自律移動ロボット(AMR):市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Autonomous Mobile Robot (AMR) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日

- 商品コード

- 1851616

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

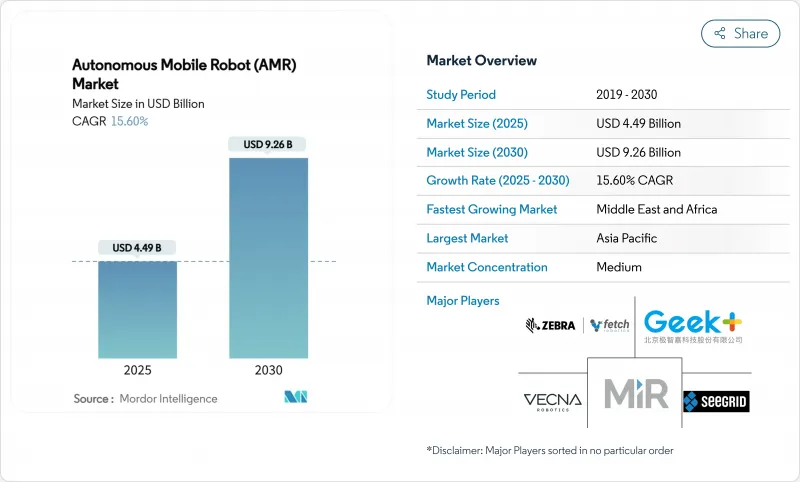

自律移動ロボット(AMR)市場の2025年の市場規模は44億9,000万米ドルで、2030年には92億6,000万米ドルに達し、CAGR 15.6%で拡大すると予測されています。

人工知能、5G-Advancedコネクティビティ、低コストのリチウムイオンバッテリーの急速な普及が、フルフィルメント、製造、ヘルスケア環境における商業的実現性を加速させる。オペレータは、労働力不足を補い、固定コンベア・インフラを構築することなく24時間365日の処理能力を獲得し、職場の安全性を向上させるためにロボットを導入します。アジア太平洋地域では、ソフトウェア中心の設計と積極的な価格設定を融合させた中国のサプライヤーが採用をリードし、中東ではメガプロジェクトがヘビーデューティシステムへの新たな需要を生み出しています。ベンダーはフリートレベルのオーケストレーション・ソフトウェアの組み込みや、Time-to-Valueを短縮するチャネル・パートナーシップの確保を競い、競合は激化します。EUの「Factory of the Future(未来の工場)」助成金のような規制上の優遇措置は、中小企業の資本支出を補助することで、普及をさらに促進します。

世界の自律移動ロボット(AMR)市場の動向と洞察

eコマースにおけるフルフィルメント需要の急増

オンライン小売は現在、即日配達の期待にかかっています。アマゾンは2025年7月までに100万台のロボットを配備し、DeepFleetのフリート・インテリジェンスによってピッキング1回あたりの移動時間を10%短縮しました。Locus Roboticsは、LocusOneソフトウェアを統合し、生産性を2倍から3倍に高めると同時に、怪我を80%削減し、30億ピックを突破しました。そのため、小売業者は、季節ごとの数量に合わせてフレキシブルに対応し、設備の変更を最小限に抑えられるコンパクトな自律移動ロボットの市場ソリューションを採用しています。Geek+-Intelのデザインで紹介されているビジョン専用ナビゲーションは、固定マーカーが不要なため、設置コストと時間を削減できます。

OECD市場における倉庫労働者の不足

OECD加盟国の事業者は、夜間シフトや繁忙期シフトに欠員が絶えないことを報告しています。欧州労働安全衛生庁は、労働年齢人口の減少を補うためには自動化が不可欠であると強調しています。Skechers社は、コンベアをロボットに置き換えた後、80%のエネルギー節約を記録し、熟練労働者が不足している場合の投資対効果を検証しました。雇用主は現在、ロボットの監督とメンテナンスを中心にロールを再設計し、倉庫の仕事を肉体的負担の少ない魅力的なものにしています。

断片的な相互運用性標準

ISO 3691-4とANSI/RIA R15.08は安全性について詳述しているが、フリート通信プロトコルを省略しているため、バイヤーは単一ベンダーのエコシステムに入ることを余儀なくされ、統合コストが膨れ上がっています。ミドルウェアサプライヤーはギャップを埋めようとしているが、独自のデータフォーマットは展開を遅らせ、交渉力を低下させる。

セグメント分析

2024年の売上高の46.0%は無人地上車両が占める。ヒューマノイドは歴史は浅いが、レイアウトを変更することなく人間が設計した空間を移動するため、CAGR 19.22%で拡大すると予測されます。アマゾンは、リヴィアンの電動バンから小包を積み込むヒューマノイド型運び屋を試験的に導入しており、自律移動ロボット市場の屋外拡張を示唆しています。無人航空ロボットや海洋ロボットは依然としてニッチだが、エネルギー資産の点検には欠かせないです。ヒューマノイドの自律型移動ロボット市場規模は、操作の信頼性が倉庫の性能ベンチマークに達すれば、急速に上昇する可能性が高いです。

従来のフリートは、1つのタスクに最適化された特殊なフォームファクターに依存しているが、汎用性に欠けています。ヒューマノイドは、1つのプラットフォームで棚入れから仕分けまで役割を切り替えることができるため、フリートの簡素化を約束します。そのため投資は、純粋なモビリティ・ハードウェアから、人間の器用さに匹敵する人工知能のビジョンと把持能力へとシフトしています。この移行は、ライフサイクルコストを下げ、ロボット・アズ・ア・サービス・サブスクリプションのような新たなサービスモデルを解放すると思われます。

LiDAR SLAMは、混雑した通路でのミリメートル・レベルの再現性があるため、2024年には41.5%のシェアを占める。CAGR21.22%で拡大するビジョンベースのシステムは、高価なセンサーや反射ターゲットが不要なため、中堅市場のオペレータの資本支出を削減できます。Geek+は、インテル・リアルセンス・デプスカメラとオンボードAIにより、LiDARと同等の精度を実証しました。エッジプロセッサーが低電力予算でリアルタイムの画像セグメンテーションを処理するため、ビジョンナビゲーションの自律移動ロボット市場規模はさらに拡大します。

ハイブリッド・センサー・フュージョンは、カメラ、LiDAR、慣性センサーを組み合わせることで、フリートはほこり、まぶしさ、帯域幅の制約が現れたときにモードを切り替えることができます。この適応的アプローチは、港湾の倉庫が現在要求している屋内と屋外の混在したオペレーションをサポートします。様々なモダリティの性能を認証する標準規格は、マルチセンサの採用を加速し、ロボットが公共の通路を横断する際の安全性を確保します。

自律移動ロボット(AMR)市場セグメンテーション:タイプ別(無人地上車両、ヒューマノイド、その他)、ナビゲーション技術別(LiDAR SLAM、ビジョンベース、磁気/誘導/QRガイド、その他)、エンドユーザー産業別(倉庫・物流、製造、自動車、その他)、地域別。市場予測は金額(米ドル)で提供されます。

地域分析

アジア太平洋地域は2024年の売上の37.8%を創出。Geek+のような中国企業は生産の3分の1以上を輸出しており、コスト面での優位性と、試験運用を促進する政府支援プログラムを活用しています。多くの日本や韓国の工場は、投資回収期間を短縮するため、中国ブランドからロボットを調達しています。北米は、アマゾンの多拠点展開と、サードパーティの物流プロバイダー向けにオーケストレーション・レイヤーを調整するソフトウェア新興企業のエコシステムが充実しているため、自律型移動ロボット市場第2位の座を維持しています。

欧州は構造化された補助金の恩恵を受けています。EUの「Factory of the Future(未来の工場)」イニシアチブは、オートメーション・ハードウェアの資本支出を最大20%まで払い戻し、中堅メーカーの採用を加速させています。2025年以降に助成金が開始されるため、欧州の自律移動ロボット市場シェアは上昇すると思われます。中東・アフリカは、サウジアラビアのビジョン2030とNEOMの建設ロボットへの7億7,460万米ドルのコミットメントに牽引され、CAGR19.0%で最も急成長している地域です。高いロジスティクス費用とグリーンフィールド倉庫により、事業者は初日からロボットを中心に設計することができます。

南米はまだ初期段階です。ブラジルとメキシコでは、輸入オートメーションに対する免税措置が試験的な導入を促しているが、為替変動が大きく普及は遅れています。アフリカでの導入は、自動車組立工場がラインサイドへのジャスト・イン・タイム納入を要求する南アフリカとモロッコに集中しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 急速なeコマース・フルフィルメント需要

- OECD市場における倉庫労働者の希少性

- リチウムイオン電池のkWhごとの価格下落が70米ドルを下回る

- 2025年以降のEU「未来の工場」補助金

- 5G-先進プライベートネットワークの展開

- AI対応「スウォーム・オーケストレーション」プラットフォーム

- 市場抑制要因

- 細分化された相互運用性標準

- サイバーフィジカル・セキュリティの脆弱性

- 大容量AMRのための高額な初期投資

- ロボット密度制限に対する労働組合の反発

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- タイプ別

- 無人地上車両(UGV)

- ヒューマノイド

- 無人航空機(UAV)

- 無人海洋機(UMV)

- ナビゲーション技術別

- LiDARスラム

- ビジョンベース(2D/3Dカメラ)

- 磁気/ 誘導/QRガイド

- ハイブリッド&マルチセンサー・フュージョン

- ペイロード容量別

- 100kg未満

- 100-500 kg

- 500-1,000 kg

- 1,000kg以上

- エンドユーザー業界別

- 倉庫・ロジスティクス

- 製造業

- 自動車

- 飲食品

- ヘルスケア

- 小売とeコマース

- 防衛と安全保障

- 鉱業・鉱物

- エネルギーと電力

- 石油・ガス

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 中東

- イスラエル

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Zebra Technologies Corporation(Fetch Robotics)

- Teradyne Inc.-Mobile Industrial Robots(MiR)

- Geek+Technology Co., Ltd.

- Vecna Robotics, Inc.

- Seegrid Corporation

- Aethon, Inc.(ST Engineering)

- Omron Corporation

- Clearpath Robotics Inc.(OTTO Motors)

- HIK Robot Co., Ltd.

- SoftBank Robotics Group Corp.

- SMP Robotics Systems Corp.

- Locus Robotics Corp.

- Amazon.com, Inc.(Kiva/System Robotics)

- Agilox Services GmbH

- Balyo SA

- Vendor Positioning Analysis

- Investment Analysis

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 150 Pages

- 納期

- 2~3営業日