|

市場調査レポート

商品コード

1937398

種子:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 種子:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

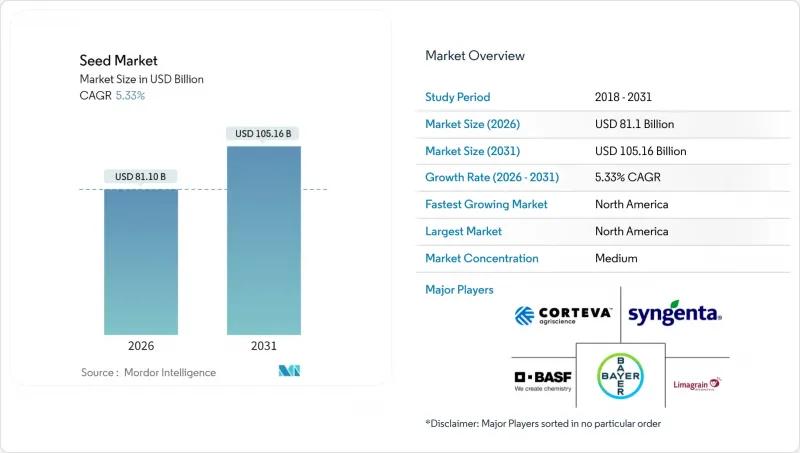

2026年の種子市場規模は811億米ドルと推定され、2025年の770億米ドルから成長が見込まれます。

2031年には1,051億6,000万米ドルに達し、2026年から2031年にかけてCAGR5.33%で拡大する見通しです。

堅調な成長は、収量増加、気候変動への耐性強化、投入コスト削減を実現する高性能種子品種の喫緊の必要性を反映しています。認定ハイブリッド種へのアクセス拡大、デジタル育種ツールの導入加速、政府支援プログラムが相まって需要を牽引しています。トウモロコシ、米、その他の主食作物におけるハイブリッド種の優位性が数量を支える一方、食習慣の変化に伴い野菜や特殊作物がより高い利益率をもたらしています。保護栽培、垂直農場、気候制御型温室の拡大は、特にアジア太平洋地域の都市部において、世界の生産戦略をさらに再構築しています。一方、遺伝子編集種子に関する規制の明確化とAIを活用した表現型解析は、イノベーションサイクルを短縮し、新たな形質ポートフォリオの可能性を開いています。

世界の種子市場の動向と洞察

作物の収量向上に向けたハイブリッド種および遺伝子組み換え種子の採用拡大

ハイブリッド種の普及率は、米国トウモロコシでは既に90%を超え、インド米でも70%近くに達しており、農家が異種交配効果による15~30%の収量向上を圧倒的に認識していることを裏付けています。かつて雑草・害虫防除に重点を置いていた遺伝子組み換えスタックは、現在では耐乾性、アミノ酸バランスの改善、長期保存性を組み合わせ、近代ハイブリッドの農学的・商業的魅力を総合的に高めています。アルゼンチンとブラジルにおける耐乾性トウモロコシの最近の承認は、主要輸出経済国の規制当局が気候適応形質に対してより寛容になりつつあることを示しており、民間育種家が多形質パイプラインの開発を加速させることを後押ししています。ハイブリッド種子は毎シーズン購入する必要があるため、採用率の上昇は認定種子の更新率も押し上げ、これが育種および流通インフラへの資本流入を促進します。生産性の向上、安定した市場アクセス、形質革新という好循環により、ハイブリッド種子と遺伝子組み換え種子は商業栽培システムの核として確固たる地位を維持しています。遺伝子編集技術に関する政策論議が未解決の地域においても、ハイブリッド研究への継続的な投資が堅調な成長基盤を確かなものにしています。

種子コーティング・処理技術における進歩

農家は、高コストな複数回の圃場散布を行う代わりに、種子レベルでの投資保護を強化しており、これが世界の種子処理剤収益を持続的な二桁成長に押し上げています。現代のコーティング技術は、化学殺菌剤と生物剤、微量栄養素、ポリマーマトリックスを組み合わせ、苗が最も脆弱な時期に的を絞った保護と栄養を供給します。徐放性層は数週間にわたり有効成分を放出するため、環境への流出を低減し、多くの輸出市場を形作る厳格な残留基準を満たします。バイエル社とコルテバ社は2024年、それぞれ独自の細菌・菌類を活用した微生物プラットフォームを拡大しました。これらは養分吸収を促進し、生育初期のストレスを軽減します。これらの生物剤は化学活性成分と相乗的に作用し、総投入量を増加させることなく生育確立を促進する混合製剤を生み出します。サステナビリティ報告の重要性が高まる中、流通業者は種子処理を、高収量ポテンシャルを維持しつつ広大な農地における農薬使用量を削減する費用対効果の高い手段として推進しています。

厳格な生物安全規制と複数年に及ぶ承認プロセス

単一の遺伝子組換え形質を構想から国際承認まで導くには、通常1億5,000万米ドルと7年を要します。これにより、収量飛躍を最も必要とする市場から中小の革新企業が締め出されています。欧州連合(EU)は新規栽培を制限する予防的アプローチを継続し、中国では進化するガイドラインが依然としてパイロット導入規模を超えた展開を制限しています。こうした膨大なデータ要件とパブリックコメントのサイクルは開発予算を膨らませ、世界同時発売を遅らせ、企業に段階的な導入を余儀なくさせています。この時間的遅延は、農家が気候変動に対応した遺伝子技術を利用できる機会を阻害し、気象リスクや害虫の進化への曝露期間を長期化させます。規制の分断化は重複した野外試験や書類作業を招き、追加的な形質発見に充てられるべき研究資金を希薄化させています。より大きな整合性が生まれるまでは、資金力のある企業でさえ、より迅速で科学に基づく承認プロセスを有する地域を優先せざるを得ません。

セグメント分析

ハイブリッド種子は2025年における種子市場収益の72.65%を占め、2031年までCAGR5.47%で拡大が見込まれます。この優位性は、収量を最大30%向上させる雑種強勢効果に起因し、確実な収益を見込めるため農家が種子コストの上昇を吸収する要因となっています。遺伝子組み換え規制が厳しい市場においても、マーカー支援選抜やゲノム予測による病害耐性選別が進む非遺伝子組み換えハイブリッドの採用は堅調です。デジタルフェノタイピング技術は、画像データとゲノムスコアの連携により開発期間を短縮し、単位コストを低減することで、ハイブリッド開発サイクルをさらに加速させています。

南米および北米では、耐乾性トウモロコシや害虫抵抗性大豆の承認が急速に拡大し、遺伝子組み換えハイブリッドが最も速いペースで普及しています。窒素利用効率やバイオフォティフィケーション(栄養強化)といった複合形質が規制上の障壁をクリアするにつれ、遺伝子組み換えハイブリッドの種子市場規模は着実に拡大すると予測されます。クラスター化規則的間隔短回文反復配列(CRISPR)編集技術は、政策上の不確実性を依然として抱えつつも、より高い精度と連鎖引きずりの低減を約束し、従来の交雑を超えた育種ツールボックスの幅を広げています。

本種子市場レポートは、育種技術(ハイブリッド、開放受粉品種、ハイブリッド派生品種)、栽培形態(露地栽培と保護栽培)、作物タイプ(作付作物と野菜)、地域(北米、欧州、アジア太平洋、南米など)ごとに分類されています。市場予測は、金額(米ドル)および数量(メトリックトン)で提供されます。

地域別分析

北米は2025年に種子収益の34.86%を占め最大のシェアを維持し、2031年までCAGR6.21%で最も速い拡大を記録すると予測されています。堅牢なバイオテクノロジー基盤と広範なデジタル農業ツールにより、生産者は他地域よりも迅速に新たなハイブリッド品種を導入できます。米国では大規模商品農場が複合形質トウモロコシ・大豆遺伝資源への投資を継続し、カナダでは高油分キャノーラや耐寒性小麦品種の開発が進められています。メキシコでは輸出回廊沿いの温室拡大に伴い野菜種子需要が増加。肥料・燃料コストの変動があるもの、これらの相乗効果により地域全体は堅調な成長軌道を維持しています。

欧州では、オランダ、フランス、スペインの特産野菜拠点が、高級小売基準を満たす風味と保存性の向上に注力し、着実な勢いを維持しております。遺伝子組み換え作物に対する厳格な規制により、育種予算はマーカー支援型病害抵抗性や欧州グリーンディールに沿った低投入特性へとシフトしております。有機農地の拡大は、非合成処理や在来品種への関心を広げ、ニッチサプライヤーの参入余地を生み出しております。英国のブレグジット後の規制変化は、地域特化型形質ポートフォリオのさらなる展開機会を生み出しています。大陸部では干ばつや熱波の頻発化が進む中、気候変動への耐性は依然として最重要課題です。

アジア太平洋地域は、中国とインドの広大な作付面積により、収益貢献度で依然として第2位を維持しています。ただし成長率は現在、アメリカ大陸に後れを取っています。インドの政府補助金と東南アジアの収量重視型ハイブリッド米が、認定種子の更新率を着実に押し上げています。南米は、ブラジルにおける大豆・トウモロコシの継続的な作付拡大と、アルゼンチンでの耐乾性ハイブリッド品種に対する迅速な規制承認の恩恵を受けています。中東・アフリカ地域は、灌漑プロジェクトや農家による改良品種へのアクセス向上を図る補助金プログラムに起因する長期的な成長余地を有しています。これらの地域は総合的に、世界の種子バリューチェーンに規模の拡大、多様化、リスク分散の深みをもたらしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3か月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

- 調査手法

第2章 エグゼクティブサマリー主要な調査結果

第3章 レポート提供

第4章 主要な業界動向

- 作付面積

- 畑作作物

- 野菜

- 最も人気のある形質

- アルファルファおよび飼料用トウモロコシ

- キャベツ、カボチャ、ズッキーニ

- 綿花、キャノーラ、ナタネ・カラシナ

- 米とトウモロコシ

- 大豆・ヒマワリ

- トマト・キュウリ

- 小麦・ソルガム

- 育種技術

- 畑作作物・野菜

- 規制の枠組み

- バリューチェーンと流通チャネル分析

- 市場促進要因

- 作物の収量向上に向けたハイブリッド種および遺伝子組換え種子品種の採用拡大

- 種子コーティングおよび処理ソリューションにおける技術的進歩

- 政府プログラムによる認定種子置換率の促進

- 人口増加と食習慣の変化による高付加価値作物への需要拡大

- AIを活用したデジタルフェノタイピングによる育種サイクルの短縮

- 気候変動に強い種子特性がインパクト資本を惹きつける

- 市場抑制要因

- 厳格なバイオセーフティ規制と複数年にわたる承認プロセス

- 種子価格の上昇が小規模農家へのアクセスを制限

- 新興市場における農家主導の種子保存運動

- 欧州連合(EU)と中国におけるクラスター化規則的間隔短回文反復配列(CRISPR)種子政策の不確実性

第5章 市場規模と成長予測(数量と金額)

- 育種技術別

- ハイブリッド

- 非遺伝子組み換えハイブリッド品種

- トランスジェニックハイブリッド

- 除草剤耐性ハイブリッド品種

- 害虫抵抗性ハイブリッド品種

- その他の特性

- 自然交配品種および交配品種

- ハイブリッド

- 栽培メカニズム別

- オープンフィールド

- 保護栽培

- 作物タイプ別

- 畑作作物

- 繊維作物

- 綿

- その他の繊維作物

- 飼料作物

- アルファルファ

- 飼料用トウモロコシ

- 飼料用ソルガム

- その他の飼料作物

- 穀物・穀類

- トウモロコシ

- 米

- ソルガム

- 小麦

- その他の穀物・穀類

- 油糧種子

- キャノーラ、ナタネ、マスタード

- 大豆

- ひまわり

- その他の油糧種子

- 豆類

- 繊維作物

- 野菜

- アブラナ科

- キャベツ

- カリフラワーとブロッコリー

- その他のアブラナ科野菜

- ウリ科

- キュウリとガーキン

- カボチャとウリ類

- その他のウリ科作物

- 根菜類と球根類

- ニンニク

- オニオン

- ジャガイモ

- その他の根菜類・球根類

- ナス科

- チリ

- ナス

- トマト

- その他のナス科

- 分類されていない野菜

- アスパラガス

- レタス

- キャロット

- オクラ

- エンドウ豆

- ほうれん草

- その他の分類されない野菜

- アブラナ科

- 畑作作物

- 地域別

- 北米

- カナダ

- メキシコ

- 米国

- その他北米地域

- 欧州

- フランス

- ドイツ

- イタリア

- オランダ

- ポーランド

- ルーマニア

- ロシア

- スペイン

- トルコ

- ウクライナ

- 英国

- その他欧州地域

- アジア太平洋地域

- オーストラリア

- バングラデシュ

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- その他南米

- 中東・アフリカ

- イラン

- サウジアラビア

- エジプト

- エチオピア

- ガーナ

- ケニア

- ナイジェリア

- 南アフリカ

- タンザニア

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 主要な戦略的動きs

- 市場シェア分析

- 企業概要

- 企業プロファイル

- Bayer AG

- Corteva, Inc.

- Syngenta Group

- BASF SE

- Groupe Limagrain Holding

- KWS SAAT SE & Co. KGaA

- Sakata Seed Corporation

- Rijk Zwaan Zaadteelt en Zaadhandel B.V.

- Takii & Co., Ltd.

- Enza Zaden Beheer B.V.

- DLF Seeds A/S

- UPL Limited

- East-West Seed International B.V.

- Hunan Haili Longping Hi-Tech Seed Co., Ltd.

- Bejo Zaden B.V.