|

|

市場調査レポート

商品コード

1851031

ドローン:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Drones - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ドローン:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月17日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

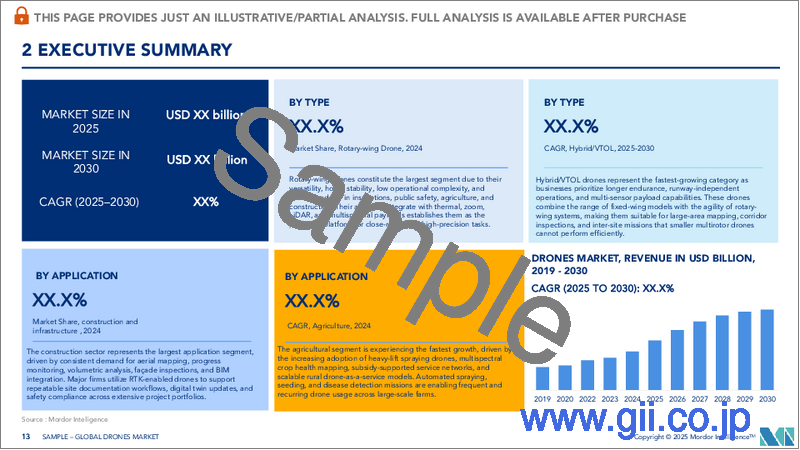

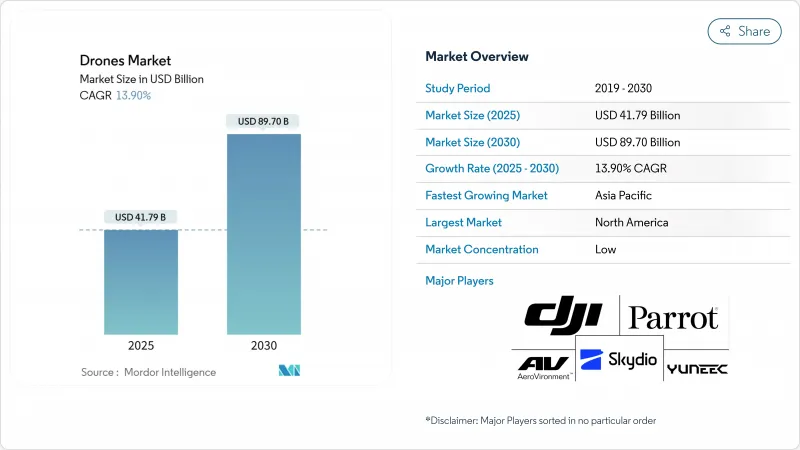

ドローン市場規模は2025年に417億9,000万米ドルに達し、2030年には897億米ドルに達する見込みです。

搭載されたエッジAIが10W以下のチップセットで複雑な知覚アルゴリズムを実行し、建設、エネルギー、農業で自律型ミッションが実行可能になるにつれて、採用が加速します。マルチアクセスエッジコンピューティング(MEC)を備えた5Gの急速な展開により、信頼性の高いBeyond Visual Line-of-Sight(BVLOS)制御をサポートする10ms以下のレイテンシが提供される一方、センサーの急激な価格低下により、高度なペイロードが小規模事業者にも開放されます。特にFAAのBVLOS規則案やICAOの新基準・推奨慣行(SARPs)といった規制の動きは、空域アクセスの拡大を示唆しています。しかし、リチウムイオン電池の不足やレアアース材料の輸出抑制など、サプライチェーンのひずみは引き続き材料費の高騰を招き、裁量需要を減退させる可能性があります。全体として、競争はハードウェア、AIソフトウェア、規制遵守をエンドツーエンドの価値提案にバンドルできる企業へとシフトしており、ドローン市場全体の統合が加速しています。

世界のドローン市場の動向と洞察

オンボードエッジAIの成熟:リアルタイム処理が自律的なオペレーションを実現

エッジ推論エンジンは、7-10Wの軽量プロセッサで物体検出、経路計画、不測事態ロジックを実行するようになり、ドローンは複雑な環境でもバックホールのレイテンシなしに適応できるようになりました。公益事業者は、AIを搭載した船舶が異常を検知し、詳細な画像処理のために自律的に再配置することで、ダウンタイムが最大35%削減され、ROIが高まったと報告しています。大規模な言語モデルが安全スタックに統合され、衝突回避の判断品質が向上しています。

5GとMECのロールアウト:超低遅延によるBVLOSの実現可能性

キャリアエッジノードと組み合わせたスタンドアロン5Gネットワークは、10ミリ秒以下の往復遅延を実現し、地上ベースの無線リレーの必要性を排除します。ValmontがT-Mobileの5Gグリッド上で行った77マイルのBVLOS検査では、永続的なコマンドリンクとリアルタイムのビデオバックホールが検証されました。FCCのパート88ルールは、ドローンコマンドチャンネル用に保護された5030-5091MHzのコリドーをさらに強化します。

リチウムイオンセルの供給不足が小型UAVの部品コストを押し上げる

バッテリーセルは一般的な小型ドローンのコストの4分の1を占め、2024年以降の30~40%の値上げにより、OEMはマージンの圧縮を吸収するか、販売価格の引き上げを余儀なくされています。地政学的緊張とEV需要の増加が不足を悪化させ、中国の主要なバッテリー鉱物の輸出抑制が長期的な生産能力を脅かしています。

セグメント分析

2024年のドローン市場の39.45%は建設業が占め、空撮による進捗追跡、3Dモデリング、現場セキュリティが主流となりました。高解像度の写真測量は、手作業に比べて測量時間を70%以上短縮し、自動化された数量計算は支払いサイクルを早める。エネルギー業界は規模こそ小さいもの、CAGRは19.05%で、2030年までにその差を縮める可能性があります。公益事業会社は現在、ヘリコプターをAI誘導ロータークラフトに切り替え、1回の出撃で絶縁体の亀裂や熱のホットスポットを発見し、年間約60%のコスト削減を達成しています。農業は、FAA(連邦航空局)が承認した群散布のおかげで、そのすぐ後に続いています。ハイリオ社などの企業によると、現在、クライアントの半数以上が、広大な土地をカバーするために複数のドローンスウォームを導入しています。

公共安全やエンターテインメント分野でも勢いが増しています。トライアルでは、ドローンによる初動対応(DFR)プログラムにより、出動時間が8分から3分半に短縮され、地域警察活動の効率が向上しました。シネマトグラフィーはペイロードの革新を推し進め、より幅広いセンサーの統合を促しています。これらの動向は、ドローン市場が徐々に多様化し、それぞれのニッチが特定の機体、センサー、自律性の要件を最適化していることを示しています。

固定翼機は2024年の売上高の45.07%を占め、パイプラインのような長い直線通路でのエネルギー消費が少ないことが評価されています。しかし、ハイブリッドVTOL航空機は、都市部のエアモビリティ事業者がスペースに制約のある屋上に合わせて垂直離陸する必要があるため、CAGR20.10%で拡大しています。通信タワーの点検や捜索救助のようなホバリング作業には、回転翼ユニットが不可欠であることに変わりはないです。EHangのEH216-Sは世界初を達成しました。複合材料の採用も差別化要因のひとつです。炭素繊維強化ポリマーの機体は、剛性を保ちながら重量を最大15%削減し、航続距離を直接伸ばします。一方、バイオベースの樹脂は、2024年にパイロットレスの旅客機eVTOLのドローン型式証明を取得し、ハイブリッドの実現可能性を強調する中で、環境に対する監視が高まっていることを反映し、使用後のリサイクル性に期待が持てる。

複合材料の採用も差別化要因のひとつです。炭素繊維強化ポリマーの機体は、剛性を保ちながら重量を最大15%削減し、航続距離を直接伸ばします。一方、バイオベースの樹脂は、ドローン業界全体で環境に対する監視の目が高まっていることを反映し、使用後のリサイクル性で有望視されています。

地域分析

北米は、FAAのテストサイトプログラムとコマンドリンク用の5030~5091MHzの専用周波数帯に後押しされ、2024年の世界売上高の37.97%を稼いです。WingとWalmartは、完全に統合されたUTMサービスを使用して15万件の小包配達を達成し、大規模な商業的準備態勢を実証しました。しかし、米国安全保障ドローン法(American Security Drone Act)は、連邦政府が保有する中国製機体に代わる国産機体の生産を奨励しており、データ・セキュリティに関する政策は強化されています。

アジア太平洋地域は、CAGR15.27%で最も急成長している地域です。中国の「低高度経済」戦略は、2035年までに3兆5,000億元(4,870億米ドル)の市場を目標としており、試験コリドーや購入補助金で地元のチャンピオンを支援しています。インドの輸入禁止措置は、外国OEMの参入を阻むが、PLIスキームの下、新興の製造クラスターを活性化させる。日本と韓国は、高い災害対策予算を反映して、ドローンをインフラ点検と津波対応ミッションに振り向ける。

欧州は、160万人以上の登録事業者を管理するEASAの統一されたUスペースの青写真に支えられ、依然として極めて重要です。厳しいプライバシー・バイ・デザインの義務化により、配備サイクルは長期化するが、ドローンによる洋上風力発電のメンテナンスのような持続可能性を重視したプロジェクトは、需要の増加を維持しています。同大陸はまた、eVTOL試験用の特定の通路を承認しており、メーカーは2020年代後半までにエアタクシーの認証取得に向けた明確な道を歩むことになります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 車載エッジAIの成熟:リアルタイム処理が自律的なオペレーションを可能にする

- 5GとMECの展開:超低遅延がBVLOSの実現を可能にする

- センサーコストの暴落:マルチスペクトルとLiDARの価格下落がROIを拡大

- U-スペース/UTMの標準化:ICAOとの連携で国境を越えたオペレーションが加速

- オンデマンド物流ブーム

- 脱炭素化の経済学

- 市場抑制要因

- 小型UAVの部品コストを押し上げるリチウムイオン電池の供給不足

- インドの厳しいRPAS輸入禁止措置が海外OEMの収益を制限

- EUのプライバシー・バイ・デザイン規則が都市部での採用を遅らせる

- 5Gのミリ波帯とのスペクトラム共有の競合

- バリューチェーン分析

- 規制の見通し

- テクノロジーの展望

- ポーターのファイブフォース分析

- 買い手の交渉力/消費者

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 用途別

- 建設

- 農業

- エネルギー

- エンターテイメント

- 法執行

- その他の用途

- タイプ別

- 固定翼ドローン

- ロータリーウイングドローン

- ハイブリッド/VTOLドローン

- 体重クラス別

- ナノ/マイクロ(2kg未満)

- 小型(2~25kg)

- 中型(25~150kg)

- 大型(150kg以上)

- 運用モード別

- 遠隔操縦

- 有人操縦オプション

- 完全自律型

- エンドユーザー別

- 商業および消費者

- 政府および民間

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 南米

- ブラジル

- その他南米

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- その他中東

- アフリカ

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- SZ DJI Technology Co., Ltd.

- Parrot Drones SAS

- AeroVironment, Inc.

- Skydio, Inc.

- The Boeing Company

- Yuneec International Co. Ltd.(ATL Global Holding AG)

- Terra Drone Corporation

- Delair SAS

- Autel Robotics Co., Ltd.

- Guangzhou EHang Intelligent Technology Co. Ltd.

- AgEagle Aerial Systems Inc.

- UVify Inc.