医薬品コールドチェーン包装市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Pharmaceutical Cold Chain Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 195 Pages

- 納期

- 2~3営業日

- 商品コード

- 1708214

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

医薬品コールドチェーン包装の世界市場は、2024年に175億米ドルを生み出し、2025年から2034年にかけて15.1%のCAGRで成長すると予測されています。

この成長は主に、mRNAベースの治療、細胞治療、遺伝子治療など、サプライチェーン全体で厳密な温度管理を必要とする先端治療の採用が増加していることが背景にあります。製薬会社がこれらの革新的治療に対する需要の高まりに対応するために生産を拡大するにつれて、信頼性の高いコールドチェーン包装ソリューションの必要性がより重要になります。コールドチェーン包装は、製造現場からエンドユーザーへの輸送中に、生物製剤やワクチンなど温度に敏感な医薬品の安全性、安定性、有効性を保証します。

さらに、慢性疾患の増加や個別化医療の動向の高まりにより、複雑な生物製剤の効能を維持するための特殊な包装ソリューションの必要性が高まっています。保管中や輸送中の温度に敏感な医薬品の品質とコンプライアンスを維持することへの注目の高まりは、市場の拡大にさらに貢献しています。規制当局の監視が強化され、厳格な流通プロトコルを遵守する必要性が高まったことで、メーカーは先進のコールドチェーン包装技術に投資し、製品の安全性とコンプライアンスを確保するようになっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 175億米ドル |

| 予測金額 | 716億米ドル |

| CAGR | 15.1% |

医薬品コールドチェーン包装市場は材料別に区分され、プラスチック、金属、紙が主なカテゴリーです。プラスチックセグメントは2024年に135億米ドルを生み出しました。プラスチックの優位性は、輸送中に必要な温度を維持するために不可欠な優れた断熱性に起因します。軽量で費用対効果に優れているため、製品の完全性を保ちながら輸送コストの削減を目指す製薬企業にとって理想的な選択肢となっています。耐久性と拡張性で知られるプラスチック素材は、生物製剤やその他のデリケートな医薬品を安全に輸送するための実用的なソリューションを提供します。生物製剤の需要が増加するにつれて、サプライチェーン全体で正確な温度管理を維持できるプラスチック包装のニーズが高まり、市場における同セグメントの地位が強化されると予想されます。

市場はさらに、物流・流通センター、バイオ医薬品企業、病院、臨床研究機関、研究機関、その他などエンドユーザー別に分類されます。バイオ製薬会社は2024年に63億米ドルを生み出し、このセグメントの急速な拡大を反映しています。遺伝子治療やmRNA治療の採用が増加しているため、繊細な医薬品の安定性と有効性を維持できる特殊な包装ソリューションの需要が高まっています。厳格な規制ガイドラインは、流通プロセス全体を通じて安全基準の遵守を保証する先進コールドチェーン・パッケージング・ソリューションの必要性を推進する上で重要な役割を果たしています。バイオ医薬品企業が生産能力を拡大するにつれて、信頼性が高く高品質なコールドチェーン包装への需要が高まり、市場の上昇基調が強まると予想されます。

北米の医薬品コールドチェーン包装市場は、2024年には34.4%のシェアを占めています。同地域の市場プレゼンスが高いのは、保管・輸送時に厳格な温度管理が必要な生物製剤や細胞治療薬の需要が伸びていることが主因です。FDAをはじめとする規制当局は、医薬品がサプライチェーン全体を通じて安全性、有効性、コンプライアンスを維持できるよう、コールドチェーン・パッケージング・ソリューションの採用を推進する厳格なガイドラインを実施しています。北米では精密医療がますます重視され、生物製剤のポートフォリオが拡大していることが、世界の医薬品コールドチェーン包装市場における同地域の優位性に寄与しています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 生物製剤と特殊医薬品に対する需要の高まり

- mRNAおよび細胞・遺伝子治療の拡大

- 厳しい規制要件

- eコマースとオンライン薬局の成長

- 製薬業界の拡大

- 業界の潜在的リスク&課題

- コールドチェーンインフラの高コスト

- 温度異常と製品腐敗のリスク

- 促進要因

- 成長可能性分析

- 規制状況

- 技術情勢

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:素材別、2021年~2034年

- 主要動向

- プラスチック

- ポリエチレン(PE)

- ポリプロピレン(PP)

- ポリエチレンテレフタレート(PET)

- ポリウレタン(PU)

- その他

- 金属

- 紙

第6章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- アクティブ

- パッシブ

第7章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 断熱ボックス

- 容器

- 保冷剤

- パレット

- その他

第8章 市場推計・予測:最終用途産業別、2021年~2034年

- 主要動向

- バイオ医薬品企業

- 臨床研究機関

- 病院

- 研究機関

- 物流・流通企業

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Chill-Pak

- Cold Chain Technologies

- CoolPac

- Cryopak

- CSafe

- Envirotainer

- Haier Biomedical

- Insulated Products Corporation

- Intelsius

- Nordic Cold Chain Solutions

- Sealed Air

- Smurfit Kappa

- Sofrigam Group

- Sonoco ThermoSafe

- Tessol

- Va-Q-Tec Thermal Solutions

- Vericool

目次

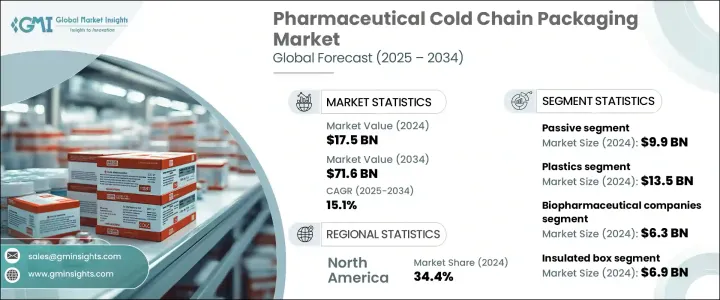

The Global Pharmaceutical Cold Chain Packaging Market generated USD 17.5 billion in 2024 and is projected to grow at a CAGR of 15.1% between 2025 and 2034. This growth is primarily driven by the increasing adoption of advanced therapies, such as mRNA-based treatments, cell therapies, and gene therapies, which require strict temperature control throughout the supply chain. As pharmaceutical companies ramp up production to meet the rising demand for these innovative treatments, the need for reliable cold chain packaging solutions becomes more critical. Cold chain packaging ensures the safety, stability, and efficacy of temperature-sensitive drugs, including biologics and vaccines, during transportation from manufacturing sites to end users.

Additionally, the rise in chronic diseases and the growing trend of personalized medicine have heightened the need for specialized packaging solutions to maintain the potency of complex biologics. The growing focus on maintaining the quality and compliance of temperature-sensitive pharmaceutical products during storage and transit further contributes to the market's expansion. Increased regulatory scrutiny and the need to adhere to strict distribution protocols push manufacturers to invest in advanced cold chain packaging technologies, ensuring product safety and compliance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $17.5 Billion |

| Forecast Value | $71.6 Billion |

| CAGR | 15.1% |

The pharmaceutical cold chain packaging market is segmented by material, with plastic, metal, and paper being the primary categories. The plastic segment generated USD 13.5 billion in 2024. Plastic's dominance can be attributed to its superior thermal insulation properties, which are essential for maintaining the required temperatures during transit. Its lightweight nature and cost-effectiveness make it an ideal choice for pharmaceutical companies aiming to reduce shipping costs while preserving product integrity. Plastic materials, known for their durability and scalability, provide a practical solution for ensuring the safe transportation of biologics and other sensitive drugs. As the demand for biologics increases, the need for plastic packaging that can maintain precise temperature control throughout the supply chain is expected to grow, strengthening the segment's position in the market.

The market is further categorized by end users, including logistics and distribution centers, biopharmaceutical companies, hospitals, clinical research organizations, research institutes, and others. Biopharmaceutical companies generated USD 6.3 billion in 2024, reflecting the rapid expansion of this segment. The growing adoption of gene and mRNA therapies has fueled the demand for specialized packaging solutions capable of preserving the stability and efficacy of sensitive pharmaceuticals. Strict regulatory guidelines play a crucial role in driving the need for advanced cold chain packaging solutions that ensure compliance with safety standards throughout the distribution process. As biopharmaceutical companies expand their production capabilities, the demand for reliable and high-quality cold chain packaging is expected to rise, reinforcing the market's upward trajectory.

North America's pharmaceutical cold chain packaging market held a 34.4% share in 2024. The region's strong market presence is largely attributed to the growing demand for biologics and cell therapies, which require stringent temperature management during storage and transportation. Regulatory authorities, including the FDA, enforce strict guidelines that drive the adoption of cold chain packaging solutions, ensuring that pharmaceutical products maintain their safety, efficacy, and compliance throughout the supply chain. The increasing emphasis on precision medicine and the expanding portfolio of biologics in North America contribute to the region's stronghold in the global pharmaceutical cold chain packaging market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for biologics & specialty drugs

- 3.2.1.2 Expansion of mRNA & cell/gene therapies

- 3.2.1.3 Stringent regulatory requirement

- 3.2.1.4 Growth of e-commerce and online pharmacies

- 3.2.1.5 Expansion of the pharmaceutical industry

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs of cold chain infrastructure

- 3.2.2.2 Risk of temperature excursions & product spoilage

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 - 2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Plastics

- 5.2.1 Polyethylene (PE)

- 5.2.2 Polypropylene (PP)

- 5.2.3 Polyethylene Terephthalate (PET)

- 5.2.4 Polyurethane (PU)

- 5.2.5 Others

- 5.3 Metal

- 5.4 Paper

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Active

- 6.3 Passive

Chapter 7 Market Estimates and Forecast, By Product, 2021 - 2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Insulated box

- 7.3 Containers

- 7.4 Coolants

- 7.5 Pallets

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 Biopharmaceutical companies

- 8.3 Clinical research organizations

- 8.4 Hospitals

- 8.5 Research institutes

- 8.6 Logistics and distribution companies

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Chill-Pak

- 10.2 Cold Chain Technologies

- 10.3 CoolPac

- 10.4 Cryopak

- 10.5 CSafe

- 10.6 Envirotainer

- 10.7 Haier Biomedical

- 10.8 Insulated Products Corporation

- 10.9 Intelsius

- 10.10 Nordic Cold Chain Solutions

- 10.11 Sealed Air

- 10.12 Smurfit Kappa

- 10.13 Sofrigam Group

- 10.14 Sonoco ThermoSafe

- 10.15 Tessol

- 10.16 Va-Q-Tec Thermal Solutions

- 10.17 Vericool

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 195 Pages

- 納期

- 2~3営業日