにくい床が必要

- 耐候性住宅における防水SPC/WPCの需要

- デジタル印刷とEIR仕上げで美観を高める

- 低VOC規制がエコラベル付き弾力性材料を促進

- 円形リノリウムとPVCの回収でグリーン認証を強化

- 市場抑制要因

- PVC原料価格の変動が利益率を圧迫

- アジアのLVTに対する反ダンピング関税

- 塩素化プラスチックの環境調査

- 熟練した設置者の不足が故障率を上昇させる

- バリュー/サプライチェーン分析

- 規制の見通し

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品タイプ別

- 高級ビニールタイル(LVT)

- ドライブック(接着)

- クリックロックフローティング

- ルーズレイ

- ビニールシート

- ビニールコンポジションタイル(VCT)

- 石材プラスチック複合材(SPC)/剛性コア

- 木材プラスチック複合材(WPC)

- リノリウム

- ゴム

- コルク

- 高級ビニールタイル(LVT)

- 設置タイプ別

- 接着式

- フローティング/クリックロック

- ルーズレイ

- エンドユーザー業界別

- 住宅用

- 商業用

- ヘルスケア施設

- 教育施設

- 小売店とスーパーマーケット

- ホスピタリティ&レジャー

- 本社

- 工業・製造業

- 流通チャネル別

- オフライン

- 専門店

- ホームセンターとDIYチェーン店

- オンライン

- オフライン

- 地域

- 北米

- カナダ

- 米国

- メキシコ

- 南米

- ブラジル

- ペルー

- チリ

- アルゼンチン

- その他南米

- アジア太平洋地域

- インド

- 中国

- 日本

- オーストラリア

- 韓国

- 東南アジア(シンガポール、マレーシア、タイ、インドネシア、ベトナム、フィリピン)

- その他アジア太平洋地域

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- イタリア

- ベネルクス(ベルギー、オランダ、ルクセンブルク)

- 北欧諸国(デンマーク、フィンランド、アイスランド、ノルウェー、スウェーデン)

- その他欧州地域

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- ナイジェリア

- その他中東・アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Mohawk Industries Inc.

- Tarkett S.A.

- Shaw Industries Group Inc.

- Armstrong Flooring LLC(AHF Products)

- Mannington Mills Inc.

- Gerflor Group

- Forbo Flooring Systems

- Interface Inc.

- LG Hausys(LX Hausys)

- Nora Systems GmbH

- Polyflor Ltd(James Halstead)

- Engineered Floors LLC

- Karndean Designflooring

- Responsive Industries Ltd.

- CFL Flooring

- Beaulieu International Group

- Parterre Flooring Systems

- Novalis Innovative Flooring

- Milliken & Company

- Fatra a.s.

- IVC Group(BerryAlloc)

- Upofloor(Kahrs Group)*