|

市場調査レポート

商品コード

1911717

軍用輸送機:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Military Transport Aircraft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 軍用輸送機:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

概要

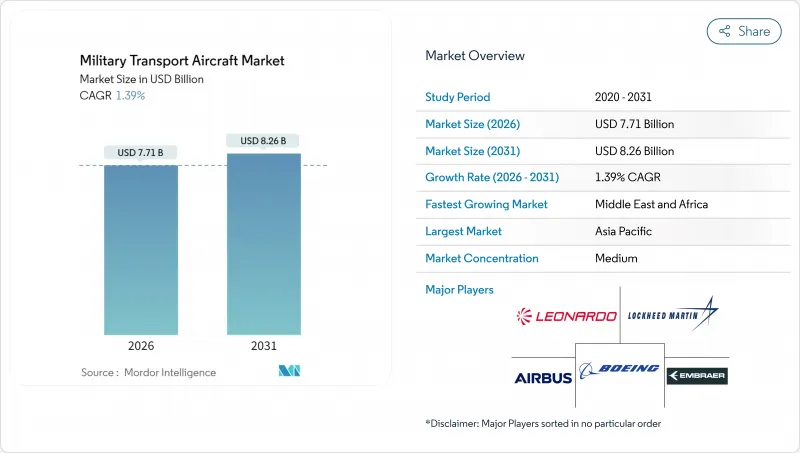

軍事輸送機市場は2025年に76億米ドルと評価され、2026年の77億1,000万米ドルから2031年までに82億6,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは1.39%と見込まれます。

現在の拡大は、地政学的緊張の高まり、緊急人道支援活動、計画的な機体更新サイクルに起因しています。アジア太平洋地域の防衛省は大型戦略プラットフォームの調達を継続する一方、小国ではインフラ投資が少なくて済む軽・中型輸送機を好んでいます。近代化計画では、オープンアーキテクチャの航空電子機器、デジタルスレッド整備システム、多目的再構成性がますます指定され、運用者はダウンタイムの削減と任務範囲の拡大が可能となっています。調達予算は堅調なままですが、複合構造体や航空エンジンのサプライチェーンのボトルネックにより、年間納入台数が抑制されており、メーカーはより長いリードタイムの交渉や、追加のTier 2サプライヤーの活用を余儀なくされています。競合のダイナミクスとしては、中国、インド、韓国からの国内メーカーが、エアバス、ボーイング、ロッキード・マーティンといった従来の支配的企業と競争している点が特徴であり、この動きは2030年までの輸出パターンを再構築する可能性が高いと考えられます。

世界の軍用輸送機市場の動向と展望

アジア太平洋地域および中東における防衛予算の増大

2024年、中国の防衛支出は2,960億米ドル、アラブ首長国連邦の航空機調達額は18%増と、防衛支出は急増しました。こうした予算増は、新たな大型輸送機プログラム、寿命延長パッケージ、技術移転条項を含む現地産業パートナーシップに充てられています。また、持続的な支出は、ライフサイクルコストの削減と任務準備の迅速化を図るデジタルロジスティクススイートの調査も支えています。湾岸協力会議(GCC)加盟国は、モジュラー式のA400MおよびC-130Jバリエーションに向けて、艦隊の多様化を継続しており、連合作戦における連合パートナーとの相互運用性を確保しています。

老朽化したC-130/L-100およびAN-26クラスの代替となる艦隊近代化プログラム

旧式のC-130A/BおよびAn-26機体の60%以上が就航40年を超えているため、運用者は、新造のC-390、C-295、およびKC-390ミレニアムモデルを優先する競合入札を迅速に進めています。スウェーデンが2024年に4機のC-390を注文したことは、フライ・バイ・ワイヤ制御と低燃費を備えた高スループット機体への移行を示しています。東欧のユーザーは同時に、ロシアのサプライチェーンへの依存度を低減するため、ソ連時代の輸送システムを退役させており、2035年まで着実な代替需要を生み出しています。

ワイドボディ複合材構造体および航空エンジンの供給網制約

プラット・アンド・ホイットニー社のTP400シリーズおよび東レ社の炭素繊維原料は、2024年に18ヶ月分の受注残を抱え、A400Mの納入遅延を招くとともに、OEMメーカーに生産スケジュールの再調整を余儀なくさせました。この供給不足は単価上昇を招き、各国空軍は暫定的な能力不足を容認するか、追加チャーター便の「緊急増便」費用を支払うことを迫られています。

セグメント分析

2025年の軍用輸送機市場規模において、固定翼輸送機は61.12%を占めました。これはC-130JスーパーハーキュリーズやA400Mアトラスといった信頼性の高い機種が牽引しています。継続的なブロックアップグレードにより、相互運用性認証を維持しつつ、積載量と航続距離の生産性が向上しています。一方、回転翼機は、制圧環境下におけるポイント・ツー・ポイント輸送への教義転換の恩恵を受け、軍事輸送機市場全体を上回るCAGR4.20%を記録しています。複合材ブレードの普及と改良された伝動装置設計により揚力重量比が向上し、チヌークやCH-53K機群の外部吊り下げ能力が拡大しています。

回転翼機のシェア拡大は、低シグネチャによる浸透作戦への特殊作戦需要も反映しており、CV-22のようなティルトローター機はジェット機並みの速度と垂直離着陸(VTOL)能力を兼ね備えています。しかしながら、戦域間移動においては固定翼機が依然として代替不可能です。C-390ミレニアムのフライ・バイ・ワイヤ制御システムは民間認証カテゴリーIIIb自動着陸を実現し、霧が発生しやすい前線基地への進入を可能にします。2030年まで、固定翼機の納入数は年間約95機で安定すると予想される一方、新型FLRAA(回転翼軍用輸送機)の参入が成熟するにつれ、回転翼機の調達数は140機でピークに達する可能性があります。

2025年の軍用輸送機市場規模において、兵員・物資空輸が34億1,000万米ドル(総額の44.85%)と最大のシェアを占め、各国が戦略的輸送能力を維持する中、市場全体のCAGR1.39%にほぼ連動する推移が見込まれます。このサブセグメントは、C-130JやA400Mといった固定翼主力機による恩恵を受けており、2024年には両機種で兵員輸送出撃の60%以上を占めました。艦隊計画担当者は、積載量と航続距離の向上、迅速な任務変更構成を優先しており、成長が頭打ちになってもセグメントの規模を維持しています。アジア太平洋地域と欧州における調達パイプラインは安定しています。一方、北米の運用機関はアビオニクス更新と耐用年数延長に注力しており、これが軍用輸送機市場におけるアフターマーケット支出の基盤となっています。

地域別分析

アジア太平洋地域は2025年の収益の39.05%を占め、軍用輸送機市場における地域的な主導的地位を確固たるものにしております。生産量は、Y-20の継続的な生産、インドの国産C-295ライン、および日本のC-2生産率拡大によるものです。主要経済圏における年間平均8.5%の防衛予算成長に牽引され、同地域のCAGRは1.75%と予測されています。クアッド(Quad)が推進する相互運用性要件などの能力協力は、共同乗員訓練契約をさらに促進します。

北米は28.50%のシェアを占め、主に米国空軍プログラムが牽引。2024年にはC-130Jの飛行時間が12%増加しました。カナダのCC-330ハスキー給油輸送機計画やメキシコのCN-235拡充は、大陸全体の需要拡大を裏付けています。大西洋を隔てた欧州は22.05%を占めましたが、サプライチェーンの混乱によりA400Mの生産は8機に留まりました。NATO戦略空輸能力(SAC)はパパ空軍基地からC-17をローテーション運用しており、同盟が共有資産に依存していることを示しています。

中東・アフリカ地域は3.60%のCAGRで最も急成長する市場として浮上しています。ナイジェリアのC-295 4機発注や南アフリカのC-130BZ近代化計画は、平和維持活動や人道支援任務が厳しい予算制約を上回ることを示しています。湾岸諸国は中東・アフリカの統計を統合しており、UAEの新型C-130J-30導入とカタールのA400M購入計画が地域全体のCAGR2.32%を支えています。アフリカ連合の共有インフラは国境を越えた空輸作戦を可能にし、規制上の障壁を緩和するとともに、共同整備基地の設置を促進しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 主要産業動向

- 国内総生産

- 北米

- 欧州

- アジア太平洋地域

- 南米

- 中東・アフリカ

- 稼働艦隊データ

- 北米

- 欧州

- アジア太平洋地域

- 南米

- 中東・アフリカ

- 防衛支出

- 北米

- 欧州

- アジア太平洋地域

- 南米

- 中東・アフリカ

第5章 市場情勢

- 市場概要

- 市場促進要因

- アジア太平洋地域および中東における防衛予算の増加傾向

- 老朽化したC-130/L-100およびAn-26クラスの代替を目的とした機体近代化プログラム

- 地政学的緊張地域が緊急輸送能力を促進

- 人道支援・災害救援任務の拡大に伴う多目的輸送機の需要増加

- デジタルスレッドMROによるダウンタイム削減とアフターマーケット収益基盤の拡大

- 俊敏なラストマイル補給を実現する新興eVTOL物流機

- 市場抑制要因

- ワイドボディ複合材構造体および航空エンジンのサプライチェーン制約

- 総所有コストの高さに対する貨物輸送機へのリース転換の可能性

- 輸出管理およびITAR規制によるプラットフォームの対応可能市場の制限

- 分散運用における滑走路利用可能性リスクが重量物輸送の有用性を制限

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第6章 市場規模と成長予測

- 航空機タイプ別

- 固定翼輸送機

- 回転翼輸送機

- 用途別

- 部隊および物資の空輸

- 人道支援および災害救援

- 特殊任務(医療後送、捜索救助、要人護衛)

- エンドユーザーサービス別

- 空軍

- 陸軍航空隊

- 海軍/海兵隊航空部隊

- 合同/特殊作戦

- 準軍事組織および沿岸警備隊

- 推進タイプ別

- ターボプロップ

- ターボシャフト

- ターボファン

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- スペイン

- イタリア

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- インドネシア

- その他アジア太平洋地域

- 南米

- ブラジル

- その他南米

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- カタール

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 中東

- 北米

第7章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Airbus SE

- Lockheed Martin Corporation

- The Boeing Company

- Leonardo S.p.A.

- Embraer S.A.

- ANTONOV COMPANY(Ukroboronprom)

- Rostec

- Kawasaki Heavy Industries, Ltd.

- Korea Aerospace Industries Ltd.

- Aviation Industry Corporation of China(AVIC)

- PT Dirgantara Indonesia

- De Havilland Aircraft of Canada Limited

第8章 市場機会と将来の展望

- ホワイトスペースと未充足ニーズの評価