|

市場調査レポート

商品コード

1851819

コールドチェーン包装:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Cold Chain Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| コールドチェーン包装:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月13日

発行: Mordor Intelligence

ページ情報: 英文 106 Pages

納期: 2~3営業日

|

概要

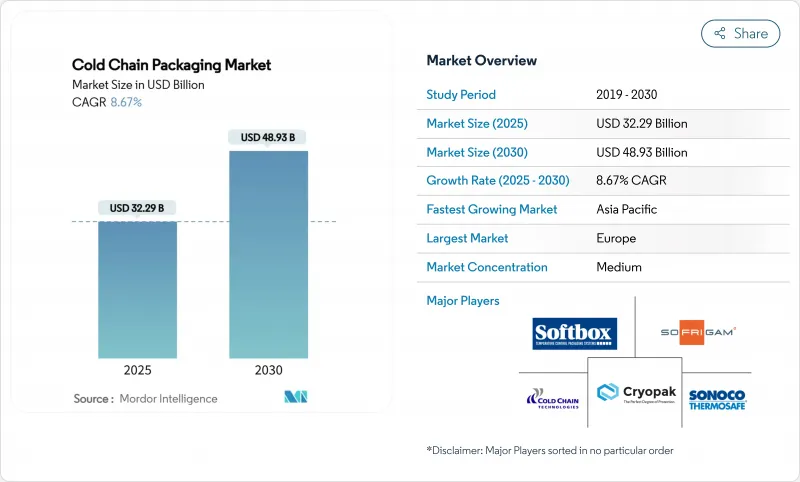

コールドチェーン包装市場規模は2025年に322億9,000万米ドル、2030年には489億3,000万米ドルに達し、CAGR 8.67%で拡大すると予測されています。

成長を支えているのは、生物製剤の数量増加、eコマースによる食料品フルフィルメントの拡大、温度管理された流通を標準化する世界的なワクチン構想です。米国食品医薬品局(FDA)の21 CFR 600.15や欧州連合(EU)の新包装・包装廃棄物規制といった規制の枠組みは、有効なソリューションを義務付ける一方で、リアルタイムのIoTモニタリングはパフォーマンスへの期待を高めています。また、企業のESG目標が再利用可能でバイオベースのフォーマットへの軸足を加速させ、コールドチェーン包装市場全体のサプライヤー戦略を再構築しています。

世界のコールドチェーン包装市場の動向と洞察

生物製剤と細胞・遺伝子治療ロジスティクスのブーム

新医薬品の半数近くが温度管理を必要とし、多くの先端療法は-150℃以下の極低温条件を必要とします。2025年1月、Cryoport社はこのような超低温レベルを長時間維持するHV3シッパーを発表し、この分野が特殊設計にシフトしていることを示しています。FDAの生物製剤認可要件は、輸送中の安定性を証明する有効な証拠を要求しており、包装の適格性は製品認可に不可欠となっています。個別化医療の動向は出荷頻度と出荷額を増加させ、コールドチェーン包装市場全体のプレミアム需要を促進します。

eコマース食料品とミールキット宅配の拡大

チルド食品と冷凍食品のオンライン食料品販売量が増加し、ラストマイルの変動に耐える軽量でスペース効率の高い断熱材へのニーズが高まる。HelloFresh社はAIを採用し、天候やルートの特定に合わせてパック構成を調整することで、データによる材料選択を実証しています。2024年4月に発売されたRanpakのカーブサイドリサイクル可能なclimaliner Plusは、72時間の熱保護を提供し、消費者の持続可能性への期待に応えます。これらのイノベーションは、コールドチェーン包装市場を従来の医薬品レーンを超えて拡大します。

ポリマー原料価格の変動

ポリエチレンやポリプロピレンのコストが上振れすると、コンバーターのマージンが圧迫され、初期費用がかさむ再利用可能な包装への切り替えが遅れる可能性があります。小規模なメーカーはヘッジの仕組みがないことが多く、ポートフォリオを合理化し、高価値の医薬品アカウントを優先するよう促しています。

セグメント分析

断熱容器は出荷の基幹となり、2024年のコールドチェーン包装市場の35.53%を占めました。このような優勢にもかかわらず、サプライチェーンが継続的な可視化を求めているため、温度監視装置のCAGRは12.95%を記録しています。Timestrip社のセマグルチドインジケーターのようなスマートラベルは、高価値の生物製剤にもコンプライアンスを拡大し、ヘルスケアプロバイダー全体で採用されています。

IoTチップと低消費電力ネットワークの融合は、パッシブボックスをコネクテッドアセットにアップグレードします。SkyCell社の1500Xハイブリッド・コンテナは270時間稼動し、ライブ・データを送信します。このような進歩は、現在では実績のあるリスク低減に報いる保険会社を惹きつけ、コールドチェーン包装市場内の機器メーカーにとって対応可能な数量を拡大しています。

2024年のコールドチェーン包装市場規模では、パッシブシッパーが55.32%のシェアを維持し、シンプルさと規制へのなじみの良さが評価されています。しかし、ハイブリッド型は、従来のシェル内にセンサーと限定的な電力補助を組み込むことで、コストと制御のバランスをとり、CAGR最速の10.32%を記録します。Va-Q-TecのThermal Coatは、レガシーボックスにインテリジェントなレイヤーを追加し、完全電源ユニットへの依存を軽減します。

世界の航空会社はリチウム電池の輸送規則を強化し、充電状態の上限を30%に設定しています。ソーラーハーベスティングとスーパーキャパシタの統合は、このハードルを軽減し、メーカーをパッシブ・アクティブ・ハイブリッドに向かわせる。コンプライアンス監査が強化されるにつれて、トレーサビリティを内蔵した荷送人が調達を選好するようになり、コールドチェーン包装市場全体でハイブリッド車の成長が強化されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 生物製剤と細胞・遺伝子治療の物流ブーム

- eコマースによる食料品・ミールキット宅配の拡大

- 新興国におけるグローバルワクチンの取り組み

- 治験小包の分散化需要

- ESG目標に向けた再利用可能なパッシブシッパーの採用

- 保険会社主導のスマート指標の普及

- 市場抑制要因

- ポリマー原料価格の変動

- EUのEPSに対するサーキュラー・エコノミー規制

- 大型荷主の航空貨物輸送能力縮小

- アクティブシステムにおけるリチウム電池の限界

- サプライチェーン分析

- 規制の見通し

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品別

- 断熱容器

- 絶縁シッパー

- 冷媒ジェルパックおよびPCM

- 温度監視装置

- 真空断熱パネル

- ドライアイスシステム

- 包装システム別

- アクティブシステムズ

- パッシブシステムズ

- ハイブリッドシステム

- 素材別

- 発泡ポリスチレン(EPS)

- ポリウレタン(PUR)

- 真空断熱パネル(VIP)

- 発泡ポリプロピレン(EPP)

- バイオベースPCM

- バリアライナー付き段ボール

- 高機能フォーム(フェノール、PIR)

- ユーザビリティ別

- シングルユース

- 再利用可能

- 用途別

- 医薬品・バイオテクノロジー

- 臨床試験と診断

- 乳製品・冷凍デザート

- 食肉・水産物

- その他のアプリケーション

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリアおよびニュージーランド

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Sonoco ThermoSafe

- Cold Chain Technologies

- Pelican BioThermal

- Softbox Systems

- Intelsius(DGP)

- Cryopak

- Sofrigam

- Tempack

- CSafe Global

- Va-Q-Tec

- SkyCell

- CrodaTherm

- Sealed Air Corp.

- DS Smith(International Paper)

- Storopack

- Cascades Inc.

- Cryoport

- Thermo King

- Marken

- Timestrip