|

市場調査レポート

商品コード

1536962

消防用航空機:市場シェア分析、産業動向、成長予測(2024~2029年)Firefighting Aircraft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 消防用航空機:市場シェア分析、産業動向、成長予測(2024~2029年) |

|

出版日: 2024年08月14日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

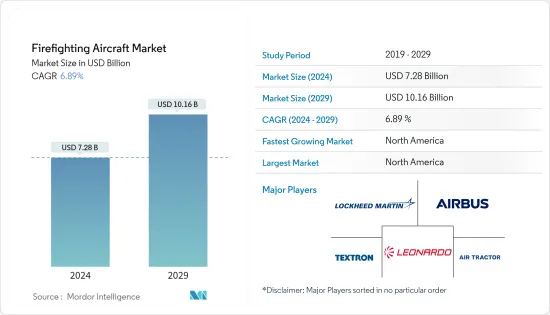

消防用航空機市場規模は2024年に72億8,000万米ドルと推定・予測され、2029年には101億6,000万米ドルに達し、予測期間(2024-2029年)のCAGRは6.89%で成長すると予測されています。

消防用航空機には液体貯蔵用の大型容器が必要です。これには、航空機のホールドエリアにあるタンク、外部タンク、またはその組み合わせが含まれます。タンクは水やその他の消火剤を貯蔵するのに役立ち、航空機から投下して消火に使用されます。世界の山火事の深刻化と頻度の増加により、積載量と運用範囲の拡大という点で、消防用航空機の技術的進歩に対する需要が高まっています。

技術の進歩には、積載量の増加、運用範囲の拡大、消火剤の展開精度の向上などが含まれます。山火事管理と空中消防隊に対する政府の投資が市場を牽引しています。広く使用されている消防用航空機には、ボーイングB747、マクドネル・ダグラスDC-10、BAe146などがあります。

市場の成長を妨げているのは、運航コストの高さ、航空安全のための厳しい規制基準、消火活動に使用される化学物質に対する環境問題などの課題です。運航コストの高さは、消防用航空機市場が直面する深刻な課題のひとつであり、主に燃料費の高騰、メンテナンスコスト、特殊な装備品の必要性などが原因となっています。

消防用航空機市場の動向

予測期間中、回転翼機セグメントが市場を独占する

消防任務には、費用対効果と適合性に基づいて幅広いヘリコプターが選択されます。固定翼機に比べ、回転翼機は水や消火剤の運搬量が少なく、消防士や機材の輸送量も少ないです。ヘリコプターは、小規模な山火事に対する迅速な初期攻撃に役立ちます。新たな技術開発によって運用効率が向上し、より安全で信頼性の高いものとなった。揚力は増大し、高度な水滴降下システムや強化された飛行制御システムが導入され、消火任務での有効性が高まった。さらに、高度な調整技術や通信技術を取り入れることで、空中での活動と地上での活動をよりうまく統合できるようになり、全体的な消火戦略の向上が確実になった。

さまざまな国で、ヘリコプターに最新の内部水タンクを搭載することで、ヘリコプターを消防士に改造しています。2023年3月、ユナイテッド・ロータークラフト社は、緊急救助・消防ヘリコプター・プログラムのためのいくつかのオプションと近代化の評価を開始しました。アップグレードには、同社がダート社と共同で開発した1,000ガロンの複合水タンクが含まれます。さらに2023年11月、レオナルドはOmni Helicopters Internationalと、消防能力を強化するためにAW189およびA189 Kヘリコプターを供給する契約を締結しました。これらの高効率で耐久性の高いヘリコプターは、同地域における消防任務の運用効率を向上させる。この契約は、消防活動における持続可能性と信頼性を重視するOHIヘリコプターズ・インターナショナルの方針に沿ったものです。

予測期間中、北米が最も高い市場シェアを占めると予測

予測期間中、北米が最も高い市場シェアを占めると予測されています。山火事は米国やカナダなどの北米諸国で多発しています。山火事の原因は、落雷などの自然現象によるものと、電気機器の不具合、発煙筒の未消火、自動車の過熱、放火などの人為的行為によるものがあります。米国国家機関間火災センターの報告書によると、2023年には約55,571件の山火事事故が発生しました。同様に、カナダでは同年、1,650万ヘクタールの土地で6,132件の山火事が発生したと報告されています。

この地域の山火事対策機関は、大型エアタンカー(LAT)、シングル・エンジン・エアタンカー(SEAT)、超大型エアタンカー(VLAT)、スモークジャンパー、ウォータースクーパーなど、さまざまなタイプの消火用航空機を使用しています。一言で言えば、高い技術力、強力な政府支援、山火事の多さが、この地域の世界消防市場における最大シェアを支えています。この優位性は、航空機技術の継続的な進歩や、山火事管理の有効性向上を目指した戦略的イニシアティブによって支えられています。

例えば、2024年4月、サスカチュワン州公共機関は、4機の再利用エアタンカーの調達に約1億8,700万米ドルを投資する計画を発表しました。連邦政府はこの投資を支援するために1,600万米ドルを拠出しており、航空消防隊の更新と近代化に対するコミットメントが高まっていることを示しています。

消防用航空機産業の概要

消防用航空機市場は統合されており、少数の企業が市場で大きなシェアを占めています。市場の主要企業には、ロッキード・マーチン・コーポレーション、エアバスSE、レオナルドSpA、テキストロン社、エアトラクター社などがあります。主要企業は、合弁事業やパートナーシップの形成によって戦略的な動きを見せています。主要OEMは、提携を通じて世界市場でのプレゼンスを拡大することに注力しています。例えば、2024年1月、エアバス(フランス)とタタ・グループ(インド)は、H125ヘリコプターの最終組立ラインのために提携しました。この提携は、航空宇宙産業におけるインドとフランスの関係強化を強調しています。このような動きは、航空機の能力を強化し、世界市場における主要企業の事業展開の足跡を増やすことになります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 航空機の種類

- 回転翼機

- 固定翼機

- 最大離陸重量

- 50,000kg未満

- 50,000kg以上

- 地域

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Lockheed Martin Corporation

- Viking Air Ltd

- ShinMaywa Industries Ltd

- MD Helicopters Inc.

- Textron Inc.

- Kaman Corporation

- Airbus SE

- Leonardo SpA

- Hynaero

- Air Tractor Inc.

- De Havilland Aircraft of Canada Limited

第7章 市場機会と今後の動向

The Firefighting Aircraft Market size is estimated at USD 7.28 billion in 2024, and is expected to reach USD 10.16 billion by 2029, growing at a CAGR of 6.89% during the forecast period (2024-2029).

Firefighting aircraft need large containers for liquid storage. These include tanks in the airplane hold area, external tanks, or a combination. The tank helps store water or any other retardant, which is used to extinguish the fire by dropping it from the aircraft. Increasingly, the higher severity and frequency of wildfires worldwide are driving the demand for technological advancements in firefighting aircraft in terms of increasing payload capacities and operational range.

Technological advances include increases in payload capacities, operational range, and accuracy of retardant deployment. Government investments in wildfire management and aerial firefighting fleets are driving the market. Some of the widely used firefighting aircraft are Boeing B747, McDonnell Douglas DC-10, and BAe 146 aerial firefighting aircraft.

The market's growth is hampered by challenges such as the high cost of operations, stringent regulatory standards for aviation safety, and environmental concerns over the chemicals used in fighting fires. The high cost of operations is among the severe challenges faced by the firefighting aircraft market, mainly attributed to higher fuel costs, maintenance costs, and specialized equipment requirements.

Firefighting Aircraft Market Trends

The Rotorcraft Segment will Dominate the Market During the Forecast Period

A wide range of helicopters are selected for firefighting missions based on cost-effectiveness and suitability. Compared to fixed-wing aircraft, rotorcrafts can carry less water or fire retardant and transport fewer firefighters and equipment. Helicopters are helpful for quick initial attacks on smaller wildfires. The new technological developments have improved operational efficiency and made them safer and more reliable. The lift capacity has increased, and advanced water drop systems and enhanced flight control systems have been installed to increase their effectiveness in firefighting missions. Furthermore, incorporating advanced coordination and communication technologies enables better integration of aerial efforts with ground operations, ensuring an improvement in overall firefighting strategies.

Various countries are converting helicopters into firefighters by installing modern internal water tanks. In March 2023, United Rotorcraft started evaluating several options and modernizations for the emergency rescue and firefighting helicopter program. The upgrades included a 1,000-gallon composite water tank, which the company developed in collaboration with Dart. Furthermore, in November 2023, Leonardo signed a contract with Omni Helicopters International to supply AW189 and A189 K helicopters to enhance firefighting capabilities. These high-efficiency, extended-endurance helicopters will improve the operational effectiveness of firefighting missions within the region. The deal aligns with OHI Helicopters International's focus on sustainability and reliability in firefighting operations.

North America Projected to Hold the Highest Market Share During the Forecast Period

North America is projected to hold the highest market share during the forecast period. Wildfires are prevalent in North American countries such as the United States and Canada. They may be caused by natural causes such as lightning or human activity, such as faulty electrical equipment, unextinguished smoking materials, overheating automobiles, or arson. The US National Interagency Fire Center report stated that around 55,571 wildfire incidents occurred in 2023. Similarly, Canada reported 6,132 incidents of wildfires that affected an area of 16.5 million hectares of land in the same year.

Wildfire control agencies in the region use different types of firefighting aircraft, such as Large Airtankers (LATs), Single Engine Airtankers (SEATs), Very Large Airtankers (VLATs), Smokejumpers, and Water Scoopers. In a nutshell, high technological capabilities, strong government support, and a high number of wildfires help the region account for the largest share of the global firefighting market. The dominance is supported by ongoing advancements in aircraft technology and strategic initiatives aimed at improving the effectiveness of wildfire management.

For instance, in April 2024, the Saskatchewan Public Agency announced plans to invest approximately USD 187 million in procuring four repurposed air tankers. The federal government has contributed USD 16 million to support the investment, which underlines a growing commitment to updating and modernizing aerial firefighting fleets.

Firefighting Aircraft Industry Overview

The firefighting aircraft market is consolidated, with a few players holding significant shares in the market. Some of the key players in the market are Lockheed Martin Corporation, Airbus SE, Leonardo SpA, Textron Inc., and Air Tractor Inc. Key players are making strategic moves by forming joint ventures and partnerships. The key OEMs are focusing on expanding their global market presence through alliances. For instance, in January 2024, Airbus (France) and Tata Group (India) partnered for a final assembly line for the H125 Helicopter. The partnership emphasizes strengthening ties between India and France in the aerospace industry. These moves will enhance aircraft capabilities and increase key players' operational footprint in the global market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Driver

- 4.3 Market Restraint

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Aircraft Type

- 5.1.1 Rotorcraft

- 5.1.2 Fixed-wing

- 5.2 Maximum Take-off Weight

- 5.2.1 Below 50,000 kg

- 5.2.2 Above 50,000 kg

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Latin America

- 5.3.5 Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Lockheed Martin Corporation

- 6.2.2 Viking Air Ltd

- 6.2.3 ShinMaywa Industries Ltd

- 6.2.4 MD Helicopters Inc.

- 6.2.5 Textron Inc.

- 6.2.6 Kaman Corporation

- 6.2.7 Airbus SE

- 6.2.8 Leonardo SpA

- 6.2.9 Hynaero

- 6.2.10 Air Tractor Inc.

- 6.2.11 De Havilland Aircraft of Canada Limited