|

市場調査レポート

商品コード

1850380

建設機械レンタル:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Construction Equipment Rental - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 建設機械レンタル:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

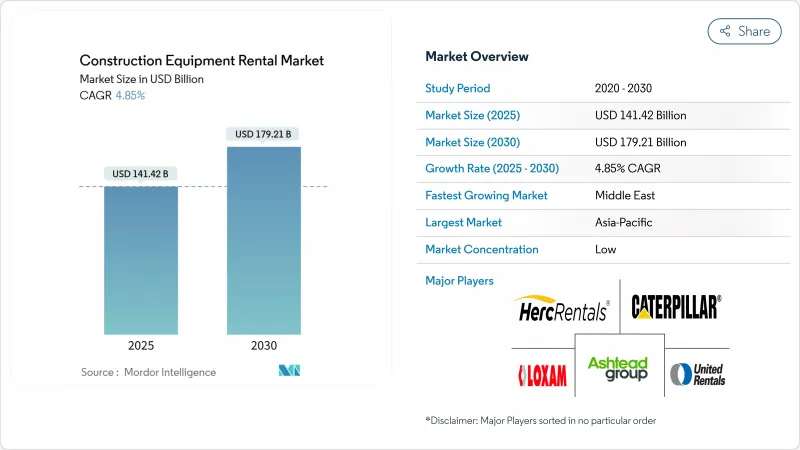

建設機械レンタル市場は2025年に1,414億2,000万米ドルに達し、CAGR 4.85%で拡大し、2030年には1,792億1,000万米ドルに達すると予測されます。

この勢いは、記録的な公共部門のインフラパイプライン、アセットライトモデルを好む請負業者の拡大、レンタル取引の急速なデジタル化から生じています。電気機械や水素燃料電池機械の採用が増加し、成果ベースのサービス契約と相まって、フリート戦略が再構築され、プレミアム価格のニッチが開かれつつあります。アジア太平洋地域は、持続的な高速道路、鉄道、都市再開発プログラムを背景に規模の主導権を維持し、中東はビジョン2030のメガプロジェクトに支えられて地域最速の成長を遂げています。大手企業が地理的な密度と技術力を得るために買収を加速させているため、競合の激しさは増しています。テレマティクスを活用したフリートの最適化は、稼働率向上と顧客維持のための重要なテコとして台頭しており、熟練労働者不足と複数ブランドのメンテナンスの複雑さによる逆風を一部相殺しつつあります。

世界の建設機械レンタル市場動向と洞察

インフラ刺激策の大型プロジェクト・パイプライン

米国の1兆2,000億米ドルのインフラ投資・雇用促進法とインドの1兆4,000億米ドルの国家インフラパイプラインは、複数年の機器需要サイクルを煽っています。ユナイテッドレンタルによると、メガプロジェクトはすでにレンタル受注に占める割合が増加しており、プロジェクトのライフサイクル全体にわたって予測可能な利用を支えています。請負業者は、遊休資本を避けるために、個別のフェーズに特化した機械のレンタルを好むようになっており、これらのプログラムの再生可能エネルギーコンポーネントは、水素とバッテリー電気アースムーバーの早期導入を推進しています。アジア太平洋と北米は、ロジスティクス・ネットワークが密で、多様なフリート・ミックスを供給できるレンタル支店が確立されているため、最も恩恵を受けています。公共事業の規模はまた、小規模プロバイダーがデジタル取引所を通じて機器をシンジケートすることを促し、第一級都市以外へのアクセスを広げています。

請負業者のCAPEXからOPEXへのシフト

高金利と不安定な受注残により、フリート・マネジャーは現場機材の最大80%をレンタルするようになり、バランスシートのレバレッジが大幅に低下しています。米国の請負業者の37%が購入延期を報告しており、運用支出モデルの魅力が高まっていることを裏付けています。サービスとしての設備契約は、メンテナンスと残存価値のリスクをレンタル専門業者に移譲するもので、請負業者は資本を中核的なプロジェクト遂行に振り向けることができます。中小企業は、以前は予算オーバーであった高級機械にアクセスすることで、競争力を高めることができます。一方、レンタル会社は、より高い機器の回転率と、より迅速にフリートを更新する能力から利益を得て、厳しくなる排出規制へのコンプライアンスを確保します。

熟練オペレーターの不足がダウンタイムリスクを高める

2026年までに8万人以上の重機オペレーターが追加で必要になる一方、現在のオペレーターの41%が定年退職を迎えます。人手不足の現場では、レンタル機械を十分に活用できず、プロジェクトのスケジュールを膨張させ、レンタル利回りを低下させる。また、経験の浅いオペレーターに関連した安全事故も、保険料や修理費を引き上げています。大手レンタル会社は現在、シミュレーターを使用したトレーニングを提供しており、このトレーニングにより、新入社員研修が6カ月から7週間に短縮され、損害賠償請求が2桁減少したと評価されています。とはいえ、人材格差は、さらなる技術的熟練を必要とする先進的な電気自動車や水素モデルの迅速な配備を制限しています。

セグメント分析

2024年の世界の建設機械レンタル市場売上高の40.98%は土木機械が占めました。掘削機とバックホーローダーは、路盤、基礎、溝掘りの定番であり、繁忙期には稼働率が70%を超えることもあります。このクラスでは、電動ミニショベルがCAGR 8.81%を記録しており、都市部の騒音と排ガス規制によって後押しされています。

クレーンやテレハンドラーなどのマテリアルハンドリングユニットは、アジアや湾岸諸国での高層ビル拡張のため、二次的な重要性を与えられています。土木機械フリート全体のテレマティクス統合は、予知保全を強化し、それによって資産寿命を延ばし、顧客満足度指数を引き上げています。

アフターマーケット・サービスにも同様の変化が見られ、レンタル業者は、割高な日当を正当化するために、オペレーター・トレーニングや24時間365日の現場サポート契約をバンドルしています。大型のグレーダーやドーザーのデジタルツインは、摩耗パターンをシミュレートし、最適な交換サイクルを知らせるために試用されています。ブルドーザーの自律制御の改修と相まって、これらの進歩は生産性を一段と向上させることを約束するが、規制当局の受け入れ態勢は管轄区域によって異なります。そのため、フリートオーナーは、農村部の需要弾力性を監視しながら、稼働率の高い地下鉄プロジェクトを優先し、投資を分散させています。

2024年の内燃機関のシェアは85.74%を維持し、給油インフラとオペレーターの慣れが定着していることを裏付けています。しかし、政府が都市部の密集地帯でゼロ・エミッションを義務化するにつれて、建設機械レンタル市場は変貌を遂げつつあります。水素燃料電池プロトタイプは、2030年までの予測CAGRが16.99%と最も高く、素早い燃料補給とバッテリーシステムに比べて長いデューティサイクルによって支えられています。バッテリー電気モデルは、航続距離の不安が制限され、現場で一晩中充電が可能な小型掘削機とシザーリフトで最も急速に拡大しています。

ハイブリッドパワーシステムは、橋渡し技術として機能します。ユナイテッド・レンタルは、発電機とバッテリー蓄電パックを組み合わせた場合、燃料を最大80%節約し、コストを34%削減できると報告しています。しかし、導入には明確な残存価値の見通しが必要です。大容量リチウム・バッテリーのアフターマーケット価格が不透明なため、積極的なフリート展開が抑制されます。リスクを軽減するため、主要なレンタル業者はサブスクリプション・ベースのアップグレードを採用しており、技術や規制が変化した場合に迅速な切り替えを可能にしています。

建設機械レンタルレポートは、機器タイプ(土木機械(バックホーローダーなど)、その他)、駆動タイプ(ICエンジン、その他)、用途(住宅建設、その他)、レンタルチャネル(オフライン、オンライン)、サービスタイプ(短期レンタル、その他)、地域(北米、その他)で区分されています。市場予測は金額(米ドル)と数量(ユニット)で提供されます。

地域別分析

アジア太平洋地域は、中国の「一帯一路(the Belt and Road)」の延長、インドの記録的な資本支出、日本の着実な公共事業パイプラインに支えられ、2024年の世界レンタル収入の39.01%を占めました。中国のOEMは2024年に世界の電動建設機械出荷台数の75%を占め、東南アジアに積極的に輸出しています。インドの建設部門は2030年までにGDPに1兆米ドルを上乗せする勢いであり、大手レンタル会社による全国的な支店拡大に活力を与えています。日本は、2四半期にわたる機械受注の縮小から回復し、半導体工場への投資が拡大したため、2025年初頭に成長に転じた。

中東は、2030年までのCAGRが7.56%で最も急成長する地域です。サウジアラビアでは、リヤド地下鉄やNEOM都市プロジェクトを含むビジョン2030のパイプラインが、賃貸需要を年率12%以上の成長へと押し上げています。アラブ首長国連邦(UAE)も同様に、80億オーストラリアドルを投じたマサール・コミュニティのような大規模回廊や複合用途開発から恩恵を受けています。クレーンやテレハンドラーを専門とする企業は、高い稼働率と魅力的な利回りを活用するため、機材を湾岸に移転しています。

北米は健全なCAGR 6.58%を示しています。大規模なインフラ整備と堅調な民間産業建設が、安定した稼働率を下支えしています。欧州の成長率は5.30%と鈍化しているが、厳しいステージVディーゼル規制と自治体のゼロカーボン義務化により、低排出ガスレンタルの分野ではリードしています。南米は、輸送回廊の近代化と一次産品セクターの活性化により、CAGR 7.34%の成長を遂げました。アフリカの平均成長率は6.90%だが、資金調達へのアクセスと規制の明確化は市場によってまだばらつきがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- インフラ刺激策の大規模プロジェクトパイプライン

- 請負業者におけるCAPEXからOPEXへの移行

- 厳格なESG目標が電気レンタルを加速

- 従量課金制と成果ベースの契約モデル

- 新興市場におけるデジタルレンタルプラットフォームの爆発的な増加

- データ駆動型の車両最適化により顧客のROIを向上

- 市場抑制要因

- 複数ブランドのメンテナンスの複雑さ

- 熟練オペレーターの不足によりダウンタイムリスクが高まる

- OEMによる顧客直販レンタルのカニバリゼーション

- リチウム電池資産の残存価値の変動性

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(価値、10億米ドル)

- 機器別

- 土木機械

- バックホーローダー

- ローダー

- 掘削機

- ブルドーザー

- スキッドステアローダー

- その他の土木工事

- マテリアルハンドリング機器

- クレーン

- フォークリフト

- ダンプトラック

- テレハンドラー

- その他のマテリアルハンドリング

- コンクリートおよび道路建設機械

- 電力・エネルギー機器

- その他の機器

- 土木機械

- ドライブタイプ別

- ICエンジン

- ハイブリッド

- 電気

- 水素燃料電池

- 用途別

- 住宅建設

- 商業建設

- 工業/ 製造業

- インフラ(道路、橋、港)

- 鉱業と採石業

- 石油・ガス

- レンタルチャンネル

- オフライン(支店ベース)

- オンラインプラットフォーム

- サービスタイプ別

- 短期レンタル(1ヶ月未満)

- 中期賃貸(1~12か月)

- 長期レンタル(1年以上)

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他南米

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- United Rentals Inc.

- Ashtead Group plc(Sunbelt Rentals)

- Herc Rentals Inc.

- H&E Equipment Services Inc.

- Loxam

- Caterpillar Inc.(Cat Rental Store)

- Sumitomo Corp.

- Hitachi Construction Machinery Co. Ltd.

- Liebherr-International AG

- Kanamoto Co. Ltd.

- CNH Industrial N.V.

- HSS Hire Group plc

- Boels Rental

- Cramo Oyj

- Ahern Rentals

- Maxim Crane Works

- Ramirent

- Coates Hire

- Sarens n.v./s.a.

- MyCrane