|

市場調査レポート

商品コード

1642112

FWaaS(Firewall-as-a-Service):市場シェア分析、業界動向・統計、成長予測(2025年~2030年)Firewall-as-a-Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| FWaaS(Firewall-as-a-Service):市場シェア分析、業界動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

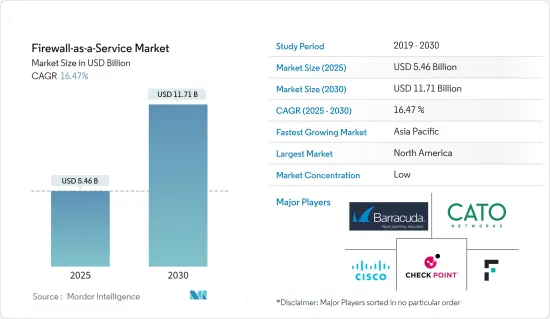

FWaaS(Firewall-as-a-Service)市場規模は、2025年に54億6,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは16.47%で、2030年には117億1,000万米ドルに達すると予測されます。

クラウドベースのファイアウォール・サービスは、柔軟な拡張性、セキュアなアクセス・パリティ、マイグレーションを超えるセキュリティ、アイデンティティ保護、セキュアなパフォーマンス管理など、いくつかのメリットを組織に提供します。その結果、多くの企業がクラウドネットワークのデータパケットを管理するためにFWaaS(Firewall-as-a-Service)を導入しています。

主なハイライト

- ハードウェアベースのセキュリティ・オプションは一般的ではなくなりつつあり、クラウドの普及により、サービス提供パラダイムを使用するソフトウェアベースのソリューションの導入が増加しています。過去5年間で、このような変化がFWaaSソリューションやその他のネットワーク・セキュリティ・サービスの普及を加速させ、よりスケーラブルで使いやすいセキュリティ・ソリューションをもたらしました。

- クラウドベースのアプリケーションの急成長、パブリッククラウド環境におけるデータ漏洩の急増、ビジネス組織のファイアウォールプロトコルの絶え間ない変化が、世界市場におけるFWaaS(Firewall-as-a-Service)の成長に影響を与える主な要因となっています。しかし、ホスト型ファイアウォールとオンプレミス型ファイアウォールの統合の複雑さや、低開発国における不十分なITインフラが、市場の成長を阻害しています。

- FWaaS(Firewall-as-a-Service)は、BFSI、政府、IT・通信、ヘルスケア、小売、製造、航空宇宙・防衛、エネルギー・公益事業など、さまざまな業界で利用されており、企業向けにクラウドベースの高度なネットワーク・セキュリティ・ソリューションを提供しています。クラウド・ネットワーク上のトラフィックが飛躍的に増加する中、企業はそれぞれのクラウド・ネットワーク上のデータを保護するために、ファイアウォールやエンドポイント・セキュリティなどのセキュリティ・ソリューションを採用しています。

- COVID-19の影響により、在宅勤務やクラウドの導入が増加しました。IT従業員のToDoリストの大半は、リモートアクセスの提供が占めるようになると思われます。Global Workplace Analyticsによると、年末までに労働人口の最大30%が週に何日も在宅勤務をするようになる可能性があるといいます。Cybersecurity Insidersの調査では、回答者の半数以上(54%)が、COVID-19によってワークフローやアプリへのクラウド導入が増加したと回答しています。さらに、回答者の約66%は、リモートワーカーに対するセキュリティ脅威の増加を予測しています。ユーザーがどこで作業していても、ファイアウォールは組織のネットワークを保護する必要があります。

FWaaS(Firewall-as-a-Service)市場動向

パブリッククラウドの導入モデルが大きな市場シェアを占める見込み

- クラウド環境への移行が進む中、データ保護やセキュリティ侵害は、金融、政府機関、ヘルスケア、小売、防衛、IT・通信など、さまざまな業界で大きな問題となっています。

- RedLock Inc.のレポートによると、全世界のデータベースの約半数(49%)が暗号化されておらず、潜在的なサイバー攻撃に対して脆弱な状態になっています。さらに、半数以上(51%)の組織がクラウドストレージサービスを利用しており、ホスト環境で実行されているアプリケーションに対する攻撃のリスクが高まっています。

- さらに、従来のITインフラからクラウド環境への移行に伴い、エンドポイントが急速に増加しているため、クラウドプラットフォームに特化した高度なファイアウォール保護サービスが必要となっています。

- 市場のベンダーは、アプリケーションの円滑な処理を保証するために、SSLオフロード、コンテンツ・キャッシング、ロード・バランシングを備えたFWaaS(Firewall-as-a-Service)ソリューションの強化バージョンを提供することで、この需要に応えています。世界の新興諸国では、クラウド環境を保護し、ビジネス機能全体を向上させるために必要なサービスとしてFWaaSを採用しています。

- 2023年4月、アカマイ・テクノロジーズ・インクはProlexic Network Cloud Firewallを発表しました。Akamai Prolexicのこの機能により、お客様は独自のアクセス制御リスト(ACL)を管理および定義できるようになり、独自のネットワークエッジをより柔軟に保護できるようになります。ProlexicはアカマイのクラウドベースのDDoSプロテクション・プラットフォームで、攻撃がアプリケーションやデータセンター、インターネットに面したインフラに到達する前に阻止します。

アジア太平洋地域が市場の大幅な成長に期待

- アジア太平洋地域では現在、FWaaS(Firewall-as-a-Service)の導入が最も急速に進んでおり、大企業から中小企業までがこのテクノロジーを採用しています。中国はサイバー攻撃の増加を目の当たりにしており、これが防衛能力の向上を促しています。しかし、同国は世界の他の地域でサイバー攻撃の重要な発信源となる可能性も十分にあります。さらに、中国では技術の進歩により、接続された機器の数が増加しています。デバイスの相互接続性も、5G対応デバイスによって飛躍的に高まると思われます。その結果、接続されたデバイスが増え、セキュリティ製品に対する市場のニーズが一気に高まる。

- 中国では、組織のデジタル化傾向が強まり、業務の一環として関連技術が使用されるようになった結果、サイバーセキュリティ事件が急増しています。技術の進歩により、中国では接続されたガジェットが増えています。さらに、5G対応ガジェットの使用増加に伴い、デバイスの相互接続性も大幅に増加するため、セキュリティ製品のニーズが直接的に高まり、同地域の市場を大きく牽引することになります。

- サイバーセキュリティに対する日本の企業や政府の関心は急速に高まっています。日本の組織に対するサイバー攻撃の増加により、政府は新たな戦略、法律、施設の設立を促しています。さらに、スマートフォンの普及や、さまざまな電化製品のインターネットへの接続の増加は、生活をより便利なものにしているが、一方で、人々を日常的に情報盗難のリスクにさらしています。

- 日本は、米国国土安全保障省との協定のように、政府が直面するサイバー脅威を抑制するための改善と協力のために、サイバーセキュリティの優先事項を運用するための各国との二国間協力を模索しています。2023年1月、米国と日本は、米国国土安全保障省が述べているように、主に運用面での協力を強化するために、サイバーセキュリティに関する最新の協力覚書に署名しました。

- オーストラリア政府は、2030年までに最もサイバーセキュアな国になるという目標に重点を置いています。これは、サイバー脅威が増大し、サイバーセキュリティ・ソリューションに対する需要が高まっているためであり、そのために同国は永続的かつ適応力のある能力に投資しています。この目標を達成するため、政府はサイバーセキュリティ製品やサービスのブランドとして認知され、国内市場の成長を後押しすることを望んでいます。

FWaaS(Firewall-as-a-Service)業界の概要

FWaaS(Firewall-as-a-Service)市場は、Barracuda Networks, Inc.、Cato Networks、Check Point Software Technologies, Inc.、Cisco Systems, Inc.、Forcepointなどの大手企業が存在し、断片化されています。市場のプレーヤーは、製品ラインナップを強化し、持続可能な競争優位性を獲得するために、パートナーシップや買収などの戦略を採用しています。

- 2023年2月- フォーティネットは、同社のコア製品であるFortiGateファイアウォールのセキュリティ機能とネットワーク機能をより効率的かつ強力に融合させることを約束する新しいASICを発表しました。このカスタムチップは7ナノメートル・パッケージで、第5世代セキュリティ・プロセッシング・システム(FortiSP5)と呼ばれ、FortiGateシステムの性能向上を約束します。

- 2022年10月- オンラインセキュリティのリーダーであるMcAfee Corp.が英国でMcAfee+を発表。この新しい製品ラインには、ユーザーが安心してオンライン生活を送れるようにする、まったく新しいプライバシーとアイデンティティの保護機能が含まれています。米国で最初にデビューした新しいMcAfee+製品スイートは、英国でも利用できるようになり、ユーザーは広範な個人情報クリーンアップサービス、ID回復支援、財布紛失支援、脅威に対する世界クラスの防御ですべてのデバイスを保護する機能を利用できるようになりました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因と市場抑制要因のイントロダクション

- 市場促進要因

- クラウドベースのアプリケーションの急成長

- パブリッククラウド環境におけるデータ漏洩の急増

- 企業組織におけるファイアウォールプロトコルの変化

- 市場抑制要因

- ホスティング型ファイアウォールとオンプレミス型ファイアウォールの統合の複雑さ

- 業界バリューチェーン分析

- 業界の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- サービスモデル別

- SaaS

- IaaS

- PaaS

- 展開モデル別

- プライベート

- パブリック

- ハイブリッド

- ユーザータイプ別

- 大企業

- 中小企業

- 業界別

- BFSI

- IT・通信

- ヘルスケア

- 小売

- 航空宇宙・防衛

- その他業界別

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他欧州

- アジア太平洋

- 中国

- 日本

- オーストラリア

- その他アジア太平洋地域

- ラテンアメリカ

- メキシコ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- 北米

第6章 競合情勢

- 企業プロファイル

- Barracuda Networks, Inc.

- Cato Networks

- Check Point Software Technologies, Inc.

- Cisco Systems, Inc.

- Forcepoint

- Fortinet, Inc.

- IntraSystems

- Juniper Networks, Inc.

- Microsoft Corporation

- Sprout Technologies Ltd

- Vocus Communications

- Zscaler, Inc.

第7章 投資分析

第8章 市場機会と今後の動向

The Firewall-as-a-Service Market size is estimated at USD 5.46 billion in 2025, and is expected to reach USD 11.71 billion by 2030, at a CAGR of 16.47% during the forecast period (2025-2030).

Cloud-based firewall services offer several benefits to organizations, including flexible scalability, secure access parity, security over migration, identity protection, and secure performance management. As a result, many organizations are implementing firewall-as-a-service to manage their data packets in the cloud network.

Key Highlights

- Hardware-based security options are becoming less common, and the implementation of more software-based solutions that use a service delivery paradigm has increased due to widespread cloud adoption. Over the past five years, these changes have accelerated the uptake of FWaaS solutions and other network and security services, bringing about more scalable and user-friendly security solutions.

- The enormous growth in cloud-based applications, the surge in data breaches in the public cloud environment, and ever-changing firewall protocols for business organizations are major factors influencing growth for the firewall-as-a-service in the global market. However, the complexity of integrating hosted firewalls with on-premise firewalls and inadequate IT infrastructures in underdeveloped nations are obstructing market growth.

- Firewall-as-a-service has found a place in various industries such as BFSI, government, IT & telecom, healthcare, retail, manufacturing, aerospace & defense, energy & utilities, and others, offering an advanced cloud-based network security solution for enterprises. As traffic increases exponentially over the cloud network, organizations have adopted security solutions like firewalls and endpoint security to protect their data on their respective cloud network.

- The impact of Covid-19 led to a rise in work-from-home and cloud adoption. The majority of IT employees' to-do lists will be dominated by providing remote access. According to Global Workplace Analytics, up to 30% of the workforce could be working from home multiple days per week by the end of the year. More than half (54%) of a Cybersecurity Insiders survey respondents said Covid-19 increased their cloud adoption for workflows and apps. Furthermore, about 66% of respondents anticipate increased security threats to remote workers. No matter where the users are located while working, firewalls must safeguard the organization's networks.

Firewall as a Service Market Trends

Public Cloud Deployment Model is Expected to Hold Significant Market Share

- As organizations continue to move their operations to cloud environments, data protection, and security breaches have become major concerns across various industries, including financial services, government organizations, healthcare institutions, retail, defense, IT & telecom, and others.

- A report by RedLock Inc. reveals that nearly half (49%) of all databases worldwide are not encrypted, leaving them vulnerable to potential cyber-attacks. Additionally, over half (51%) of organizations are exposed to cloud storage services, increasing the risk of attacks on applications running in hosted environments.

- Furthermore, the shift from traditional IT infrastructure to cloud environments has resulted in a rapid increase in endpoints, necessitating advanced firewall protection services that are specific to cloud platforms.

- Vendors in the market are responding to this demand by offering enhanced versions of firewall-as-a-service (FWaaS) solutions with SSL offloading, content caching, and load balancing to ensure the smooth processing of applications. Developed countries worldwide are adopting FWaaS as a necessary service to protect their cloud environments and improve overall business functions.

- In April 2023, Akamai Technologies, Inc. launched the Prolexic Network Cloud Firewall. This capability of Akamai Prolexic allows customers to manage and define their own access control lists (ACLs) while enabling greater flexibility to secure their own network edge. Prolexic is Akamai's cloud-based DDoS protection platform that stops attacks before they reach applications, data centers, and internet-facing infrastructure.

Asia Pacific Expected to Witness Significant Growth in the Market

- The Asia Pacific region is currently experiencing the fastest adoption of firewall-as-a-service, with both large and small enterprises adopting this technology. China has witnessed an increase in cyberattacks, which has prompted the country to improve its defense capabilities. However, the country also has a good chance of serving as a significant point of origin for cyberattacks in other parts of the globe. Moreover, the number of connected devices has increased in China due to technological advancements. The interconnectivity of the devices will also grow exponentially with 5G-enabled devices. Consequently, there are more connected devices, which immediately increases the market's need for security products.

- Cybersecurity incidents have sharply increased in China as a result of the growing organizational propensity toward digitization and the usage of related technology as part of their operations. Due to technological advancements, there are more connected gadgets in China. Moreover, with the rise in the usage of 5G-enabled gadgets, the interconnectedness of the devices will also significantly increase, which in turn directly increases the need for security products, driving the market significantly within the region.

- Cybersecurity is gaining interest from Japanese enterprises and the government rapidly. The rise in cyberattacks on Japanese organizations prompts the government to establish new strategies, legislation, and facilities. Moreover, the widespread utilization of smartphones and the increasing connection of various electrical appliances to the Internet have made life more convenient but however, had exposed people to the daily risk of information theft.

- Japan is seeking bilateral cooperation with countries to operationalize its cybersecurity priorities, such as the agreement with the U.S. Department of Homeland Security, to improve and collaborate on curbing cyber threats faced by the governments. In January 2023, The United States and Japan signed an updated memorandum of cooperation on cybersecurity mainly to strengthen operational collaboration, as stated by the U.S. Department of Homeland Security.

- The government of Australia is focusing on the goal of becoming the most cyber-secure nation by 2030 as a result of growing cyber threats and demand for cyber security solutions for which the country is investing in enduring and adaptive capabilities. With this aim, the government wants the country to be a recognized brand for cybersecurity products and services, boosting domestic market growth.

Firewall as a Service Industry Overview

The Firewall-as-a-Service market is fragmented with the presence of major players like Barracuda Networks, Inc., Cato Networks, Check Point Software Technologies, Inc., Cisco Systems, Inc., and Forcepoint. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- February 2023 - Fortinet introduced a new ASIC that promises to meld the security and network functions of its core family of FortiGate firewalls more efficiently and powerfully. The custom chip is a 7-nanometer package, called a fifth-generation security processing system or FortiSP5, that promises several performance improvements for the FortiGate system.

- October 2022 - McAfee Corp., a leader in online security, introduced McAfee+ in the UK. This new product line includes all-new privacy and identity protections that let users live their lives online with confidence and security. The new McAfee+ product suite, which first debuted in the US, is now accessible in the UK and gives users access to extensive Personal Data Cleanup services, identity recovery assistance, lost wallet assistance, and the ability to secure all of their devices with world-class defense against threats.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Enormous Growth in Cloud Based Applications

- 4.3.2 Surge in Data Breaches on Public Cloud Environment

- 4.3.3 Everchanging Firewall Protocols for Business Organisations

- 4.4 Market Restraints

- 4.4.1 Complexity in Integrating Hosted Firewalls with On-premise Firewalls

- 4.5 Industry Value Chain Analysis

- 4.6 Industry Attractiveness - Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Service Model

- 5.1.1 SaaS

- 5.1.2 IaaS

- 5.1.3 PaaS

- 5.2 By Deployment Model

- 5.2.1 Private

- 5.2.2 Public

- 5.2.3 Hybrid

- 5.3 By User Type

- 5.3.1 Large Enterprises

- 5.3.2 SMEs

- 5.4 By Industry Vertical

- 5.4.1 BFSI

- 5.4.2 IT & Telecom

- 5.4.3 Healthcare

- 5.4.4 Retail

- 5.4.5 Aerospace & Defence

- 5.4.6 Other Industry Verticals

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 Australia

- 5.5.3.4 Rest of Asia-Pacific

- 5.5.4 Latin America

- 5.5.4.1 Mexico

- 5.5.4.2 Brazil

- 5.5.4.3 Rest of Latin America

- 5.5.5 Middle-East & Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Barracuda Networks, Inc.

- 6.1.2 Cato Networks

- 6.1.3 Check Point Software Technologies, Inc.

- 6.1.4 Cisco Systems, Inc.

- 6.1.5 Forcepoint

- 6.1.6 Fortinet, Inc.

- 6.1.7 IntraSystems

- 6.1.8 Juniper Networks, Inc.

- 6.1.9 Microsoft Corporation

- 6.1.10 Sprout Technologies Ltd

- 6.1.11 Vocus Communications

- 6.1.12 Zscaler, Inc.