|

市場調査レポート

商品コード

1444878

経口糖尿病治療薬: 市場シェア分析、業界動向と統計、成長予測(2024年~2029年)Oral Anti-Diabetic Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 経口糖尿病治療薬: 市場シェア分析、業界動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

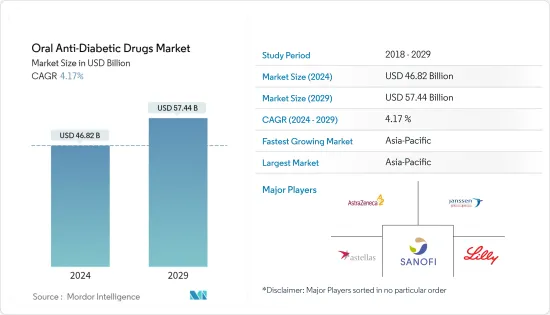

経口糖尿病治療薬市場規模は2024年に468億2,000万米ドルと推定され、2029年までに574億4,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に4.17%のCAGRで成長します。

市場は2027年までに520億米ドル以上の価値に達すると推定されています。

COVID-19のパンデミックは、経口糖尿病治療薬市場に大きな影響を与えています。COVID-19感染症で入院した患者における糖尿病の有病率と、血糖コントロールの改善により、SARS-CoV-2患者の転帰が改善し、入院期間が短縮される可能性があるという認識は、経口糖尿病治療薬市場の重要性を強調しています。糖尿病患者は免疫力が弱く、COVID-19感染症の合併症により症状が悪化して、免疫力が急速に弱まってしまいます。糖尿病と制御されていない高血糖は、重症化または死亡のリスク増加を含む、COVID-19感染症患者の予後不良の危険因子です。このように、COVID-19の発生により、世界的に経口糖尿病治療薬市場の成長が加速しました。

国際糖尿病連盟(IDF)によると、2021年の成人糖尿病人口は約5億3,700万人で、この数は2030年には6億4,300万人増加すると予想されています。1型および2型糖尿病の新規診断症例の割合は増加すると見られています。、主に肥満、不健康な食事、運動不足が原因です。世界中で糖尿病患者の発生率と有病率、ヘルスケア費が急速に増加していることは、抗糖尿病薬の使用量が増加していることを示しています。この間に技術の進歩と革新が進み、開発中の薬剤や製剤にいくつかの変更が加えられました。

したがって、前述の要因により、調査対象の市場は分析期間中に成長すると予想されます。

経口糖尿病薬市場動向

ビグアニドセグメントが今年度の経口糖尿病治療薬市場で最高の市場シェアを占める

ビグアニドセグメントは、今年度の経口糖尿病治療薬市場で約45%の最高シェアを占めています。

メトホルミンは、2型糖尿病の治療に使用されるビグアニドとして分類されます。インスリン抵抗性などの症状のある人に対する適応外使用のために処方されています。 T2DM治療にメトホルミンがイントロダクション以来、多くの患者がこの世界的に利用可能な薬剤で治療に成功しました。これには、IDFガイドラインで第一選択薬として推奨されている有利なリスク/ベネフィットプロファイルが含まれています。メトホルミンの長期にわたる良好な使用経験、臨床効果、安全性、高い遵守率、低コスト、一般入手可能性、費用対効果の強力な証拠が、高い市場シェアの要因となっています。世界保健機関はメトホルミンを必須医薬品のリスト、つまり「国民の医療ニーズの優先順位を満たす医薬品」に加えました。

ビグアニドは、2型糖尿病の治療に使用される薬剤の一種です。それらは、消化中に発生するグルコースの生成を減らすことによって機能します。メトホルミンは、現在ほとんどの国で糖尿病の治療に利用できる唯一のビグアナイド薬です。グルコファージ(メトホルミン)およびグルコファージ XR(メトホルミン徐放)は、これらの薬剤のよく知られたブランド名です。他には、フォルタメット、グルメッツァ、リオメットなどがあります。メトホルミンは、スルホニル尿素など、他のいくつかの種類の糖尿病治療薬と組み合わせて使用することもできます。

2022年7月、Zydus Lifesciencesは、エンパグリフロジン錠剤と塩酸メトホルミン錠剤を複数の強度で販売する最終承認を取得したと発表しました。エンパグリフロジンおよび塩酸メトホルミン錠剤は、2型糖尿病の成人の血糖コントロールを改善するために、適切な食事と運動とともに使用されます。また、2型糖尿病および既往の心血管疾患を有する患者の心血管死のリスクを下げるためにも使用されます。

上記の要因と普及の増加により、市場は成長し続ける可能性があります。

アジア太平洋地域は、予測期間中に経口糖尿病治療薬市場で最高のCAGRを示すと予想されます

アジア太平洋地域は、予測期間中に4%以上のCAGRで推移すると予想されます。

国際糖尿病連盟によると、2021年時点でIDF東南アジア地域では9,000万人の成人が、IDF西太平洋地域では2億600万人の成人が糖尿病を抱えて暮らしています。この数字は、2030年までに1億1,300万人、2億3,800万人に増加すると推定されています。 DPP-4やSGLT-2などの新世代経口薬が糖尿病患者のCVリスク率を低下させるため、経口糖尿病治療薬の使用率は増加しています。

中国と日本は、糖尿病人口の増加により、アジア太平洋地域の潜在的な新興国市場として認識されています。日本は成熟市場であり、経済成長の鈍化、人口の高齢化、競合の激化などの課題を抱えています。この国ではジェネリック医薬品メーカーが大幅に増加しています。さらに、調査対象市場における主要な世界的企業は、地域の企業との激しい競合に直面しています。

糖尿病は寿命を縮め、この疾患を持つ人々は失明したり、切断、腎不全、心臓発作、脳卒中、心不全などで入院する可能性が高くなります。 T2D患者に使用される第一選択療法はメトホルミン単独療法です。メトホルミンが禁忌であるか許容されない場合、または最大耐用量で3か月使用しても治療目標が達成されない場合は、他の選択肢を考慮する必要があります。糖尿病治療薬の範囲は拡大しており、ジペプチジルペプチダーゼ-4(DPP-4)阻害剤、ナトリウム-グルコース共輸送体-2阻害剤、およびグルカゴン様ペプチド-1アゴニストが含まれており、これらは一般にメトホルミンによる治療を補うために使用されます。

上記の要因により、市場は予測期間中に成長すると予想されます。

経口糖尿病治療薬業界の概要

経口糖尿病治療薬市場は適度に細分化されており、イーライリリー、アストラゼネカ、サノフィ、ヤンセンファーマシューティカルズなどの大手メーカーが世界市場で存在感を示しています。対照的に、残りのメーカーは他の地域市場に限定されています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替製品やサービスの脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 薬物

- ビグアニデス

- メトホルミン

- α-グルコシダーゼ阻害剤

- α-グルコシダーゼ阻害剤

- ドーパミン-D2受容体作動薬

- ブロモクリプチン(サイクロゼット)

- ナトリウム-グルコース共輸送-2(SGLT-2)阻害剤

- インボカナ(カナグリフロジン)

- ジャディアンス(エンパグリフロジン)

- フォシーガ/フォシーガ(ダパグリフロジン)

- スーグラ(イプラグリフロジン)

- ジペプチジルペプチダーゼ-4(DPP-4)阻害剤

- ジャヌビア(シタグリプチン)

- オングリザ(サクサグリプチン)

- トラジェンタ(リナグリプチン)

- Vipidia/Nesina(アログリプチン)

- ガルバス(ビルダグリプチン)

- スルホニル尿素

- スルホニル尿素

- メグリチニド

- メグリチニド

- ビグアニデス

- 地域

- 北米

- 米国

- カナダ

- その他の北米

- 欧州

- フランス

- ドイツ

- イタリア

- スペイン

- 英国

- ロシア

- その他の欧州

- ラテンアメリカ

- メキシコ

- ブラジル

- その他のラテンアメリカ

- アジア太平洋

- 日本

- 韓国

- 中国

- インド

- オーストラリア

- ベトナム

- マレーシア

- インドネシア

- フィリピン

- タイ

- その他のアジア太平洋

- 中東・アフリカ

- サウジアラビア

- イラン

- エジプト

- オマーン

- 南アフリカ

- その他の中東・アフリカ

- 北米

第6章 市場指標

- 1型糖尿病人口

- 2型糖尿病の人口

第7章 競合情勢

- 企業プロファイル

- Sanofi SA

- Eli Lilly and Company

- AstraZeneca

- Astellas Pharma Inc.

- Johnson &Johnson(Janssen Pharmaceuticals)

- Boehringer Ingelheim

- Merck And Co.

- Takeda

- Bristol Myers Squibb

- Novartis

- Pfizer

- 企業シェア分析

- Sanofi SA

- Eli Lilly and Company

- AstraZeneca

- Merck and Co.

- Others

第8章 市場機会と将来の動向

The Oral Anti-Diabetic Drugs Market size is estimated at USD 46.82 billion in 2024, and is expected to reach USD 57.44 billion by 2029, growing at a CAGR of 4.17% during the forecast period (2024-2029).

The market is estimated to reach a value of more than USD 52 billion by 2027.

The COVID-19 pandemic has had a substantial impact on the oral anti-diabetic drugs market. The prevalence of diabetes in people hospitalized with COVID-19 infection and the recognition that improved glycemic control might improve outcomes and reduce the length of stay in patients with SARS-CoV-2 have underlined the importance of the oral anti-diabetic drugs market. People with diabetes have a weaker immune system, the COVID-19 complication aggravates the condition, and the immune system gets weaker very fast. Diabetes and uncontrolled hyperglycemia are risk factors for poor outcomes in patients with COVID-19 including an increased risk of severe illness or death. Thus, the COVID-19 outbreak increased the oral anti-diabetic drugs market's growth globally.

According to International Diabetes Federation (IDF), the adult diabetes population in 2021 is approximately 537 million, and this number is going to increase by 643 million in 2030. The rate of newly diagnosed cases of Type 1 and Type 2 diabetes is seen to increase, mainly due to obesity, unhealthy diet, and physical inactivity. The rapidly increasing incidence and prevalence of diabetic patients and healthcare expenditure worldwide are indications of the increasing usage of anti-diabetic drugs. Technological advancements and innovations have increased over the period leading to several modifications either in the drugs or the formulations being developed.

Therefore, owing to the aforementioned factors the studied market is anticipated to witness growth over the analysis period.

Oral Anti Diabetic Drugs Market Trends

Biguanide Segment Occupies the Highest Market Share in the Oral Anti-Diabetic Drugs Market in the current year

Biguanide Segment holds the highest share of about 45% in the Oral Anti-Diabetic Drugs Market in the current year.

Metformin is classified as a biguanide used for treating type 2 diabetes. It is prescribed for its off-label use in people with conditions such as insulin resistance. Since the introduction of metformin in T2DM therapy, many patients were treated successfully with this globally available medication. It includes a favorable risk/benefit profile recommended by IDF guidelines as a first-line drug. Long-term positive experience with the use of metformin, strong evidence of clinical efficacy, safety, high adherence rate, low cost, general availability, and cost-effectiveness are the contributing factors to the high market share. The World Health Organization put metformin on the list of essential medicines: 'medicines that satisfy the priority of health care needs of the population.'

Biguanides are a class of medications used to treat type 2 diabetes. They work by reducing the production of glucose that occurs during digestion. Metformin is the only biguanide currently available in most countries for treating diabetes. Glucophage (metformin) and Glucophage XR (metformin extended release) are well-known brand names for these drugs. Others include Fortamet, Glumetza, and Riomet. Metformin is also available in combination with several other types of diabetes medications, such as sulfonylureas.

In July 2022, Zydus Lifesciences announced that it had received final approval to market Empagliflozin and Metformin Hydrochloride tablets in multiple strengths. Empagliflozin and Metformin Hydrochloride tablets are used with proper diet and exercise to improve glycemic control in adults with type 2 diabetes mellitus. They are also used to lower the risk of cardiovascular death in patients with type 2 diabetes mellitus and established cardiovascular disease.

Owing to the factors above and the increasing prevalence, the market will likely continue to grow.

Asia-Pacific Region is Expected to witness highest CAGR in the Oral Anti-Diabetic Drugs Market over the forecast period

The Asia-Pacific region is expected to register a CAGR of more than 4% over the forecast period.

According to International Diabetes Federation, 90 million adults lived with diabetes in the IDF South-East Asia Region and 206 million adults in the IDF Western Pacific Region in 2021. This figure is estimated to increase to 113 million and 238 million by 2030. The use of oral anti-diabetes drugs is rising because new-generation oral drugs, such as DPP-4 and SGLT-2, reduce the rate of CV risk in diabetes patients.

China and Japan are recognized as potential developing markets in the Asia-Pacific region due to the growing diabetic population. Japan is a mature market with associated challenges, like slow economic growth, an aging population, and increased competition. The country is witnessing a significant increase in generic drug manufacturers. Furthermore, the leading global players in the market studied are facing intense competition from the regional players.

Diabetes reduces lifespan, and people with the disease are likely to experience blindness and be hospitalized for amputations, kidney failure, heart attacks, strokes, and heart failure. First-line therapy used in patients with T2D is metformin monotherapy. Other options must be considered when metformin is contraindicated or not tolerated or when treatment goals are not achieved after three months of use at the maximum tolerated dose. The growing spectrum of diabetes mellitus drugs includes dipeptidyl peptidase-4 (DPP-4) inhibitors, sodium-glucose cotransporter-2 inhibitors, and glucagon-like peptide-1 agonists, generally used to supplement treatment with metformin.

The market is expected to grow during the forecast period due to the factors above.

Oral Anti Diabetic Drugs Industry Overview

The oral anti-diabetes drug market is moderately fragmented, with major manufacturers like Eli Lilly, AstraZeneca, Sanofi, Janssen Pharmaceuticals, etc., having a global market presence. In contrast, the remaining manufacturers are confined to the other local or regional markets.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Drugs

- 5.1.1 Biguanides

- 5.1.1.1 Metformin

- 5.1.2 Alpha-glucosidase inhibitors

- 5.1.2.1 Alpha-glucosidase Inhibitors

- 5.1.3 Dopamine -D2 Receptor Agonist

- 5.1.3.1 Bromocriptin (Cycloset)

- 5.1.4 Sodium-glucose Cotransport -2 (SGLT-2) inhibitor

- 5.1.4.1 Invokana (Canagliflozin)

- 5.1.4.2 Jardiance (Empagliflozin)

- 5.1.4.3 Farxiga/Forxiga (Dapagliflozin)

- 5.1.4.4 Suglat (Ipragliflozin)

- 5.1.5 Dipeptidyl Peptidase - 4 (DPP-4) Inhibitors

- 5.1.5.1 Januvia (Sitagliptin)

- 5.1.5.2 Onglyza (Saxagliptin)

- 5.1.5.3 Tradjenta (Linagliptin)

- 5.1.5.4 Vipidia/Nesina (Alogliptin)

- 5.1.5.5 Galvus (Vildagliptin)

- 5.1.6 Sulfonylureas

- 5.1.6.1 Sulfonylureas

- 5.1.7 Meglitinides

- 5.1.7.1 Meglitinides

- 5.1.1 Biguanides

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Rest of North America

- 5.2.2 Europe

- 5.2.2.1 France

- 5.2.2.2 Germany

- 5.2.2.3 Italy

- 5.2.2.4 Spain

- 5.2.2.5 United Kingdom

- 5.2.2.6 Russia

- 5.2.2.7 Rest of Europe

- 5.2.3 Latin America

- 5.2.3.1 Mexico

- 5.2.3.2 Brazil

- 5.2.3.3 Rest of Latin America

- 5.2.4 Asia-Pacific

- 5.2.4.1 Japan

- 5.2.4.2 South Korea

- 5.2.4.3 China

- 5.2.4.4 India

- 5.2.4.5 Australia

- 5.2.4.6 Vietnam

- 5.2.4.7 Malaysia

- 5.2.4.8 Indonesia

- 5.2.4.9 Philippines

- 5.2.4.10 Thailand

- 5.2.4.11 Rest of Asia-Pacific

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 Iran

- 5.2.5.3 Egypt

- 5.2.5.4 Oman

- 5.2.5.5 South Africa

- 5.2.5.6 Rest of Middle East and Africa

- 5.2.1 North America

6 MARKET INDICATORS

- 6.1 Type 1 Diabetes Population

- 6.2 Type 2 Diabetes Population

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Sanofi S.A.

- 7.1.2 Eli Lilly and Company

- 7.1.3 AstraZeneca

- 7.1.4 Astellas Pharma Inc.

- 7.1.5 Johnson & Johnson (Janssen Pharmaceuticals)

- 7.1.6 Boehringer Ingelheim

- 7.1.7 Merck And Co.

- 7.1.8 Takeda

- 7.1.9 Bristol Myers Squibb

- 7.1.10 Novartis

- 7.1.11 Pfizer

- 7.2 Company Share Analysis

- 7.2.1 Sanofi S.A.

- 7.2.2 Eli Lilly and Company

- 7.2.3 AstraZeneca

- 7.2.4 Merck and Co.

- 7.2.5 Others