|

市場調査レポート

商品コード

1693464

アジア太平洋地域の種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Asia-Pacific Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アジア太平洋地域の種子:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 541 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

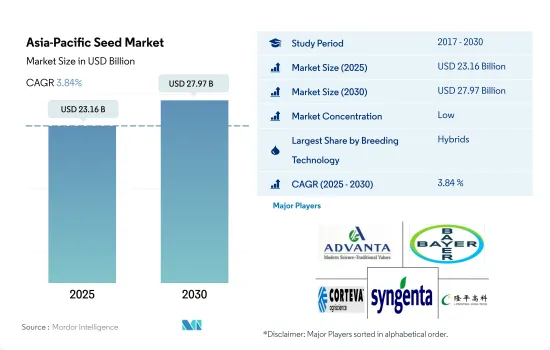

アジア太平洋地域の種子市場規模は、2025年には231億6,000万米ドルと推定され、2030年には279億7,000万米ドルに達すると予測され、予測期間中(2025年~2030年)のCAGRは3.84%で成長する見込みです。

ハイブリッド種子は高い収量と生物的・生物的ストレスへの耐性を持つことからアジア太平洋地域の種子市場を独占

- アジア太平洋地域では、ハイブリッド種子が種子市場を独占し、2022年には金額ベースで70.2%のシェアを占めました。ハイブリッド種子市場全体の金額のうち、連作作物のシェアは87.1%を占め、野菜は2022年に12.9%を占める。

- ハイブリッド分野が大きなシェアを占めているのは、高い生産性、幅広い適応性、生物学的・生物学的ストレスに対する高い耐性があるためです。綿花では、ハイブリッドは従来品種よりも収量が50%多いです。ハイブリッドの幅広い適応性は、主に環境の変動に対する高い緩衝能力によるものです。したがって、ハイブリッド種子の需要は予測期間中に増加すると予想されます。

- 2022年には、連作作物のハイブリッドのうち、遺伝子組み換えハイブリッドが市場シェアの24.2%を占めました。これは、より優れた収量を生み出す能力に起因します。非遺伝子組み換えハイブリッドは市場金額の75.8%を占めました。

- ハイブリッドの中では、昆虫抵抗性の遺伝子組み換えハイブリッドがトランスジェニック種子市場を独占し、2022年の市場シェア値の84.4%を占める。この地域で栽培が認められている耐虫性形質を持つ作物は、トウモロコシ、綿花、コメです。

- 開放受粉品種とハイブリッド派生品種は、金額ベースでアジア太平洋地域の2022年の市場シェア29.8%を占めました。インドのような国では、政府がOPVの利用拡大を支援するため、国際的な種子会社が請求できる価格に上限を設けることで、地元で育成された開放受粉品種を積極的に推進しています。

- ハイブリッドや改良型OPVの利用可能性が高まった結果、収量が向上し、手ごろな価格で種子を入手できるようになるなど、多くの利点が生まれました。これらの要因が、予測期間中のアジア太平洋地域の種子市場の成長を促進すると推定されます。

同地域の農業を支援する様々な政府の取り組みや制度、ハイブリッド種子の需要拡大が市場を牽引

- アジア太平洋地域では、中国が種子市場を独占し、金額ベースで市場の54.4%を占め、次いでインドが15.7%、日本が5.5%、パキスタンが3.8%、インドネシアが3.7%となっている(2022年)。

- 中国は、多国籍種子企業の国内市場への参入を奨励しています。新しい開発コンセプトや技術を国内に持ち込み、新技術や増殖方法を普及させ、産業合理化を推進するためです。こうした要因により、予測期間中の中国の種子市場のCAGRは2.9%になると予想されます。

- インドでは、種子産業の発展を支援するため、インド政府が種子村プログラム、油糧種子統合スキーム、インド北東部への種子輸送補助金、ハイブリッド米種子生産など、生産、流通、輸送のコストを支援する多くのスキームを立ち上げました。これらの要因は、予測期間中、インドの種子市場をCAGR 5.5%で牽引すると予想されます。

- 日本では、都市農業が農業の新しい動向として開発されています。新鮮な野菜の需要は、全国の健康志向の消費者により拍車がかかっています。農地が制約に直面する中、国産野菜の不足に対処するため、室内農業や垂直農法などの都市農業が事業規模を拡大しています。

- オーストラリア市場は、予測期間中にCAGR 6.0%を記録し、この地域で最も急成長している種子市場になると予想されます。これは主に、同国における栽培面積の拡大と需要の増加に起因しています。

- 同地域の農業を支援する政府の様々な取り組みが、予測期間中の市場を牽引すると予想されます。

アジア太平洋地域の種子市場動向

同地域における連作作物需要の増加は、連作作物の高い輸出ポテンシャルと相まって、連作作物栽培面積を牽引しています。

- アジア太平洋地域では、2022年の総栽培面積の95.0%以上を連作作物が占めています。この地域で栽培されている主な連作作物には、コメ、小麦、トウモロコシ、ヒマワリ、大豆、その他の穀物・穀類が含まれます。2022年には、穀物・穀類が約68.0%と大きなシェアを占め、連作作物の栽培面積を独占します。穀物・穀類のこのような支配的地位は、その地域的な生産高によるものです。

- 2022年の穀物・穀類の作付面積は6,740万ヘクタールで、このうちアジアではコメが大きなシェアを占めています。これは、夏期とモンスーン期の高温と豊富な降雨が、アジアの稲作に理想的な条件を提供しているためです。ミレットは主にインド、中国、パキスタンの地域で栽培されています。インドは世界有数の雑穀生産国です。

- *列作物全体の作付面積は、2017年から2022年の間に約8.9%増加しました。これは、この地域における連作作物に対する需要の高まりによるもので、米や小麦などの作物は、この地域のほとんどの国で主食作物となっています。さらに、中国やインドなどの国々では、政府がインドの国家食糧安全保障ミッション(NFSM)など様々な制度を通じて農業を推進しています。

- 中国とインドは、この地域の主要な連作作物輸出国です。2022年、インドは同年に約2,220万トンのコメを輸出しました。同地域の米栽培面積は全体として約6.7%増加し、予測期間終了時には1億5,420万ヘクタールに達すると予想されます。これは、米の需要拡大と輸出ポテンシャルの高さによるものです。連作作物に対する需要の高まりが、予測期間中の作付面積を牽引すると予想されます。

畜産における飼料需要の増加は、耐病性、幅広い適応性、早熟の特徴を持つハイブリッド飼料種子の使用を促進しています。

- アルファルファと飼料用トウモロコシは、消化率が高く高タンパク質であるなど、家畜の飼育に有益であるため、主要な飼料作物です。また、農家は品質を犠牲にすることなく、より高い収量を達成することができます。アルファルファは、天候の変化、早熟に対する需要の高さ、異なる投入資材の使用を最小限に抑えるために単一製品でリグニン含有量が低いことから、適応性の広さが最も採用された形質でした。

- アルファルファの最も一般的で有害な菌類病害は、フザリウムと褐斑病です。これらは植物の生産性を30%以上低下させる。そのため、アルファルファ生産者がより高い生産性を達成するためには、耐病性形質を持つアルファルファ品種への需要が高まっています。さらに、低リグニン形質のアルファルファは消化性が高く、収量が15~20%増加するため、日本では低リグニン形質のアルファルファが栽培されています。したがって、低リグニン形質を持つアルファルファの需要は、予測期間中にこの地域で増加すると予想されます。

- 高収量ポテンシャル、干ばつ耐性、耐病性、早熟性、宿根耐性形質を持つフォレージコーンは需要が高いです。これらの形質のうち、早熟形質は畜産業で高い需要があるため、最大のシェアを占めています。この需要に応えるため、生産者はオフシーズンに作物を栽培し、通常の栽培よりも栽培期間を1~2週間短縮します。例えば、Land O'Lakes社は、干ばつ耐性と早熟の特徴を持つ約44の製品を提供しています。

- 病害による損失の増加を防ぎ、短期間で生産性を向上させるため、耐病性、早生、干ばつ耐性などの形質を持つ種子が市場の成長を後押ししています。

アジア太平洋地域の種子産業の概要

アジア太平洋地域の種子市場は細分化されており、上位5社で20.27%を占めています。この市場の主要企業は以下の通りです。 Advanta Seeds-UPL, Bayer AG, Corteva Agriscience, Syngenta Group and Yuan Longping High-Tech Agriculture(アルファベット順)

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 耕作面積

- 耕作作物

- 野菜

- 最も人気のある品種

- アルファルファ&飼料用トウモロコシ

- キャベツ&レタス

- 米&トウモロコシ

- トマト&チリ

- 小麦&綿花

- 育種技術

- 畑作物&野菜

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 育種技術

- ハイブリッド

- 非遺伝子組み換え雑種

- 遺伝子組み換え雑種

- 除草剤耐性雑種

- 昆虫抵抗性雑種

- その他の形質

- 開放受粉品種とハイブリッド派生品種

- ハイブリッド

- 栽培メカニズム

- 露地栽培

- 保護栽培

- 作物タイプ

- 畑作物

- 繊維作物

- 綿花

- その他の繊維作物

- 飼料作物

- アルファルファ

- 飼料用トウモロコシ

- 飼料用ソルガム

- その他の飼料作物

- 穀物・穀類

- トウモロコシ

- 米

- ソルガム

- 小麦

- その他の穀物

- 油糧種子

- キャノーラ、菜種、マスタード

- 大豆

- ひまわり

- その他の油糧種子

- 豆類

- 豆類

- 野菜

- アブラナ

- キャベツ

- ニンジン

- カリフラワー&ブロッコリー

- その他のアブラナ

- ウリ科

- キュウリ・ガーキン

- カボチャ・スカッシュ

- その他ウリ科

- 根菜・球根

- ニンニク

- タマネギ

- ジャガイモ

- その他の根菜類

- ナス科

- 唐辛子

- ナス科

- トマト

- その他ナス科

- 分類されていない野菜

- アスパラガス

- レタス

- オクラ

- エンドウ豆

- ほうれん草

- その他分類されていない野菜

- 畑作物

- 生産国

- オーストラリア

- バングラデシュ

- 中国

- インド

- インドネシア

- 日本

- ミャンマー

- パキスタン

- フィリピン

- タイ

- ベトナム

- その他アジア太平洋地域

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Advanta Seeds-UPL

- BASF SE

- Bayer AG

- Bejo Zaden BV

- Corteva Agriscience

- East-West Seed

- Groupe Limagrain

- Rijk Zwaan Zaadteelt en Zaadhandel BV

- Syngenta Group

- Yuan Longping High-Tech Agriculture Co. Ltd

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク

- 世界のバリューチェーン分析

- 世界市場規模とDRO

- 情報源と参考文献

- 図表リスト

- 主要洞察

- データパック

- 用語集

The Asia-Pacific Seed Market size is estimated at 23.16 billion USD in 2025, and is expected to reach 27.97 billion USD by 2030, growing at a CAGR of 3.84% during the forecast period (2025-2030).

Hybrids dominate the Asia-Pacific seed market due to their ability to produce higher yields and resistance to biotic and abiotic stresses

- In Asia-Pacific, hybrid seeds dominated the seed market, with a share of 70.2% in 2022 in terms of value. Out of the total hybrid seed market value, row crops accounted for an 87.1% share, whereas vegetables accounted for 12.9% in 2022.

- The hybrid segment has a major share because of higher productivity, wider adaptability, and a high degree of resistance to biotic and abiotic stresses. In cotton, hybrids give 50% more yield than conventional varieties. The wider adaptability of hybrids is mainly due to their high buffering capacity to environmental fluctuations. Thus, the demand for hybrid seeds is expected to increase during the forecast period.

- In 2022, among the row crop hybrids, transgenic hybrids accounted for 24.2% of the market share. This is attributed to their ability to produce better yields. Non-transgenic hybrids accounted for 75.8% of the market value.

- Among hybrids, insect-resistant transgenic hybrids dominate the transgenic seed market, accounting for a share of 84.4% of the market share value in 2022. Crops with insect-resistant traits approved for cultivation in the region are corn, cotton, and rice.

- Open-pollinated varieties and hybrid derivatives held a market share of 29.8% in 2022 in Asia-Pacific in terms of value. In countries such as India, the government is actively promoting locally bred open-pollinated varieties by capping the prices that international seed companies can charge to help increase the usage of OPVs.

- The increased availability of hybrids and improved OPVs resulted in many advantages, such as yield improvement and availability of seeds at an affordable price. These factors are estimated to drive the growth of the Asia-Pacific seed market during the forecast period.

The various government initiatives and schemes to support agriculture in the region and the growing demand for hybrids are driving the market

- In Asia-Pacific, China dominated the seed market, which accounted for 54.4% of the market in terms of value, followed by India at 15.7%, Japan at 5.5%, Pakistan at 3.8%, and Indonesia at 3.7% in 2022.

- China encourages multinational seed companies to enter the domestic market as they bring new development concepts and technology into the country, spread new technologies and propagation methods, and promote industrial rationalization. These factors are anticipated to drive the Chinese seed market at a CAGR of 2.9% during the forecast period.

- In India, to support the development of the seed industry, the Government of India launched many schemes, such as the Seed Village Program, Integrated Scheme on Oilseeds, transport subsidy on the movement of seeds to the North Eastern States in India, and hybrid rice seed production, which support the cost of production, distribution, and transportation. These factors are anticipated to drive the Indian seed market at a CAGR of 5.5% during the forecast period.

- In Japan, urban agriculture is developing as a new trend in agriculture. The demand for fresh vegetables is spurred by health-conscious consumers across the country. As agricultural land faces constraints, urban agriculture, such as indoor farming and vertical farming practices, has been scaling up operations to address the shortage of domestically grown vegetables.

- The Australian market is anticipated to be the fastest-growing seed market in the region, registering a CAGR of 6.0% during the forecast period. This is mainly attributed to the growing cultivation area in the country and the growing demand.

- The various government initiatives supporting agriculture in the region are anticipated to drive the market during the forecast period.

Asia-Pacific Seed Market Trends

The increasing demand for row crops in the region, combined with the high export potential of row crops, is driving the row crop area

- In the Asia-Pacific region, row crops dominated the total cultivated acreage in 2022, which accounted for more than 95.0% of the total cultivated area in 2022. The primary row crops cultivated in the region include rice, wheat, corn, sunflower, soybean, and other grains and cereals. In 2022, grains and cereals dominated the row crop acreage with a significant share of about 68.0%. This domination of grains and cereals is due to their substantial regional production output.

- The area under grains cereals accounted for 67.4 million hectares in 2022, in which rice held the major share in acreage in Asia. This is because high temperatures and abundant rainfall during the summer and monsoon seasons have provided ideal conditions for rice growing in Asia. Millets are mostly grown in the regions of India, China, and Pakistan. India is the world's leading producer of millet.

- * The overall row crop acreage increased by about 8.9% between 2017 and 2022. This is due to the growing demand for row crops in the region, and crops such as rice and wheat are staple food crops in most countries in the region. Moreover, in countries such as China and India, governments promote agriculture through various schemes such as the National Food Security Mission (NFSM) in India.

- China and India are the major row crop exporting countries in the region. In 2022, India exported about 22.2 million tons of rice during the same year. The overall rice cultivated area in the region is anticipated to increase by about 6.7% and reach 154.2 million hectares by the end of the forecast period. This is due to the growing demand and the high export potential of rice. The growing demand for row crops is anticipated to drive the acreage during the forecast period.

Increasing demand for fodder in livestock farming is driving the usage of hybrid forage seeds having disease resistant, wider adaptability, and early maturity traits

- Alfalfa and forage corn are the major forage crops because of their benefits to livestock rearing, such as more digestibility and high protein. They also allow farmers to attain greater yields without sacrificing quality. Wider adaptability for alfalfa was the largest adopted trait as there have been weather changes, high demand for early maturity, and low lignin content in a single product to minimize the usage of different inputs.

- The most common and harmful fungal diseases of alfalfa are fusarium and brown spot. They can reduce the productivity of plants by 30% or more. Therefore, the demand for alfalfa varieties with disease-resistant traits increases for alfalfa growers to achieve higher productivity. Additionally, alfalfa with low lignin traits is cultivated in Japan as the low-lignin trait alfalfa is highly digestible, and it offers a 15-20% increase in yield. Therefore, the demand for alfalfa with low lignin traits is expected to increase in the region during the forecast period.

- Forage corn with high yield potential, drought tolerance, disease tolerance, early maturity, and lodging tolerance traits are in high demand. Among these traits, the early maturity trait had the largest share as it has a high demand in the livestock industry. To meet this demand, the growers cultivate the crop in the off-season and reduce the cultivating period to normal cultivation by 1-2 weeks than normal cultivation. For instance, Land O' Lakes provides about 44 products with drought tolerance and early maturity traits.

- To prevent the increasing losses from diseases and increase productivity in a shorter period, the seeds with traits such as disease resistance, early maturity, and drought tolerance are fueling the market's growth.

Asia-Pacific Seed Industry Overview

The Asia-Pacific Seed Market is fragmented, with the top five companies occupying 20.27%. The major players in this market are Advanta Seeds - UPL, Bayer AG, Corteva Agriscience, Syngenta Group and Yuan Longping High-Tech Agriculture Co. Ltd (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Row Crops

- 4.1.2 Vegetables

- 4.2 Most Popular Traits

- 4.2.1 Alfalfa & Forage Corn

- 4.2.2 Cabbage & Lettuce

- 4.2.3 Rice & Corn

- 4.2.4 Tomato & Chilli

- 4.2.5 Wheat & Cotton

- 4.3 Breeding Techniques

- 4.3.1 Row Crops & Vegetables

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Insect Resistant Hybrids

- 5.1.1.2.3 Other Traits

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Cultivation Mechanism

- 5.2.1 Open Field

- 5.2.2 Protected Cultivation

- 5.3 Crop Type

- 5.3.1 Row Crops

- 5.3.1.1 Fiber Crops

- 5.3.1.1.1 Cotton

- 5.3.1.1.2 Other Fiber Crops

- 5.3.1.2 Forage Crops

- 5.3.1.2.1 Alfalfa

- 5.3.1.2.2 Forage Corn

- 5.3.1.2.3 Forage Sorghum

- 5.3.1.2.4 Other Forage Crops

- 5.3.1.3 Grains & Cereals

- 5.3.1.3.1 Corn

- 5.3.1.3.2 Rice

- 5.3.1.3.3 Sorghum

- 5.3.1.3.4 Wheat

- 5.3.1.3.5 Other Grains & Cereals

- 5.3.1.4 Oilseeds

- 5.3.1.4.1 Canola, Rapeseed & Mustard

- 5.3.1.4.2 Soybean

- 5.3.1.4.3 Sunflower

- 5.3.1.4.4 Other Oilseeds

- 5.3.1.5 Pulses

- 5.3.1.5.1 Pulses

- 5.3.2 Vegetables

- 5.3.2.1 Brassicas

- 5.3.2.1.1 Cabbage

- 5.3.2.1.2 Carrot

- 5.3.2.1.3 Cauliflower & Broccoli

- 5.3.2.1.4 Other Brassicas

- 5.3.2.2 Cucurbits

- 5.3.2.2.1 Cucumber & Gherkin

- 5.3.2.2.2 Pumpkin & Squash

- 5.3.2.2.3 Other Cucurbits

- 5.3.2.3 Roots & Bulbs

- 5.3.2.3.1 Garlic

- 5.3.2.3.2 Onion

- 5.3.2.3.3 Potato

- 5.3.2.3.4 Other Roots & Bulbs

- 5.3.2.4 Solanaceae

- 5.3.2.4.1 Chilli

- 5.3.2.4.2 Eggplant

- 5.3.2.4.3 Tomato

- 5.3.2.4.4 Other Solanaceae

- 5.3.2.5 Unclassified Vegetables

- 5.3.2.5.1 Asparagus

- 5.3.2.5.2 Lettuce

- 5.3.2.5.3 Okra

- 5.3.2.5.4 Peas

- 5.3.2.5.5 Spinach

- 5.3.2.5.6 Other Unclassified Vegetables

- 5.3.1 Row Crops

- 5.4 Country

- 5.4.1 Australia

- 5.4.2 Bangladesh

- 5.4.3 China

- 5.4.4 India

- 5.4.5 Indonesia

- 5.4.6 Japan

- 5.4.7 Myanmar

- 5.4.8 Pakistan

- 5.4.9 Philippines

- 5.4.10 Thailand

- 5.4.11 Vietnam

- 5.4.12 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Bejo Zaden BV

- 6.4.5 Corteva Agriscience

- 6.4.6 East-West Seed

- 6.4.7 Groupe Limagrain

- 6.4.8 Rijk Zwaan Zaadteelt en Zaadhandel BV

- 6.4.9 Syngenta Group

- 6.4.10 Yuan Longping High-Tech Agriculture Co. Ltd

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms