|

市場調査レポート

商品コード

1851103

電気通信におけるAPI:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Telecom API - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 電気通信におけるAPI:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月30日

発行: Mordor Intelligence

ページ情報: 英文 207 Pages

納期: 2~3営業日

|

概要

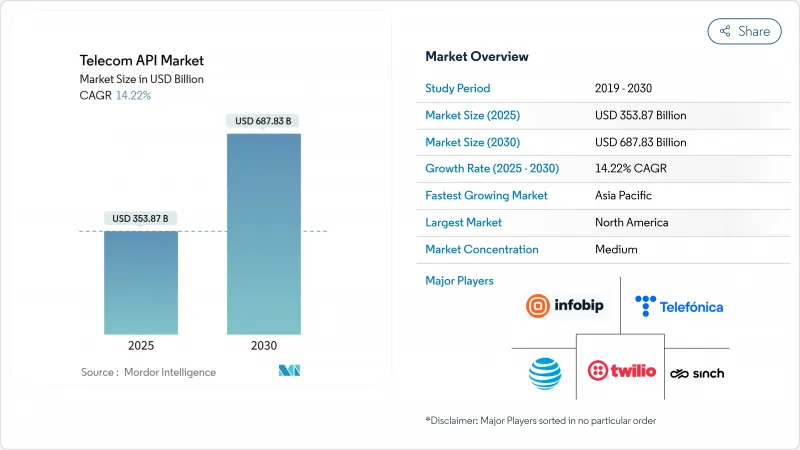

電気通信におけるAPI市場規模は、2025年に3,538億7,000万米ドルと推計され、2030年には6,878億3,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは14.22%です。

通信セクターのプログラマブル・ネットワークへの移行、5G機能の収益化、CPaaS(Communications Platform as a Service)の急速な普及を反映しています。GSMA Open Gatewayのような標準化の取り組み、5GネットワークスライシングのためのクオリティオンデマンドAPIの普及、組み込みリアルタイム通信に対する企業の需要などが成長の主な要因となっています。競合の激化は統合を促しています。機器ベンダーと通信事業者はネットワークAPIをプールするために合弁会社を設立し、CPaaSのスペシャリストは企業買収戦略を通じて規模を拡大しています。また、クラウドの俊敏性とデータの主権要件とのバランスをとるハイブリッドクラウドの展開も市場の恩恵をもたらし、事業者はネットワーク機能を開発者エコシステムに迅速に公開できるようになりました。

世界の電気通信におけるAPI市場の動向と洞察

企業におけるCPaaS導入の急増

Twilioの2025年第1四半期の売上高が11億7,000万米ドル、アクティブ顧客数が33万5,000を超えたことが示すように、企業はオムニチャネルコミュニケーションを顧客のワークフローに組み込み続けています。通信事業者も社内の効率を向上させている:AT&TのMuleSoftを中心としたプログラムは、オンボーディングのサイクルを1年から6週間に短縮し、年間200万時間の作業時間を節約しました。APIの再利用による経済的な見返りは、開発者のエクスペリエンスと継続的な統合パイプラインに対する経営陣のフォーカスを強化します。ジェネレーティブAIを活用したコーディングアシスタントは社内チームの参入障壁を下げ、パーソナライズされたメッセージングはSMS、RCS、音声チャネルでの持続的なトラフィックを促進します。

Open GatewayとCAMARAによるネットワークAPIの標準化

現在、49の事業者グループがGSMA Open Gatewayを支持しており、デバイス検証、遅延制御、位置情報サービスなどの機能の統一インターフェースに関する業界のコンセンサスを示しています。Telefonicaの商用化により、開発者はプライバシー管理を維持しながら、フィンテックやストリーミング・アプリに通信機能を統合することができます。T-MobileのCAMARA準拠のQuality-on-Demand APIは、ヘルスケア、ロジスティクス、リテールにおける低遅延導入を可能にします。標準化により、ソフトウェア企業の統合コストが削減され、ネットワーク対応アプリケーションの市場投入までの時間が短縮されます。

深刻化するAPIセキュリティ侵害と不正シグナリング

APIコール量は2024年に167%急増し、プラットフォームが攻撃ベクトルにさらされた結果、Dell、GitHub、TracFoneで侵害が発生し、後者は1,600万米ドルの違約金を支払いました。調査によると、組織の95%がAPIセキュリティ・インシデントに直面し、23%がデータ損失を被りました。加入者のIDやシグナリングシステムは複数のドメインを横断するため、電気通信事業者は依然として高い標的となっています。効果的な緩和策としては、ゼロトラストポリシー、継続的なランタイム保護、通信事業者とクラウドプロバイダー間での脅威インテリジェンスの共有などがあります。

セグメント分析

メッセージングAPIは2024年に35.67%の電気通信におけるAPI市場シェアを維持し、2兆2,000億メッセージに達した企業向けA2Pトラフィックがその中心となっています。メッセージングの電気通信におけるAPI市場規模は、企業が認証やプロモーションのためにSMS、MMS、リッチコミュニケーションサービスを優先するにつれて着実に拡大すると予測されます。RCSの成長には目を見張るものがある:Infobip社は、A2P RCSの売上が2029年までに42億米ドルに達すると予測しています。一方、決済APIはCAGR 17.45%で最も急速に拡大しています。これは、組み込み型金融モデルが通信事業者のリーチとフィンテック機能を融合させているためです。音声、IVR、WebRTC APIは、企業がマルチモーダルサポートをカスタマーエクスペリエンス・プラットフォームに統合しているため、関連性を維持しています。開発者はまた、加入者識別APIや不正検出APIを活用して、モバイルトランザクションのセキュリティを高めています。

需要パターンは付加価値機能へとシフトし続けています。ジェネレーティブAIチャットボットはコンテクスチュアル・メッセージングを推進し、位置情報ベースのAPIはスマートシティ展開におけるハイパーローカル・マーケティングを可能にします。スパムに対する規制が強化される中、事業者は認証済みの送信者IDにプレミアムを課し、収益の多様化を強化しています。クラウドコンタクトセンターベンダーとの緊密な連携により、メッセージングAPIはヘルスケア、銀行、小売など、企業の変革課題の中心的存在となっています。

ハイブリッド環境は、2024年に49.85%の市場シェアを獲得し、CAGR 15.45%と最も高い成長軌道を達成。ハイブリッド展開の電気通信におけるAPI市場規模は、ネットワークコアがオンプレミスに留まる一方で、課金、分析、暴露レイヤーのマイクロサービスがパブリッククラウドに移行することで拡大すると予測されています。事業者の例としては、VIVA Bahrainのハイブリッドクラウドコアや、PCCW GlobalのホールセールAPI向けマルチクラウド戦略が挙げられます。APACでは、ローカル・データ・ストレージに対する規制が義務付けられており、ハイブリッドの導入がさらに進んでいます。

事業者は、ベンダーのロックインを回避し、コスト最適化のためにワークロードを動的にシフトするために、クラウドにとらわれないコンテナオーケストレーションを支持しています。エッジノードはハイブリッドトポロジを拡張し、AI推論やコンピュータビジョンタスクにミリ秒単位のレイテンシを提供します。純粋なパブリッククラウドモデルは、グリーンフィールドのMVNOには依然として適しているが、統合の複雑さと予測不可能なイグレス料金は、ティアワン事業者の幅広い採用を制限しています。オンプレミスのみの戦略は、セキュリティが重視される政府機関のネットワークには適しているが、大規模なAPIエコノミーに必要な弾力性に欠ける。

電気通信におけるAPI市場レポートは、サービスタイプ別(メッセージング/SMS-MMS-RCS API、音声/IVR &音声コントロールAPI、その他)、展開タイプ別(ハイブリッド、マルチクラウド、その他展開モード)、エンドユーザー別(企業デベロッパー、社内通信デベロッパー、パートナーデベロッパー、ロングテールデベロッパー)、ビジネスモデル別(キャリアへの直接接続、アグリゲータ主導のCPaaS、Platform-As-A-Service[PaaS]、その他)、地域別に分類されています。

地域分析

北米は2024年の売上高の34.06%を占め、CPaaSの高い普及率と広範な5Gカバレッジを反映しています。AT&T、T-Mobile、VerizonのAdunaベンチャーとの協業により、フィンテックやヘルスケア・アプリケーションのセキュリティを高める番号認証とSIMスワップAPIへの統一アクセスが可能になりました。Twilioの2024年の売上高は44億6,000万米ドルで、プログラマブル通信に対する企業の投資が堅調であることを裏付けています。テクノロジー・サンドボックスを奨励する政府の枠組みは、電気通信におけるAPI市場における継続的な実験をサポートしています。

アジア太平洋地域は、モバイル・ファーストの経済が5Gの導入とデジタル・サービスの普及を促進し、2030年までのCAGRが最速の17.51%になると予測されています。2024年第2四半期の地域通信事業者の合計売上高は1,477億米ドルに達し、72%の事業者がプラス成長を報告しています。2028年までに5G加入率が88%に達すると予測される中国と、クオリティ・オンデマンドAPIを公開するオーストラリア、日本、韓国の取り組みは、積極的な拡大を示しています。スマート・マニュファクチャリングと電子政府に対する政府の指令は、低遅延とセキュリティ機能に対する需要を高め、電気通信におけるAPI市場を地域のデジタル・アジェンダのバックボーンにしています。

欧州では、GDPRに沿ったセキュリティ対策がAPIサービスに対する顧客の信頼を高めているため、着実な成長を示しています。ドイツテレコムのAIフォンのロードマップは、デバイス、AI、通信機能の融合に対する地域の通信事業者の関心を示しています。欧州の通信事業者とハイパースケーラー間の共同プロジェクトは、エッジの展開とCAMARA APIの標準化を加速させる。中東・アフリカ、ラテンアメリカの新興市場も、ネットワーク近代化投資とクラウドパートナーシップ戦略に支えられ、デジタルサービス開始までの市場投入期間を短縮し、同様の軌道をたどっています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 企業におけるCPaaS導入の急増

- オープンゲートウェイとCAMARAによるネットワークAPIの標準化

- QoSオンデマンドAPIを推進する5Gの収益化圧力

- エッジコンピューティングのワークロードは低レイテンシのスライシングAPIを必要とする

- IDおよび課金APIを必要とするIoTフリートの拡大

- 参入障壁を下げるGen-AI支援開発ツール

- 市場抑制要因

- 深刻化するAPIセキュリティ侵害とシグナリング詐欺

- レガシーOSS/BSSアップグレードのボトルネック

- OTT CPaaS競合によるマージン圧縮

- ハイパースケーラーとの不透明な収益分配モデル

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- マクロ経済影響分析

- 電気通信業界におけるAPIの使用事例

第5章 市場規模と成長予測

- サービスタイプ別

- メッセージング/SMS-MMS-RCS API

- 音声/IVRおよび音声コントロールAPI

- 決済API

- WebRTC API

- ロケーション&マッピングAPI

- 加入者ID管理およびSSO API

- その他のサービス

- 展開タイプ別

- ハイブリッド

- マルチクラウド

- その他の展開モード

- エンドユーザー別

- エンタープライズデベロッパー

- 社内通信開発者

- パートナー開発者

- ロングテール開発者

- ビジネスモデル別

- 通信事業者への直接接続

- アグリゲータ主導型CPaaS

- プラットフォーム・アズ・ア・サービス(PaaS)

- APIマーケットプレース/エクスチェンジ

- 地域別

- 北米

- 南米

- 欧州

- アジア太平洋地域

- 中東・アフリカ

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- ベンダー能力マトリックス

- 主要ベンダーの主要事例

- 企業プロファイル

- ATandT Inc.

- Telefonica SA

- Twilio Inc.

- Infobip Ltd.

- Sinch AB

- Verizon Communications Inc.

- Orange SA

- Deutsche Telekom AG

- Ribbon Communications

- Huawei Technologies Co. Ltd.

- Telefonaktiebolaget LM Ericsson

- Cisco Systems Inc.

- Google LLC(Apigee)

- Vodafone Group Plc

- Nokia Corp.

- Vonage Holdings Corp.

- MessageBird B.V.

- Bandwidth Inc.

- Telnyx LLC

- Syniverse Technologies LLC