|

市場調査レポート

商品コード

1444824

ワイヤレスECGデバイス:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Wireless ECG Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ワイヤレスECGデバイス:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 112 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

ワイヤレスECGデバイスの市場規模は、2024年に18億4,000万米ドルと推定され、2029年までに22億7,000万米ドルに達すると予測されており、予測期間(2024年~2029年)中に4.35%のCAGRで成長します。

パンデミック期間中、COVID-19はワイヤレスECGデバイス業界に大きな影響を与えました。 2021年1月にヨーロピアンハートジャーナルに掲載された記事によると、入院していないCOVID-19症患者を対象に、スマートフォンを使った自宅心電図モニタリングにより、疾患に関連した心臓合併症と心電図変化の存在を特定することができました。さらに、COVID-19のパンデミックにより、パンデミックの初期段階で課された厳格なロックダウン規制により、遠隔医療および仮想ソリューションの需要が増加しました。パンデミック中は心臓ケア施設への患者のアクセスが制限されていたため、これらの遠隔監視システムは世界中で非常に人気がありました。したがって、COVID-19はワイヤレスECGデバイス市場に大きな影響を与えました。さらに、ワイヤレスECGデバイスの需要はパンデミック後の期間もそのまま維持されると予想されます。

ワイヤレスECGデバイス市場の成長を促進する主な要因には、高齢者人口の増加、心血管疾患の発生率の増加、遠隔監視技術の技術進歩が含まれます。たとえば、2022年 1月に発表された英国心臓財団(BHF)のデータによると、2021年に世界中で影響を受けた最も一般的な心臓病は、冠状動脈(虚血性)心疾患(世界有病率は2億人と推定)、末梢動脈(血管)疾患(1億1,000万人)、脳卒中(1億人)、心房細動(6,000万人)です。同報告書はまた、北米での心臓および循環器疾患の有病率が4,600万人、欧州で9,900万人、アフリカで5,800万人、南米で3,200万人、アジアとオーストラリアで3億1,000万人であると述べた。したがって、世界人口における心血管疾患の数の多さにより、より正確で使いやすいワイヤレスECGデバイスの需要が高まる可能性があります。これは市場の成長につながります。

さらに、国連が2022年に発行した報告書では、世界人口に占める65歳以上の人口の割合が2022年の10%から2050年には16%に上昇すると予測されています。今後数年間で市場は成長します。また、心臓病になりやすい高齢者の数が増えていることも助けになると期待されています。

さらに、大手企業は市場での存在感を高めるためにさまざまな戦略を採用しており、それが市場の成長をさらに促進する可能性があります。たとえば、2022年 1月にフィリップスは、分散型臨床試験で使用するための12誘導心電図ソリューションを発売しました。臨床グレードのソリューションは、同社の心臓モニタリング製品ラインの中で最も先進的な患者中心のECGです。そのデータ読み取り値は、臨床現場で使用されるECGのデータ読み取り値と同様です。したがって、市場の成長は、高齢者の数の増加、心血管疾患を患う人の数の多さ、主要な市場企業による新製品の定期的なリリースによって促進される可能性があります。

しかし、心血管疾患に対する複雑な償還政策や正確な報告の誤りにより、市場の成長は鈍化する可能性が高いです。

ワイヤレスECGデバイスの市場動向

監視システムセグメントは、予測期間中に最も急速に成長するセグメントになると予想されます

心血管疾患の発生率の増加と高齢者人口の増加により、継続的な心血管モニタリングECGシステムセグメントは予測期間中に成長すると予想されており、日常生活における患者の心臓の継続的な心血管モニタリングの必要性が高まる可能性があります。たとえば、2021年9月に発行されたMDPIジャーナルの調査論文では、末梢動脈疾患(PAD)の世界の有病率は3~12%と推定されており、アメリカと欧州の約2,700万人が罹患していると報告されています。同情報筋はまた、欧州では、PADの有病率が45歳から55歳の間で約17.8%であると推定されていると報告しています。このような心血管疾患の有病率の高さは、継続的な心血管モニタリング ECGシステムに対する需要の増大に寄与すると予想されます。セグメントの成長を促進します。

心血管疾患の早期発見と管理に対する意識の高まりにより、継続的な心血管心電図モニタリング装置の需要が増大しています。たとえば、世界心臓連盟(WHF)は毎年9月29日に世界心臓デーを祝います。 WHFは、2022年9月に心臓の健康に対する意識を高めるキャンペーンを計画しています。毎年90か国以上がこの国際的な行事に参加しています。その結果、世界心臓デーは心血管疾患に関する情報を広める効果的な手段であることが証明されました。

継続的な心血管モニタリングECGシステムに対する需要の高まりに応えるために必要な革新的な製品の発売も、この分野の成長を促進すると予想されます。たとえば、バイオトリシティは2022年 4月に、米国FDAの認可を受けたワイヤレスウェアラブル心臓モニタリングデバイスBiotresを発売しました。この製品は、2022年 2月下旬から医師、診療所、病院、個人ユーザー向けに予約注文を開始しました。

北米では、予測期間中にワイヤレスECGデバイス市場の成長が見込まれる

北米はワイヤレスECGデバイス市場で大きなシェアを占めており、予測期間中に同様の傾向を示すと予想されます。高齢者人口の増加や心血管疾患の発生率の増加などの要因が、調査対象地域の市場の成長を促進しています。たとえば、2022年の心臓病および脳卒中統計最新ファクトシートによると、米国では約40秒ごとに1人が心筋梗塞を発症すると予想されています。同様に、2021年9月に更新されたCDCは、米国の40歳以上の約650万人が末梢動脈疾患を患っていると報告しました。また、カナダ心臓脳卒中財団の2022年2月の報告書によると、国内では75万人が心不全を抱えており、毎年10万人が心不全と診断されています。

さらに、主要企業の存在と頻繁な製品の承認、発売、開発が、この地域の市場の成長に貢献すると予想されます。たとえば、2022年 10月にQT Medicalは、小児患者に使用する12誘導心電図のPCA 500に関するFDA認可を取得しました。この認可により、新生児、乳児、小児、青少年を含むすべての小児集団に使用の適応が拡大されました。

したがって、高齢者人口の増加や心血管疾患の発生率の増加などの上記の要因、主要製品の発売がこの地域の市場の成長に貢献すると予想されます。

ワイヤレスECGデバイス業界の概要

ワイヤレスECGデバイス市場は、市場に少数の大手企業と小規模企業が存在するため、適度に統合された市場です。市場関係者は、市場向けに技術的に高度な製品を開発するための研究開発に注力しています。主要な市場企業は、日本光電株式会社、メドトロニック、ゼネラルエレクトリックカンパニー(GEヘルスケア)、エアロテルメディカルシステムズ、およびAliveCor Inc.などです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 高齢者人口の増加と心血管疾患の発生率の増加

- ワイヤレス技術のコスト低下

- 遠隔監視技術の技術進歩

- 市場抑制要因

- 心血管疾患(CVD)に関する複雑な償還ポリシー

- 正確なレポートの不正確さ

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の競合関係の激しさ

第5章 市場セグメンテーション

- 製品タイプ別

- ECGシステムのモニタリング

- リモートデータモニタリング

- イベント監視

- 継続的な心血管モニタリングシステム

- 診断用ECGシステム

- 安静時心電図システム

- ストレス心電図システム

- ホルター心電図システム

- ECGシステムのモニタリング

- エンドユーザー別

- 病院

- 在宅ユーザー

- その他のエンドユーザー

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Aerotel Medical Systems Ltd

- AliveCor Inc.

- BPL Medical Technologies

- Bittium

- CardioComm Solutions Inc.

- GE Healthcare

- iRhythm Technologies Inc.

- MediBioSense Ltd

- Medtronic PLC

- Nihon Kohden Corporation

- Dozee

- QT Medical

第7章 市場機会と将来の動向

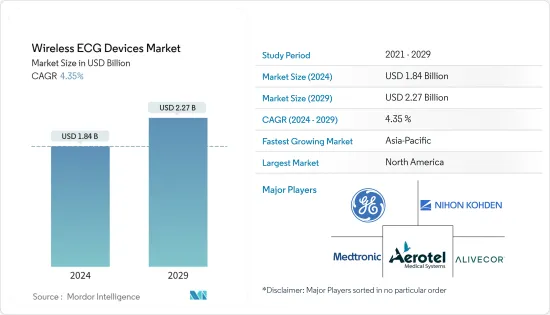

The Wireless ECG Devices Market size is estimated at USD 1.84 billion in 2024, and is expected to reach USD 2.27 billion by 2029, growing at a CAGR of 4.35% during the forecast period (2024-2029).

Over the pandemic period, COVID-19 had a significant impact on the wireless ECG device industry. As per the article published by the European Heart Journal in January 2021, home ECG monitoring with the help of smartphones in non-hospitalized COVID-19 patients was able to identify disease-related cardiac complications and the presence of ECG alterations. Moreover, the COVID-19 pandemic increased the demand for telehealth and virtual solutions due to the strict lockdown regulations imposed at the initial stages of the pandemic. Since there was limited patient access to cardiac care facilities during the pandemic, these remote monitoring systems were immensely popular across the world. Hence, COVID-19 had a significant impact on the wireless ECG device market. In addition, the demand for wireless ECG devices is expected to remain intact during the post-pandemic period.

The major factors driving the growth of the wireless ECG devices market include the growing geriatric population, the increasing incidence of cardiovascular diseases, and technological advancements in remote monitoring technologies. For instance, the British Heart Foundation (BHF) data published in January 2022 reported that in 2021, the most common heart conditions affected globally were coronary (ischemic) heart disease (global prevalence estimated at 200 million), peripheral arterial (vascular) disease (110 million), stroke (100 million), and atrial fibrillation (60 million). The report also mentioned that the prevalence of heart and circulatory diseases in North America was 46 million, in Europe it was 99 million, in Africa it was 58 million, in South America it was 32 million, and in Asia and Australia it was 310 million. Thus, the high number of cardiovascular diseases in the world's population is likely to increase the demand for wireless ECG devices because they are more accurate and easier to use. This will help the market grow.

Additionally, the report published by the UN in 2022 mentioned that the share of the global population aged 65 years or older is projected to rise from 10% in 2022 to 16% in 2050. Over the next few years, the growth of the market is also expected to be helped by the growing number of older people who are more likely to get heart diseases.

Furthermore, major players are adopting various strategies to grow their presence in the market, which may further fuel market growth. For instance, in January 2022, Philips launched the 12-lead electrocardiogram solution for use in decentralized clinical trials. The clinical-grade solution is the most advanced patient-centered ECG in the company's line of cardiac monitoring products. Its data readings are similar to those of ECGs used in clinical settings. Thus, the growth of the market is likely to be helped by the growing number of older people, the high number of people with cardiovascular diseases, and the regular release of new products by key market players.

But the growth of the market is likely to be slowed by complicated reimbursement policies for cardiovascular diseases and errors in precision reporting.

Wireless ECG Devices Market Trends

The Monitoring Systems Segment is Expected to be the Fastest Growing Segment During the Forecast Period

The continuous cardiovascular monitoring ECG systems segment is expected to grow over the forecast period, due to the increasing incidence of cardiovascular diseases and a growing geriatric population, which is likely to increase the need for continuous cardiovascular monitoring of patients' hearts during their daily routines. For instance, the MDPI Journal research article published in September 2021 reported that the worldwide prevalence of peripheral arterial disease (PAD) is estimated to be 3-12%, affecting nearly 27 million people in America and Europe. The same source also reported that in Europe, the prevalence of PAD is estimated at around 17.8% between the ages of 45 and 55. Such a high prevalence of cardiovascular diseases is expected to contribute to the growing demand for continuous cardiovascular monitoring ECG systems, thereby fueling segment growth.

Increasing awareness regarding the early detection and management of cardiovascular diseases is augmenting the demand for continuous cardiovascular ECG monitoring devices. For instance, the World Heart Federation (WHF) celebrates World Heart Day on September 29 every year. WHF has planned a campaign to raise awareness of heart health in September 2022.Over 90 countries take part in this international observance every year. As a result, World Heart Day has proven to be an effective means for disseminating information about cardiovascular disorders.

The innovative product launches necessary to meet the growing demand for continuous cardiovascular monitoring ECG systems are also expected to boost segment growth. For instance, in April 2022, Biotricity launched its US FDA-cleared, wireless wearable cardiac monitoring device, Biotres. The product was available for pre-order to physicians, medical offices, hospitals, and individual users as of late February 2022.

North America is Expected to Witness a Growth in Wireless ECG Devices Market Over the Forecast Period

North America holds a major share of the wireless ECG devices market, and it is expected to show a similar trend over the forecast period. Factors such as the growing geriatric population and increasing incidence of cardiovascular diseases fuel the market growth in the studied region. For instance, as per the 2022 Heart Disease and Stroke Statistics Update Fact Sheet, approximately every 40 seconds, a person in the United States is anticipated to have a myocardial infarction. Likewise, the CDC updated in September 2021 reported that approximately 6.5 million people aged 40 and older in the United States have peripheral arterial disease. Also, as per the February 2022 report from the Heart and Stroke Foundation of Canada, 750,000 people are living with heart failure, and 100,000 people are diagnosed with heart failure each year in the country.

Furthermore, the presence of key players and frequent product approvals, launches, and developments are expected to contribute to the growth of the market in this region. For instance, in October 2022, QT Medical received FDA clearance for PCA 500, aresting 12-lead electrocardiogram for use in pediatric patients. This clearance expanded its indication for use to all pediatric populations, including newborns, infants, children and adolescents.

Therefore, the above mentioned factors such as growing geriatric population and increasing incidence of cardiovascular diseases, key product launches are expected to contribute to the growth of the market in this region.

Wireless ECG Devices Industry Overview

The wireless ECG devices market is a moderately consolidated market, owing to the presence of a few major players and smaller players in the market. The market players are focusing on R&D to develop technologically advanced products for the market. The major market players are Nihon Kohden Corporation, Medtronic, General Electric Company (GE Healthcare), Aerotel Medical Systems, and AliveCor Inc., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Geriatric Population and Increasing Incidence of Cardiovascular Diseases

- 4.2.2 Declining Cost of Wireless Technologies

- 4.2.3 Technological Advancements in Remote Monitoring Technologies

- 4.3 Market Restraints

- 4.3.1 Complex Reimbursement Policies Regarding Cardiovascular Diseases (CVD)

- 4.3.2 Inaccuracies in Precision Reporting

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By Product Type

- 5.1.1 Monitoring ECG Systems

- 5.1.1.1 Remote Data Monitoring

- 5.1.1.2 Event Monitoring

- 5.1.1.3 Continuous Cardiovascular Monitoring Systems

- 5.1.2 Diagnostic ECG Systems

- 5.1.2.1 Rest ECG Systems

- 5.1.2.2 Stress ECG Systems

- 5.1.2.3 Holter ECG Systems

- 5.1.1 Monitoring ECG Systems

- 5.2 By End User

- 5.2.1 Hospital

- 5.2.2 Home-based User

- 5.2.3 Other End Users

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Aerotel Medical Systems Ltd

- 6.1.2 AliveCor Inc.

- 6.1.3 BPL Medical Technologies

- 6.1.4 Bittium

- 6.1.5 CardioComm Solutions Inc.

- 6.1.6 GE Healthcare

- 6.1.7 iRhythm Technologies Inc.

- 6.1.8 MediBioSense Ltd

- 6.1.9 Medtronic PLC

- 6.1.10 Nihon Kohden Corporation

- 6.1.11 Dozee

- 6.1.12 QT Medical