|

|

市場調査レポート

商品コード

1687902

世界の滅菌装置-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Global Sterilization Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界の滅菌装置-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 114 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

世界の滅菌装置市場規模は2025年に96億米ドルと推定され、予測期間(2025~2030年)のCAGRは7.37%で、2030年には137億米ドルに達すると予測されます。

COVID-19パンデミックは医療の優先順位を変え、医療管理に悪影響を与えました。パンデミックの初期には、いくつかの国が封鎖状態にありました。他国との貿易を停止し、渡航制限を実施したため、2020年前半には治療、診断、外科手術などの医療サービスが低下しました。COVID-19の臨床管理では、院内感染を防ぐことが重要です。2021年8月に発表された「英国の最初のCOVID-19パンデミックの波における院内SARS-CoV-2感染」と題する研究によると、英国の314の病院でCOVID-19に感染した患者の11.3%が入院後に感染しました。この割合は2020年5月には15.8%に増加しました。このように、この流行は医療施設の院内感染管理能力に影響を与え、滅菌器の需要を大幅に増加させました。COVID-19症例の増加により、政府関連団体もCOVID-19の影響を軽減するために取り組んでいます。例えば、米国食品医薬品局(USFDA)による2020年3月の更新、産業と食品医薬品局スタッフ向けガイダンスによると、滅菌または消毒された医療装置の迅速な回転を促進し、COVID-19パンデミック時の公衆衛生上の緊急事態のために患者や医療従事者がSARS-CoV-2にウイルス曝露するリスクを低減するのに役立つ滅菌器、消毒装置、空気清浄機の供給を維持することが適切であるとしています。USFDAは、この公衆衛生上の緊急事態において、滅菌器、消毒器、空気清浄機の利用可能性を高めることで、このような緊急の公衆衛生上の懸念に対処することができると考えています。

世界人口の増加に伴い、様々な感染症の流行が急速に増加しています。これらの病気の多くは、医療介入や手術を必要とします。手術に使用される器具や装置は滅菌する必要があります。さらに、感染した器具が病気の相互感染を引き起こす可能性もあります。米国形成外科学会による「全米形成外科統計2020」によると、2020年には米国で2314720件の美容外科手術が行われ、2019年には267万8302件の手術が行われました。さらに、2020年と2019年に行われた再建手術の総数は、それぞれ687万8,486件と665万2,591件でした。これらの手術には滅菌された器具が必要であるため、市場は今後数年間で大きな成長が見込まれます。

これらの要因により、感染症のさらなる蔓延を防ぐための滅菌装置のニーズが高まっています。製薬会社の進出も市場成長の大きな要因となっています。しかし、これらの装置の承認や製造に関する厳しい規制基準や、一部の装置に化学滅菌剤として使用されている薬剤が目や皮膚に潜在的な損傷を与える可能性があるという欠点が、市場の成長を抑制しています。

滅菌装置市場の動向

高温滅菌装置が市場を独占

高温装置は最も広く使用されており、最も信頼できる滅菌装置です。高温滅菌は通常、患者、スタッフ、環境に対して無害であり、高い殺微生物効果があります。また、医療装置の奥深くまで浸透し、他の滅菌装置に比べてコストが低いため、費用対効果も高いです。これらの要因が、市場におけるこのセグメントの優位性の要因となっています。高温滅菌装置はさらに蒸気滅菌と乾式滅菌に細分化されます。

いくつかの外科手術の増加は、その過程で使用される外科用装置の高温滅菌を後押ししており、このセグメントの成長を促進する可能性があります。American Joint Replacement RegistryのAnnual Report 2020によると、米国では2012~2019年の間に189万7,050件の一次と再置換の股関節と膝関節形成術が実施されました。また、米国では2012~2019年にかけて、約99万5,410件の人工膝関節全置換術と62万5,097件の人工股関節全置換術が行われました。

米国代謝・肥満外科学会統計によると、米国だけで2019年に約25万6,000件、2018年に約25万2,000件の手術が行われました。これらの統計は、肥満手術件数の増加を示しており、市場全体の成長を牽引しています。

さらに、このセグメントにおける新製品の発売が市場の成長を促進する可能性があります。例えば、2020年5月、EscoはEsco CelCulture CO2 Incubator with High Heat Sterilization(CCL-HHS)を発売しました。これは、作業スペースを汚染する可能性のある耐性真菌、細菌胞子、植物細胞を死滅させるのに効果的であることが証明されています。従って、このような要因が予測期間中の同セグメントの成長を後押しすると予想されます。

北米が最速の成長を遂げる

北米は滅菌装置市場においてプラスの成長を遂げており、予測期間中も大幅な成長が見込まれます。二次汚染や院内感染リスクの増加、手術件数の増加、大手市場参入企業の存在、研究開発手順の増加が、同地域の市場を牽引すると予測されます。米国は北米市場を独占すると予想されています。

米国疾病予防管理センターが発表した「2020 HAI Progress Reportエグゼクティブサマリー」レポートによると、米国の患者の約31人に1人が少なくとも1件の院内感染に罹患しており、同国の医療施設における患者ケアの実践を改善する必要性が浮き彫りになっています。このように、同国では院内感染によって、病院のカーテンを適時に交換するなど、適切な衛生維持と滅菌の必要性が高まっています。

また、高齢者層は手術を受けやすく、免疫力が低下しているため感染症のリスクが高いです。World Ageing Report 2019によると、同国の高齢者は2019年の5,334万人から2050年には8,381万3,000人に増加する見込みであるため、感染症の発生率が高まり、市場の成長に寄与します。

また、このセグメントにおける技術の進歩も市場を牽引しています。例えば、2020年9月、Midmark Corporationは新しい滅菌器データロガーと更新されたMidmark M3 Steam Sterilizerを発売し、米国の歯科クリニックにおける器具処理にスピード、簡便性、コンプライアンスをもたらしました。

したがって、医療装置やその他の器具の需要が急増し、滅菌装置の需要が増加しています。

滅菌装置産業概要

滅菌装置の大半は世界企業が製造しています。より多くの研究資金と優れた流通システムを持つ市場リーダーが市場での地位を確立しています。主要市場参入企業は、Getinge AB、Fortive Corporation、Anderson Products、Cantel Medical、Steris PLCです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 感染のリスク増加

- 手術件数の増加

- 製薬・バイオテクノロジー産業の成長

- 市場抑制要因

- 装置に関連する高コスト

- 装置内の化学品への暴露

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 装置別

- 高温滅菌

- 湿式/蒸気滅菌

- ドライ滅菌

- 低温滅菌

- 酸化エチレン(ETO)

- 過酸化水素

- オゾン

- その他の低温滅菌装置

- 濾過滅菌

- 電離放射線滅菌

- 電子ビーム滅菌

- ガンマ線滅菌

- その他電離放射線滅菌装置

- 高温滅菌

- エンドユーザー別

- 病院とクリニック

- 製薬・バイオテクノロジー企業

- 教育・研究機関

- 飲食品産業

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Fortive Corporation(Advanced Sterilization Products)

- Anderson Products

- Metall Zug Group(Belimed)

- Cantel Medical

- Getinge AB

- Matachana Group

- MMM Group

- STERIS PLC

- Systec GmbH

- Stryker Corporation(TSO3 INC.)

第7章 市場機会と今後の動向

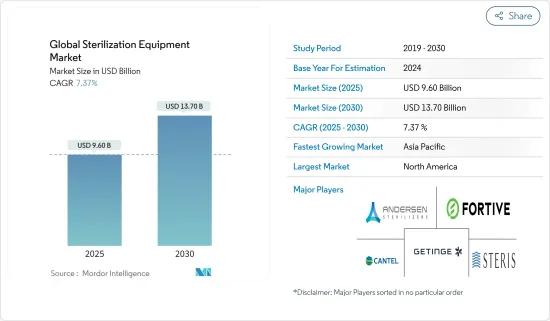

The Global Sterilization Equipment Market size is estimated at USD 9.60 billion in 2025, and is expected to reach USD 13.70 billion by 2030, at a CAGR of 7.37% during the forecast period (2025-2030).

The COVID-19 pandemic has altered healthcare priorities, adversely impacting healthcare management. In the initial days of the pandemic, several countries were in lockdown. They suspended trade with other countries and implemented travel restrictions, leading to a decline in healthcare services such as treatments, diagnosis, and surgical procedures in the first half of 2020. Preventing hospital-acquired infections is a critical aspect of the clinical management of COVID-19, as hospital-acquired infections have been a common feature of such outbreaks. According to the study titled 'Hospital-acquired SARS-CoV-2 infection in the UK's first COVID-19 pandemic wave', published in August 2021, 11.3% of patients with COVID-19 in 314 UK hospitals became infected after hospital admission. This rate increased to 15.8% in May 2020. Thus, the outbreak has impacted the healthcare facilities' ability to manage hospital-acquired infections, significantly increasing the demand for sterilizers. Due to the rising COVID-19 cases, government associations also worked toward reducing the COVID-19 impact. For instance, as per a March 2020 update by the US Food and Drug Administration (USFDA), Guidance for Industry and Food and Drug Administration Staff, it is adequate to maintain the supply of sterilizers, disinfectant devices, and air purifiers that can facilitate the rapid turnaround of sterilized or disinfected medical equipment and help reduce the risk of viral exposure for patients and healthcare providers to SARS-CoV-2 for public health emergency during the COVID-19 pandemic. The USFDA believes that the policy outlined will help address these urgent public health concerns by increasing the availability of sterilizers, disinfectant devices, and air purifiers during this public health emergency.

With the growing global population, the prevalence of various infectious diseases has rapidly increased. Many of these diseases require medical interventions and surgeries. The instruments and devices used in the surgeries need to be sterilized. Moreover, the infected instruments may give rise to the cross-transmission of diseases. According to the National Plastic Surgery Statistics 2020 by the American Society of Plastic Surgeons, 2,314720 cosmetic surgical procedures were performed in the United States in 2020, and 2,678,302 surgeries were performed in 2019. Additionally, the total number of reconstructive procedures performed in 2020 and 2019 were 6,878,486 and 6,652,591, respectively, in the United States. As these surgeries require sterilized instruments, the market is expected to witness significant growth in the coming years.

These factors have given rise to the need for sterilization equipment to prevent the further spread of infectious diseases. The expansion of pharmaceutical companies has also been a major factor in the market's growth. However, stringent regulatory standards for approval, production of these devices, and disadvantages of chemical agents used as chemical sterilants in some equipment, which may cause potential damage to the eyes and skin, have been restraining the market's growth.

Sterilization Equipment Market Trends

High-temperature Sterilization Equipment Dominates the Market

High-temperature equipment is the most widely used and the most dependable sterilization equipment. High-temperature sterilization is usually nontoxic to patients, staff, and the environment and is highly microbicidal. It also penetrates deep into the medical devices and is less costly than other sterilization equipment, thus making it cost-effective. These factors are responsible for the dominance of this segment in the market. High-temperature sterilization equipment is further sub-segmented into steam sterilization and dry sterilization.

The increasing number of several surgical procedures is boosting the high-temperature sterilization of surgical devices used in the process, which may drive the segment's growth. As per the American Joint Replacement Registry's Annual Report 2020, 1,897,050 primary and revision hip and knee arthroplasty procedures were performed between 2012 and 2019 in the United States. About 995,410 total knee arthroplasty and 625,097 total hip arthroplasty were also performed from 2012 to 2019 in the United States.

According to the American Society for Metabolic and Bariatric Surgery Statistics, around 256,000 surgeries and 252,000 surgeries were performed in 2019 and 2018, respectively, in the United States alone. These statistics show an increase in the number of bariatric surgeries, which is driving the growth of the overall market.

Moreover, the launch of new products in the segment may drive the market's growth. For instance, in May 2020, Esco launched Esco CelCulture CO2 Incubator with High Heat Sterilization (CCL-HHS). It has proven effective in killing resistant fungi, bacterial spore, and vegetative cells that may contaminate the workspace. Thus, such factors are expected to boost the segment's growth during the forecast period.

North America to Witness the Fastest Growth

North America experienced positive growth in the sterilization equipment market, and it is estimated to witness significant growth over the forecast period. The increasing risk of cross-contamination and hospital-acquired infections, rising number of surgeries, the presence of major market players, and growth in R&D procedures are expected to drive the market in the region. The United States is expected to dominate the North American market.

According to the '2020 HAI Progress Report Executive Summary' report published by the Centers for Disease Control and Prevention, approximately one in 31 US patients contract at least one hospital-acquired infection, highlighting the need for improvements in patient care practices in the country's healthcare facilities. Thus, hospital-acquired infections in the country are driving the need for proper hygiene maintenance and sterilization, including timely changing of hospital curtains.

In addition, the elderly population is prone to surgeries and is at higher risk of infections due to a weakened immune system. According to the World Ageing Report 2019, the country's elderly population is expected to increase from 53.340 million in 2019 to 83.813 million in 2050, thus increasing the incidence of infectious diseases and contributing to the market's growth.

The technological advancements in the field are also driving the market. For instance, in September 2020, Midmark Corporation launched the new Sterilizer Data Logger and the updated Midmark M3 Steam Sterilizer, bringing speed, simplicity, and compliance to instrument processing in dental practices in the United States.

Hence, there has been a surge in demand for medical devices and other instruments, increasing the demand for sterilization equipment.

Sterilization Equipment Industry Overview

The majority of sterilization equipment is being manufactured by global players. Market leaders with more funds for research and a better distribution system established their positions in the market. Major market players are Getinge AB, Fortive Corporation, Anderson Products, Cantel Medical, and Steris PLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Risks of Cross-transmission

- 4.2.2 Increasing Number of Surgical Procedures

- 4.2.3 Growth in Pharmaceutical and Biotechnology Industries

- 4.3 Market Restraints

- 4.3.1 High Cost Associated with the Device

- 4.3.2 Exposure to Chemicals in Equipments

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Equipment

- 5.1.1 High-temperature Sterilization

- 5.1.1.1 Wet/Steam Sterilization

- 5.1.1.2 Dry Sterilization

- 5.1.2 Low-temperature Sterilization

- 5.1.2.1 Ethylene Oxide (ETO)

- 5.1.2.2 Hydrogen Peroxide

- 5.1.2.3 Ozone

- 5.1.2.4 Other Low-temperature Sterilization Equipment

- 5.1.3 Filtration Sterilization

- 5.1.4 Ionizing Radiation Sterilization

- 5.1.4.1 E-beam Radiation Sterilization

- 5.1.4.2 Gamma Sterilization

- 5.1.4.3 Other Ionizing Radiation Sterilization Equipment

- 5.1.1 High-temperature Sterilization

- 5.2 By End User

- 5.2.1 Hospitals and Clinics

- 5.2.2 Pharmaceutical and Biotechnology Companies

- 5.2.3 Education and Research Institutes

- 5.2.4 Food and Beverage Industries

- 5.2.5 Other End Users

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Fortive Corporation (Advanced Sterilization Products)

- 6.1.2 Anderson Products

- 6.1.3 Metall Zug Group (Belimed)

- 6.1.4 Cantel Medical

- 6.1.5 Getinge AB

- 6.1.6 Matachana Group

- 6.1.7 MMM Group

- 6.1.8 STERIS PLC

- 6.1.9 Systec GmbH

- 6.1.10 Stryker Corporation (TSO3 INC.)