|

|

市場調査レポート

商品コード

1444908

血小板凝集デバイス:市場シェア分析、業界動向と統計、成長予測(2024年~2029年)Platelet Aggregation Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 血小板凝集デバイス:市場シェア分析、業界動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

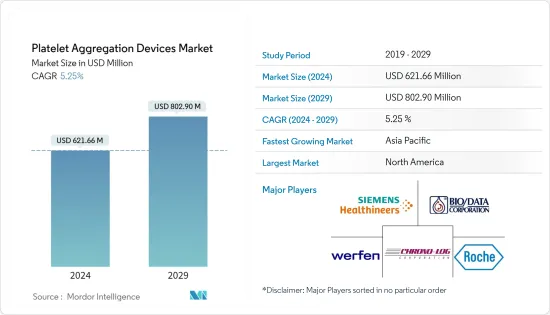

血小板凝集デバイスの市場規模は、2024年に6億2,166万米ドルと推定され、2029年までに8億290万米ドルに達すると予測されており、予測期間(2024年から2029年)中に5.25%のCAGRで成長します。

COVID-19の世界の流行は市場に大きな影響を与え、SARS-CoV-2感染がアテローム血栓現象と関連していることを示す実質的な証拠があった。 2021年 7月に発表されたNCBIの記事では、血小板減少症の発生率はSARS-CoV-2感染症における重大な出来事であり、呼吸器症状を悪化させるだけでなく、死亡リスクを高める可能性があり、血小板減少症に関連する予後因子であると述べられています。 COVID-19。COVID-19に関与するヒト血小板細胞の血小板凝集プロセスに関連する調査の増加は、パンデミック期間中の市場の成長に顕著な影響を与えました。また、血小板凝集デバイスの需要はパンデミック後の期間もそのまま維持されると予想され、それによりパンデミック期間中の市場の成長を促進します。

血小板凝集デバイス市場の成長に寄与する主な要因は、慢性疾患の負担の増加、高齢者人口の増加、血小板凝集計の技術進歩です。

たとえば、2022年 1月に発表された英国心臓財団(BHF)のデータによると、世界中で影響を受ける最も一般的な心臓病は、冠状動脈(虚血性)心疾患(世界有病率は2億人と推定)、末梢動脈(血管)疾患(1億1,000万人)でした。報告書はまた、心臓疾患と循環器疾患の有病率が北米で4,600万人、欧州で9,900万人、アフリカで5,800万人、南米で3,200万人であると述べた。したがって、世界人口における心血管疾患の高い発生率が市場の成長に寄与すると予想されます。したがって、心血管疾患に苦しむ人の数が大幅に増加すると、最終的には影響を受けた患者の血小板凝集を研究するための血小板凝集デバイスの使用が増加し、予測期間中の市場の成長を促進する可能性があります。

さらに、主要な市場プレーヤーによるさまざまな高度な血小板凝集デバイスの発売の増加も、予測期間中の市場の成長を促進すると予想されます。たとえば、2021年 7月、シスメックス株式会社は2つの新しい自動血液凝固分析装置 CN-3500およびCN-6500をEMEA地域の特定の国で発売しました。 CN-6000/CN-6000/CN-で測定可能な血液凝固、血小板凝集に加え、血栓、止血など幅広い検査オーダーに応じて柔軟に測定できる新型血液凝固分析装置です。 3000。

しかし、新しい技術やデバイスを扱う熟練した専門家が不足しているため、市場は予測期間中の成長の面で障害を経験すると予想されます。

血小板凝集デバイスの市場動向

システム部門は、予測期間中に市場で顕著な成長が見込まれる

血小板凝集システムまたは血小板凝集計は、血小板がどの程度よく付着しているかを決定します。このようなシステムは、ADP、トロンビン、リストセチンなどの血小板アンタゴニストを使用して血小板凝集を測定します。凝集システムは、血小板凝集デバイスの分野における継続的な技術進歩、血小板凝集検査方法の動向の高まり、採用の増加、診断検査機関における自動化システムに対する市場の選好などの要因により、予測期間中に成長する可能性が高いです。従来の機器と比較して、ポイントオブケア検査分析装置が提供する利点はますます大きくなっています。

出血性疾患や心血管疾患による負担の増大により、出血性疾患の診断に使用される血小板凝集システムの需要が増加すると予想されます。 2022年 7月にGenetic Home Referenceの最新情報によって提供されたデータによると、免疫性血小板減少症の発生率は、世界中で毎年、小児では100,000人あたり4人、成人では100,000人あたり3人と推定されています。このような出血性疾患の発生率は、抗血栓因子をスクリーニングするための血小板凝集システムの需要を促進し、それによって研究分野の成長に貢献すると予想されます。

さらに、提携、買収、合併などの新興市場プレーヤーの戦略も、調査対象セグメントの成長を促進すると予想されます。たとえば、2021年 7月、バクスターインターナショナル社は、バクスターヘルスケアコーポレーションの子会社がCryoLife, Inc.からPerClot多糖類止血システムに関連する資産の買収を完了したと報告しました。PerClot多糖類止血システムは、制御のための補助止血装置として使用されます。婦人科、一般、心臓血管、泌尿器科を含む複数の開腹手術および腹腔鏡手術中の出血。

したがって、出血性疾患の発生率の増加や市場プレーヤーの戦略などの上記の要因により、このセグメントの市場は予測期間中に成長すると予想されます。

北米は予測期間中に市場で最大のシェアを保持すると予想される

北米地域は、対象となる疾患の増加、高齢者人口の増加、血小板凝集計の技術進歩、血小板がもたらす利点に対するヘルスケア従事者の意識の高まりにより、機器メーカーの強い存在感により最大の市場シェアを保持しています。病気の診断における集計検査。

2021年に更新された米国疾病予防管理センター(CDC)の統計報告によると、アメリカ人は40秒ごとに心臓発作を起こす可能性があります。また、世界血友病連盟の2021年報告書によると、米国には約14,816人の血友病患者(血友病 A 11,790人、血友病 B 3,026人を含む)と血友病と診断された人がおり、米国では3,924人の血友病患者がいます。したがって、この地域ではさまざまな慢性疾患や血液疾患の発生率が高く、効果的な疾患診断により血小板凝集デバイスの需要が高まると予想されます。

さらに、規制当局による製品承認の増加も、この地域の市場の成長に寄与すると予想されます。たとえば、2022年11月、Cerus Corporationはカナダ保健省から、INTERCEPT血液システムで治療された血小板の保管期間を収集時から5日間から7日間に延長する承認を取得し、インターセプト血小板の7日間が承認されている他の地域に加わりました。ストレージ。

したがって、慢性疾患や血液疾患の発生率の増加や製品開発の増加などの上記の要因により、北米地域は予測期間中に有利な成長を示すと予想されます。

血小板凝集デバイス業界の概要

調査された血小板凝集デバイス市場は中程度の競争があり、いくつかの企業がこの市場で事業を行っています。斬新な発売と最近の開発は、主要企業が血小板凝集デバイス市場での地位を確立するために採用する重要な戦略です。市場における世界のプレーヤーは、Aggredyne Inc.、Bio/Data Corporation、Chrono-Log Corporation、F. Hoffmann-La Roche Ltd、Haemonetics Corporation、Siemensヘルスケア GmbH、Werfenなどです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 慢性疾患の発生率の増加

- 高齢者人口の増加

- 血小板凝集計の技術の進歩

- 市場抑制要因

- 機器の高価格と熟練した人材の不足

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品別

- システム

- 試薬

- 消耗品と付属品

- 用途別

- 臨床応用

- 研究用途

- エンドユーザー別

- 病院

- 診断研究所

- その他のエンドユーザー

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- AggreDyne, Inc.

- Bio/Data Corporation

- Chrono-Log Corporation

- F. Hoffmann-La Roche Ltd

- Haemonetics Corporation

- Siemens Healthcare GmbH

- Werfen

- Sysmex Corporation

- Sienco, Inc.

- Drucker Diagnostics

- Heamochrom Diagnostica GmbH

- Grifols, SA

第7章 市場機会と将来の動向

The Platelet Aggregation Devices Market size is estimated at USD 621.66 million in 2024, and is expected to reach USD 802.90 million by 2029, growing at a CAGR of 5.25% during the forecast period (2024-2029).

The outbreak of COVID-19 worldwide had a significant impact on the market, and there was substantial evidence that SARS-CoV-2 infection is associated with atherothrombotic phenomena. An NCBI article published in July 2021 mentioned that the incidence of thrombocytopenia is a critical occurrence in SARS-CoV-2 infection, which not only may exacerbate the respiratory symptoms but also increase the risk of mortality and it is a prognostic factor associated with platelets in COVID-19. The increasing research related to the platelet aggregation process on human platelet cells involved in COVID-19 had a notable impact on the market's growth over the pandemic period. Also, the demand for platelet aggregation devices is expected to remain intact during the post-pandemic period, thereby fueling market growth over the pandemic period.

The major factors attributing to the growth of the platelet aggregation devices market are the rising burden of chronic diseases, the increasing geriatric population, and technological advancements in platelet aggregometer.

For instance, the British Heart Foundation (BHF) data published in January 2022 reported that the most common heart conditions affected globally were coronary (ischemic) heart disease (global prevalence estimated at 200 million), peripheral arterial (vascular) disease (110 million), stroke (100 million) and atrial fibrillation (60 million) in 2022. The report also mentioned that the prevalence of heart and circulatory diseases in North America was 46 million, in Europe 99 million, in Africa 58 million, in South America 32 million, and in Asia and Australia 310 million in 2022. Thus, the high incidence of cardiovascular diseases among the global population is expected to contribute to the market's growth. Thus, the significant increase in the number of people suffering from cardiovascular diseases ultimately increases the use of platelet aggregation devices to study platelet aggregation among the affected patients and may drive market growth over the forecast period.

Moreover, the increasing launches of various advanced platelet aggregation devices by key market players are also expected to drive the market's growth over the forecast period. For instance, in July 2021, Sysmex Corporation launched two new automated blood coagulation analyzers, CN-3500 and CN-6500, in specific countries in the EMEA region. These new blood coagulation analyzers allow for flexible measurements in response to a broad range of test orders in the fields of thrombosis and hemostasis, in addition to the blood coagulation and platelet aggregation parameters, which can also be measured by the CN-6000/CN-3000.

However, owing to the dearth of skilled professionals to handle new technologies or devices, the market is expected to witness hindrances in terms of growth over the forecast period.

Platelet Aggregation Devices Market Trends

The Systems Segment is Expected to Witness Notable Growth in the Market Over the Forecast Period

The platelet aggregation system or aggregometer determines how well the platelets stick together. Such systems measure platelet aggregation using a platelet antagonist, such as ADP, thrombin, and ristocetin. Aggregation systems are likely to grow over the forecast period due to factors such as continuous technological advances in the field of platelet aggregation devices, the escalation of trends in platelet aggregation testing methods, growing adoption, and market preference for automated systems among diagnostic laboratories, and growing advantages offered by point-of-care testing analyzers, as compared to conventional instruments.

The growing burden of bleeding disorders and cardiovascular disorders is expected to increase the demand for platelet aggregation systems, which are used to diagnose bleeding disorders. As per the data provided by Genetic Home Reference updates in July 2022, the incidence of immune thrombocytopenia was estimated at 4 per 100,000 in children and 3 per 100,000 in adults worldwide annually. Such incidence of bleeding disorders is expected to drive the demand for platelet aggregation systems to screen anti-thrombotic factors, thereby contributing to the growth of the studied segment.

Furthermore, the rising market player's strategies, such as collaborations, acquisitions, and mergers, are also expected to drive the growth of the studied segment. For instance, in July 2021, Baxter International, Inc. reported its Baxter Healthcare Corporation subsidiary had completed the acquisition of assets related to the PerClot Polysaccharide Hemostatic System from CryoLife, Inc. The PerClot Polysaccharide Hemostatic System is used as an adjunctive hemostatic device to control bleeding during multiple open and laparoscopic surgical procedures, including gynecologic, general, cardiovascular, and urology.

Hence, owing to the above-mentioned factors, such as the rising incidence of bleeding disorders and market players' strategies, the market in this segment is expected to grow over the forecast period.

North America is Expected to Hold the Largest Share in the Market Over the Forecast Period

The North American region holds the largest market share due to the strong presence of device manufacturers, due to the increasing number of target disorders, the increasing geriatric population, technological advancements in platelet aggregometer, and rising awareness among healthcare professionals regarding the benefits offered by platelet aggregation testing in disease diagnosis.

As per a report by the United States Centers for Disease Control (CDC) statistics updated in 2021, every 40 seconds, an American may have a heart attack. Also, according to the World Federation of Hemophilia 2021 report, there were about 14,816 patients with hemophilia (including Hemophilia A -11,790 and Hemophilia B-3,026) in the United States and people diagnosed with hemophilia in the United States and 3,924 patients with hemophilia in Canada (including Hemophilia A -3,223 and Hemophilia B-701) in 2021. Therefore, the high incidence of various chronic and blood disorders in this region is expected to drive the demand for platelet aggregation devices owing to the effective disease diagnosis.

Additionally, the increasing product approvals by the regulatory authorities are also expected to contribute to the growth of the market in this region. For instance, in November 2022, Cerus Corporation received approval from Health Canada to extend the storage of platelets treated with the INTERCEPT blood system from five days to seven days from the time of collection, joining other territories where intercept platelets are approved for seven-day storage.

Thus, owing to the abovementioned factors, such as the increasing incidence of chronic and blood disorders and rising product developments, the North American region is expected to show lucrative growth over the forecast period.

Platelet Aggregation Devices Industry Overview

The Platelet Aggregation Devices Market studied is moderately competitive, and several companies are operating in this market. The novel launches and recent developments are the key strategies the key players adopt to develop their positions in the platelet aggregation devices market. The global players in the market are Aggredyne Inc., Bio/Data Corporation, Chrono-Log Corporation, F. Hoffmann-La Roche Ltd, Haemonetics Corporation, Siemens Healthcare GmbH, and Werfen, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Chronic Diseases

- 4.2.2 Increasing Geriatric Population

- 4.2.3 Technological Advancements in Platelet Aggregometers

- 4.3 Market Restraints

- 4.3.1 High Cost of Devices and Shortage of Skilled Personnel

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product

- 5.1.1 Systems

- 5.1.2 Reagents

- 5.1.3 Consumables and Accessories

- 5.2 By Application

- 5.2.1 Clinical Applications

- 5.2.2 Research Applications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Diagnostic Laboratories

- 5.3.3 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle-East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle-East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 AggreDyne, Inc.

- 6.1.2 Bio/Data Corporation

- 6.1.3 Chrono-Log Corporation

- 6.1.4 F. Hoffmann-La Roche Ltd

- 6.1.5 Haemonetics Corporation

- 6.1.6 Siemens Healthcare GmbH

- 6.1.7 Werfen

- 6.1.8 Sysmex Corporation

- 6.1.9 Sienco, Inc.

- 6.1.10 Drucker Diagnostics

- 6.1.11 Heamochrom Diagnostica GmbH

- 6.1.12 Grifols, S.A.