|

市場調査レポート

商品コード

1642013

データセンタートランスフォーメーション:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Data Center Transformation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| データセンタートランスフォーメーション:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

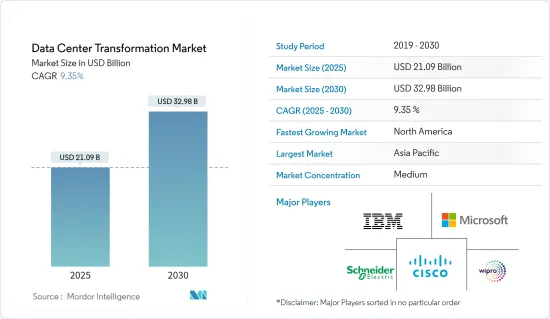

データセンタートランスフォーメーションの市場規模は2025年に210億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは9.35%で、2030年には329億8,000万米ドルに達すると予測されます。

世界中のデータセンタープロバイダーは、運用コストを削減しながら全体的な効率を高めるため、データセンターの変革に向けて徐々に動き出しています。デジタルトランスフォーメーション戦略の一環として、さまざまな企業でクラウド、IoT(モノのインターネット)、ビッグデータ分析の導入が急速に進んでいるため、データセンターの負担も増加しており、世界のデータセンターの成長につながっています。

主なハイライト

- さらに、Ciscoの予測によると、通信機器の増加やSaaS(Software-as-a-Service)ベースのアプリケーションに切り替える企業の増加を考慮すると、世界中のデータセンターのトラフィックも増加しており、これも市場を牽引します。

- 信頼性の向上と世界中のデータセンター数の増加に伴い、データセンタープロバイダーは一貫性と運用効率を維持することが難しくなっています。

- デジタル・インフラに依存する多くの分野でデータセンターサービスの需要が増加し、その結果、データセンターネットワーク・サービスの需要も増加しています。データセンターへのニーズが高まっているのは、インターネットを利用する企業や教育機関が世界中で増加しているためで、必要なプログラムの可用性とデータセキュリティを提供しなければならないです。

- また、総コストの40%近くをエネルギーが占めているため(ネットワーク戦略・技術企業のCienaによる)、データセンターではエネルギー効率への配慮も重要視されています。データセンタートランスフォーメーションの一環としてのインフラ管理は、コスト削減策としてエネルギー効率を高めようとする試みを考慮すると、今後数年間で牽引力を増すと予想されます。

- データセンタートランスフォーメーション市場は、COVID-19の大流行によってプラスの影響を受けました。高セキュリティで信頼性の高いITインフラを提供するクラウドコンピューティングが提供する利点に対する認識の高まりや、ローカルデータセンターの構築需要の高まりも、データセンターの成長を後押ししています。

データセンタートランスフォーメーション市場の動向

eコマース・データベースの重要性が高まり、大きな成長が期待される

- eコマース企業にとって、データセンターは多くの大きなメリットを提供します。また、収集したデータを活用し、極めて有用な顧客インサイトやビジネスプロセスの最適化に役立てる必要があります。

- eコマース・データベースの重要性の高まりは、データセンターを世界中に拡大する重要な原動力となっています。ブランディングやプロモーションなど、さまざまな組織的タスクのためにこれらのデータセットを保存・転送するために、データセンターはインターネット上で販売する企業によって利用されています。

- eコマース・データを取得することで、オンライン小売業者は、分析や顧客情報など、eコマースのさまざまな要素を監視することができます。また、新興国におけるデジタルトランスフォーメーションの高まりが、データセンター市場の成長を促進すると予想されています。

- その結果、データセンター市場は中国やインドなどの新興経済諸国によって大きく刺激されています。デジタルトランスフォーメーションのこの段階では、技術の進化により効率的なデータセンターと関連ソリューションが開発されています。

北米が最大の市場シェアを占める

- 中国インターネット・ネットワーク情報センター(CNNIC)によると、北米地域は世界のクラウドおよびインターネット・データセンターで最大の市場シェアを占めています。この高いシェアは、多くの大手企業がこの地域に本社を置いているためでもあります。

- 北米もまた、IT、BFSI、小売、ヘルスケアなどさまざまなエンドユーザー産業からの世界データセンター需要に大きく貢献しています。

- 連邦政府のデータセンター最適化イニシアチブ(Data Center Optimization Initiative:DCOI)は、主にデータセンター事業者に対し、非効率なインフラの統合、既存施設の最適化、コスト削減の達成、より効率的なインフラへの移行を促すことを目的としています。

- 信頼性と持続可能性への注目が高まっているため、データセンターの所有者と運営者は、燃料電池エネルギー貯蔵のような最先端技術を調査する必要があります。比較的最近の需要源である暗号通貨マイニングのおかげで、最新のコロケーションには不向きと思われる古い資産にも新たな機会が訪れています。

- この発言を一般化すると、政府はこのイニシアチブを通じて、年度末までに物理的なデータセンターのコストを最低でも25%削減する意向です。市場におけるこの地域の優位性は、運用コストを削減するニーズの高まりと相まって、データセンタートランスフォーメーションソリューションの採用余地を提供し、市場を牽引しています。

データセンタートランスフォーメーション産業の概要

データセンタートランスフォーメーション市場は、国内市場だけでなく国際市場でも多くのプレーヤーが活動しているため、半独立市場となっています。市場は適度に集中しており、主要企業は製品や設計の革新戦略を採用しています。市場の主要企業には、IBM Corporation、Cisco Systems, Inc.、Wiproなどがあります。

2023年9月、シュナイダーエレクトリックSEは投資家とのコロブレーションで、Compass Datacentersとの30億米ドルの複数年契約を発表しました。この契約は、両社のサプライチェーンを統合し、プレハブ式モジュラー・データセンターソリューションを製造・提供する既存の関係を拡大するものです。

2022年10月、キンドリルはデル・テクノロジーズおよびマイクロソフト・コーポレーションと共同で、包括的なハイブリッドクラウドソリューションを発表しました。このソリューションにより、データセンター、リモート、メインフレーム環境の顧客は、デル、Kyndrylのマネージドサービス、Microsoft Azureが提供するインフラを活用することで、クラウド変革の旅を加速することができます。

2022年1月、IBMはハイブリッドクラウドの採用を促進するため、IBM Z and Cloud Modernization Centerを立ち上げました。このセンターは、さまざまなツール、リソース、トレーニング、エコシステム・パートナーへのデジタル・ゲートウェイとして機能し、IBM Zの顧客がハイブリッドクラウド環境でアプリケーション、プロセス、データのデジタル化を加速できるよう支援します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヵ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- データセンターのコスト削減と効率化の必要性

- クラウドベースのサービスの採用

- eコマース・データベースの重要性の高まりは著しい成長が見込まれる

- 市場抑制要因

- 低負荷データセンターへの投資に対するROIの懸念

第6章 市場セグメンテーション

- サービス別

- 統合サービス

- 最適化サービス

- 自動化サービス

- インフラ管理

- データセンターのレベル別

- ティア1

- ティア2

- ティア3

- ティア4

- エンドユーザー別

- データセンタープロバイダー

- 企業

- ITおよびテレコム

- BFSI

- ヘルスケア

- 小売

- 製造業

- 航空宇宙、防衛、インテリジェンス

- その他のエンドユーザー

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- IBM Corporation

- Cisco Systems, Inc.

- NetApp, Inc.

- NTT Communications

- Dell EMC(Dell Inc.)

- Microsoft Corporation

- Schneider Electric SE

- HCL Technologies Limited

- Accenture plc

- Wipro Technologies

- Hitachi Vantara Federal, Corporation

- Emerson Network Power, Inc

第8章 投資分析

第9章 市場機会と今後の動向

The Data Center Transformation Market size is estimated at USD 21.09 billion in 2025, and is expected to reach USD 32.98 billion by 2030, at a CAGR of 9.35% during the forecast period (2025-2030).

Data center providers across the globe are gradually moving towards data center transformation in order to increase overall efficiency whilst reducing operational costs. Owing to the rapidly rising adoption of cloud, Ineternet of Things (IoT), and big data analytics across various enterprises as a part of their digital transformation strategy, the burden on the data centers is also increasing, leading to the growth in the data centers globally.

Key Highlights

- Moreover, data center traffic across the world is also increasing, considering the number of increasing communicating devices and more enterprises switching to software-as-a-service (SaaS)-based applications, as forecasted by Cisco, which will also drive the market.

- With the increasing reliability and the increase in the number of data centers around the world, data center providers are finding it difficult to maintain consistency and operational efficiency

- Demand for data center services increased in many sectors which are dependent on digital infrastructures and this has resulted in an increase in the demand for Data Center Network Services. The need for data centres is increasing as a result of the rising number of enterprises and education institutions around the world who are Internet based, which means that they have to provide required program availability and data security.

- Energy efficiency considerations are also gaining importance among data centers since energy accounts for almost 40% of total costs (according to network strategy and technology company Ciena). Infrastructure management, as a part of the data center transformation, is expected to gain traction over the years, considering the attempt to increase energy efficiency as a cost-saving measure.

- The market for data center transformation was positively affected by the COVID 19 pandemic. Increasing awareness of the advantages provided by cloud computing to deliver a high security, reliable IT infrastructure and growing demand for building local data centres has also helped drive Data Centres growth.

Data Center Transformation Market Trends

Increasing Significance of E-commerce Databases are Expected to Grow at a Significant Rate

- For e commerce companies, data centres offer a number of significant advantages. In addition, they need to take advantage of the data that they collect and use it for extremely useful customer insights and business process optimisation.

- The growing importance of e commerce databases is the key driver for expanding data centres around the world. In order to store and transfer these data sets for a variety of organizational tasks, e.g. branding, promotion or anything like that, Data Centres are being used by businesses selling on the Internet.

- Through the acquisition of e-commerce data, online retailers monitor all the many components of their e-commerce, such as analytics or customer information. It is also expected that rising digital transformation in emerging nations fuels data centre market growth.

- Consequently, the market for data centres has been significantly stimulated by developing economies like China and India. At this phase of digital transformation, efficient data centers and related solutions are being developed due to the evolution of technology.

North America Occupies the Largest Market Share

- The North American region holds the largest market share of the global cloud and internet data centers, according to China Internet Network Information Center (CNNIC). This high share can also be because many major players are headquartered in this region.

- North America also contributes substantially to the global data center demand from various end-user industries such as IT, BFSI, retail, and healthcare.

- The Federal government's Data Center Optimization Initiative (DCOI) primarily aims to encourage data center players to consolidate the inefficient infrastructure, optimize existing facilities, achieve cost savings, and transition to a more efficient infrastructure.

- Due to the increased focus on dependability and sustainability, data center owners and operators must investigate cutting-edge technologies like fuel-cell energy storage. Older assets that might be deemed unsuitable for modern colocation are receiving new opportunities thanks to cryptocurrency mining, a comparatively recent source of demand.

- To generalize the statement, through this initiative, the government intends to reduce the costs of physical data centers by a minimum of 25% by the end of the fiscal year. The dominance of this region in the market, combined with the increasing need to reduce operational costs, provides scope for adopting data center transformation solutions, hence driving the market.

Data Center Transformation Industry Overview

The data center transformation market is semi-conslidated owing to the presence of many players in the market operating in the domestic as well as the international market. The market is moderately concentrated, with key players adopting product and design innovation strategies. Some of the major players in the market are IBM Corporation, Cisco Systems, Inc., and Wipro, among others.

In September 2023 - Schneider Electric SE announced at its Collobration with investors a USD 3 billion multi-year agreement with Compass Datacenters. The agreement extends the companies' existing relationship that integrates their respective supply chains to manufacture and deliver prefabricated modular data center solutions.

In October 2022, Kyndryl announced a comprehensive hybrid cloud solution in collaboration with Dell Technologies and Microsoft Corporation. This solution empowers clients in data center, remote, and mainframe environments to expedite their cloud transformation journey by leveraging the infrastructure offered by Dell, Kyndryl's managed services, and Microsoft Azure.

In January 2022, IBM launched the IBM Z and Cloud Modernization Center to facilitate the adoption of hybrid clouds. The center serves as a digital gateway to a wide range of tools, resources, training, and ecosystem partners, assisting IBM Z clients in accelerating the digitization of their applications, processes, and data in a hybrid cloud environment.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Need to Reduce Costs and Increase Efficiency of Data Centers

- 5.1.2 Adoption of Cloud-based Services

- 5.1.3 Increasing Significance of E-commerce Databases are Expected to Grow at a Significant Rate

- 5.2 Market Restraints

- 5.2.1 ROI Concerns Over the Investment across Low Load Data Centers

6 MARKET SEGMENTATION

- 6.1 By Services

- 6.1.1 Consolidation Services

- 6.1.2 Optimization Services

- 6.1.3 Automation Services

- 6.1.4 Infrastructure Management

- 6.2 By Level of Data Center

- 6.2.1 Tier 1

- 6.2.2 Tier 2

- 6.2.3 Tier 3

- 6.2.4 Tier 4

- 6.3 By End User

- 6.3.1 Data Center Providers

- 6.3.2 Enterprises

- 6.3.2.1 IT and Telecom

- 6.3.2.2 BFSI

- 6.3.2.3 Healthcare

- 6.3.2.4 Retail

- 6.3.2.5 Manufacturing

- 6.3.2.6 Aerospace, Defense, and Intelligence

- 6.3.2.7 Other End Users

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Cisco Systems, Inc.

- 7.1.3 NetApp, Inc.

- 7.1.4 NTT Communications

- 7.1.5 Dell EMC (Dell Inc.)

- 7.1.6 Microsoft Corporation

- 7.1.7 Schneider Electric SE

- 7.1.8 HCL Technologies Limited

- 7.1.9 Accenture plc

- 7.1.10 Wipro Technologies

- 7.1.11 Hitachi Vantara Federal, Corporation

- 7.1.12 Emerson Network Power, Inc