|

市場調査レポート

商品コード

1437944

医療コーディング:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Medical Coding - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 医療コーディング:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 109 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

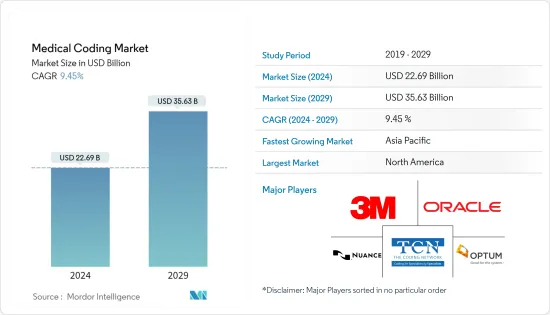

医療コーディング市場規模は2024年に226億9,000万米ドルと推定され、2029年までに356億3,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に9.45%のCAGRで成長します。

新型コロナウイルス感染症(COVID-19)のパンデミックは、世界中のヘルスケアシステムに大きな影響を与えました。 WHOによると、2020年 2月に、COVID-19(COVID-19が発動されました。また、2020年4月には、死因としてのCOVID-19の認定と分類(コーディング)に関する国際ガイドラインがWHOから7か国語で公表されました。さらに、メディケア・メディケイド・サービスセンター(CMS)は、COVID-19の検査と治療における医療請求とコーディングの側面を医療提供者が処理できるよう支援する最前線に立った。たとえば、2020年 3月にCMSは、新しい米国ヘルスケアCOVID-19システム(HCPCS)コードをリリースしました。)ガイドライン。したがって、新型コロナウイルス感染症の発生により、調査対象の市場に多くの変化が生じ、これらの変化は長期的に市場に影響を与えると予想されます。したがって、調査対象の市場は今後数年間で再びペースを取り戻すと予想されます。

市場成長の要因としては、コーディングサービスの需要の高まり、保険金請求に関連した詐欺や誤解を減らすための世界共通言語のニーズの高まり、病院の請求手続きの合理化に対する高い需要などが挙げられます。

コーディングサービスの需要は大幅に増加しています。たとえば、米国病院協会(AHA)の2022年の病院統計によると、米国のすべての病院での入院者数は約3,335万6,853人でした。したがって、調査対象の市場では医療請求業者や医療コーダーに対する需要が高く、それが医療コーディング市場の成長を促進すると予想されます。

さらに、より合理化された便利なコーディングおよび課金ソリューションに切り替える需要もあります。医療コーディングにより、医療施設間での統一文書化も可能になります。医療コーディング会社を利用すると、行政は施設内での治療の発生率と有効性を確認できます。これは、三次医療病院のような大規模な医療施設にとって特に重要です。頻繁な発売が市場を牽引すると予想されます。たとえば、2021年 3月に、Athenahealthは、臨床医のコーディング関連の作業を軽減し、最終的には臨床医の燃え尽き症候群を軽減できるEHRコーディングソリューションであるathenaOneメディカルコーディングソリューションを発売しました。

しかし、継続的に変化する規制、データセキュリティへの懸念、ヘルスケア分野における十分な装備を備えた情報技術(IT)専門家の不足などが、市場の成長を妨げると予想されます。

医療コーディング市場の動向

国際疾病分類(ICD)部門は、予測期間中に健全な成長を示すことが予想されます

国際疾病分類(ICD)セグメントは、予測期間中に大きなシェアを占めると予想されます。 ICDは、医療専門家が標準化された情報を世界中で共有できるようにする共通言語を提供します。これは、世界中の健康動向と統計を特定するための基盤であり、120,000を超えるコード化可能な用語に裏付けられた、傷害、病気、死因に関する約17,000の固有のコードが含まれています。コードの組み合わせを使用して、160万を超える臨床状況をコード化できるようになりました。 ICDは疫学、健康管理、臨床目的のための診断ツールと呼ばれ、WHOによって維持されています。したがって、慢性疾患の有病率の増加とICDの進歩により、この分野の成長が促進されると予想されます。

英国心臓財団(BHF)の2022年 1月の最新情報によると、英国では約400万人の男性と360万人の女性が心臓および循環器疾患を抱えて暮らしています。 ICDは疾患を分類するための診断コードの方法を提供するため、CVDの蔓延によりそのようなコードの必要性が生じ、これが市場セグメントの成長を促進すると予想されます。

さらに、ICDのバージョンは向上しており、新しいバージョンでは以前のバージョンよりも多くの情報が提供されるため、その使用量が増加すると予想されます。たとえば、WHOによる2022年 2月の更新によると、ICDの新バージョンであるICD-11が2022年 2月から発効しました。ICD-11は完全にデジタルであり、使いやすい新しい形式と多言語機能を備えており、感染の可能性を減らします。エラー。このデータベースは、90か国以上からの意見と医療提供者の前例のない関与に基づいて編集および更新されており、臨床医に課せられたシステムから、統計の記録と報告に幅広い用途に使用できる真に有効な臨床分類および用語データベースへの進化を可能にしています。健康について。

また、CMSによる2021年 10月の更新によると、新型COVID-19症の発生中に宣言された国家非常事態に対応して、CDC国立保健統計センターは6つの新しい診断コードを国際疾病分類、第10版、臨床医学分類に導入しました。修正(ICD-10-CM)。したがって、このセグメントは将来的に成長を記録すると予想されます。

北米は予測期間中に市場で大きなシェアを示すと予想されます

北米の医療コーディング市場は、この地域のさまざまな国における技術の進歩とヘルスケアインフラの改善により、予測期間中に大きなシェアを占めると推定されています。コーディングサービスに対する需要の高まりと、慢性疾患の増加による病院の請求手続きの合理化に対する高い需要が、この地域の市場プレーヤーによる戦略的取り組みと相まって、この地域の市場の成長を押し上げています。

地域のさまざまな国で慢性疾患の負担が増大していることも、市場の成長に貢献しています。たとえば、米国がん協会は、2022年に米国で新たにがんの症例が1,918,030件発生すると推定しており、これにより病院の請求手続きの合理化に対する需要が生まれ、それによって市場の成長が促進されると考えられます。

市場関係者による戦略的取り組みも市場の成長を推進しています。たとえば、2022年 10月、カナダの組織であるWELL Health Technologies Corp.は、Cloud Practice Inc.と3つの診療所をCloudMD Software &Services Inc.から買収する契約を締結しました。2022年 10月に、RBCはMDBilling.ca.を買収しました。カナダの医師の医療請求を自動化および簡素化するクラウドベースのプラットフォーム。

したがって、上記の要因により、北米地域で調査された市場は、予測期間中に大幅な成長が予想されます。

医療コーディング業界の概要

医療コーディング市場は、幅広いサービスを提供する国内外のプロバイダーが多数存在するため、適度な競争が続いています。すべてのプレーヤーは、市場での存在感を高めるためにさまざまな成長戦略を採用しています。調査対象となっている市場の主要企業には、3M、Nuance Communications Inc.、Oracle Corporation、Thecoding Network、Optum Inc.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 高まるコーディングサービスの需要

- 保険金請求に関連した詐欺や誤解を減らすために世界共通言語の必要性が高まる

- 病院の請求手続きの合理化に対する高い需要

- 市場抑制要因

- 医療コーディングに関連する規制の変更

- データセキュリティに関する懸念

- 適切な装備を備えたITプロフェッショナルの不足

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 分類体系別

- 国際疾病分類(ICD)

- ヘルスケア共通手順コードシステム(HCPCS)

- コンポーネント別

- 社内

- 外部委託

- エンドユーザー別

- 病院

- 診断センター

- その他のエンドユーザー

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- 3M Company

- Aviacode Inc.

- Dolbey Systems Inc.

- Maxim Health Information Services

- MRA Health Information Services

- Nuance Communications Inc.

- Optum Inc.

- Oracle Corporation

- Talix

- The Coding Network LLC

- Precyse Solutions LLC

- Access Healthcare

- Global Healthcare Resource

- Episource

第7章 市場機会と将来の動向

The Medical Coding Market size is estimated at USD 22.69 billion in 2024, and is expected to reach USD 35.63 billion by 2029, growing at a CAGR of 9.45% during the forecast period (2024-2029).

The COVID-19 pandemic significantly impacted healthcare systems across the world. As per the WHO, in February 2020, emergency codes were activated for the confirmed diagnosis of COVID-19 and clinical or epidemiological diagnosis (suspected or probable) of COVID-19. Also, in April 2020, the international guidelines for certification and classification (coding) of COVID-19 as the cause of death were published in seven languages by the WHO. Moreover, the Centers for Medicare and Medicaid Services (CMS) was at the forefront of helping providers handle the medical billing and coding aspect of COVID-19 testing and treatment. For instance, in March 2020, CMS released two Healthcare Common Procedure Coding System (HCPCS) codes that laboratories can use to bill for certain COVID-19 diagnostic tests, including those developed in-house according to the new United States Food and Administration (USFDA) guidelines. Hence, the COVID -19 outbreak led to many changes in the market studied, and these changes are expected to have an impact in the long term on the market. Thus, the market studied is expected to regain its pace in the upcoming years.

The factors responsible for the growth of the market include the escalating demand for coding services, the rising need for a universal language to reduce frauds and misinterpretations associated with insurance claims, and the high demand for streamlining hospital billing procedures.

The demand for coding services is significantly increasing. For instance, as per the American Hospital Association's (AHA) Hospital Statistics 2022, there were around 33,356,853 admissions in all the hospitals in the United States. Thus, there is a high demand for medical billers and coders in the market studied, which, in turn, is expected to propel the growth of the medical coding market.

Moreover, there is also a demand to switch to a more streamlined and convenient coding and billing solution. Medical coding also enables uniform documentation between medical facilities. Medical coding companies enable administrations to look at the incidence and effectiveness of treatments in their facility. This is particularly important to large medical facilities, like tertiary-care hospitals. Frequent launches are expected to drive the market. For instance, in March 2021, Athenahealth launched the athenaOne Medical Coding Solution, an EHR coding solution that could mitigate clinician coding-related work and ultimately reduce clinician burnout.

However, continuously changing regulations, data security concerns, and the lack of adequately equipped information technology (IT) professionals in the healthcare sector are expected to hinder the growth of the market.

Medical Coding Market Trends

The International Classification of Diseases (ICD) Segment is Expected to Show Healthy Growth Over the Forecast Period

The International Classification of Diseases (ICD) segment is expected to hold a significant share during the forecast period. ICD provides a common language that allows health professionals to share standardized information across the world. It is the foundation for identifying health trends and statistics worldwide, containing around 17,000 unique codes for injuries, diseases, and causes of death, underpinned by more than 120,000 codable terms. Using code combinations, more than 1.6 million clinical situations can now be coded. The ICD is referred to as a diagnostic tool for epidemiology, health management, and clinical purposes, and it is maintained by the WHO. Thus, the increased prevalence of chronic diseases and the advances in ICD are expected to boost the growth of this segment.

According to the January 2022 update of the British Heart Foundation (BHF), around 4 million males and 3.6 million females live with heart and circulatory diseases in the United Kingdom. As the ICD provides a method of diagnostic codes for classifying diseases, the high prevalence of CVDs creates the need for such codes, which is expected to drive the growth of the market segment.

Moreover, with the improving versions of ICD, its usage is expected to rise as the newer versions provide more information than the previous ones. For instance, as per a February 2022 update by the WHO, the new version of ICD, ICD-11, was effective from February 2022. ICD-11 is entirely digital with a new user-friendly format and multilingual capabilities that reduce the chance of error. It has been compiled and updated with input from over 90 countries and unprecedented involvement of health-care providers, enabling evolution from a system imposed on clinicians into a truly enabling clinical classification and terminology database that serves a broad range of uses for recording and reporting statistics on health.

Also, as per an October 2021 update by the CMS, in response to the national emergency that was declared during the COVID-19 outbreak, CDC's National Center for Health Statistics implemented six new diagnosis codes into the International Classification of Diseases, Tenth Revision, Clinical Modification (ICD-10-CM). Hence, this segment is expected to record growth in the future.

North America is Expected to Show Large Share in the Market Over the Forecast Period

The medical coding market in North America is estimated to hold a large share during the forecast period, owing to technological advancements and improved healthcare infrastructure in various countries in this region. Escalating demand for coding services and the high demand for streamlining hospital billing procedures due to the growing number of chronic diseases, coupled with strategic initiatives taken by the market players in the region, boost the growth of the market in the region.

The growing burden of chronic diseases in the different countries of the region is also contributing to the growth of the market. For instance, the American Cancer Society estimates that there will be 1,918,030 new cases of cancer in the United States in 2022, which would create demand for streamlining hospital billing procedures and thereby drive the growth of the market.

The strategic initiatives taken by the market players are also propelling the growth of the market. For instance, in October 2022, WELL Health Technologies Corp., a Canadian organization, entered into an agreement to acquire Cloud Practice Inc. and three clinics from CloudMD Software & Services Inc. In October 2022, RBC acquired MDBilling.ca., which is a cloud-based platform that automates and simplifies medical billing for Canadian physicians.

Thus, owing to the abovementioned factors, the market studied in the North American region is expected to project significant growth over the forecast period.

Medical Coding Industry Overview

The medical coding market is moderately competitive due to the presence of many local and international providers offering a wide array of services. All the players are adopting various growth strategies to enhance their market presence. Some of the key players in the market studied are 3M, Nuance Communications Inc., Oracle Corporation, The Coding Network, and Optum Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Demand for Coding Services

- 4.2.2 Rising Need for a Universal Language to Reduce Frauds and Misinterpretations Associated with Insurance Claims

- 4.2.3 High Demand to Streamline Hospital Billing Procedures

- 4.3 Market Restraints

- 4.3.1 Changing Regulations Related to Medical Coding

- 4.3.2 Data Security Concerns

- 4.3.3 Lack of Adequately Equipped IT Professionals

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By Classification System

- 5.1.1 International Classification of Diseases (ICD)

- 5.1.2 Healthcare Common Procedure Code System (HCPCS)

- 5.2 By Component

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Diagnostic Centers

- 5.3.3 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 3M Company

- 6.1.2 Aviacode Inc.

- 6.1.3 Dolbey Systems Inc.

- 6.1.4 Maxim Health Information Services

- 6.1.5 MRA Health Information Services

- 6.1.6 Nuance Communications Inc.

- 6.1.7 Optum Inc.

- 6.1.8 Oracle Corporation

- 6.1.9 Talix

- 6.1.10 The Coding Network LLC

- 6.1.11 Precyse Solutions LLC

- 6.1.12 Access Healthcare

- 6.1.13 Global Healthcare Resource

- 6.1.14 Episource