|

市場調査レポート

商品コード

1641944

ポリウレタン添加剤:市場シェア分析、産業動向、統計、成長予測(2025~2030年)Polyurethane Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ポリウレタン添加剤:市場シェア分析、産業動向、統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

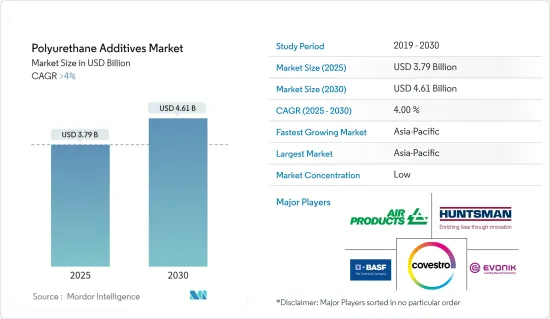

ポリウレタン添加剤の市場規模は2025年に37億9,000万米ドルと推計され、2030年には46億1,000万米ドルに達すると予測され、予測期間(2025~2030年)のCAGRは4%を超えると予想されます。

COVID-19の大流行により、市場はマイナスの影響を受けました。生産と移動が減速し、業界は封じ込め対策と経済的混乱により生産の延期を余儀なくされたからです。現在、市場はパンデミックから回復しています。市場は2022年にはパンデミック以前の水準に達し、今後も安定した成長が見込まれます。

主なハイライト

- 建設業界におけるポリウレタン需要の高まりが添加剤の消費を促進すると思われます。最大の用途のひとつは、硬質PUフォームを壁や屋根の断熱材、断熱パネル、ドアや窓周りの隙間充填材として使用することです。これによって市場の成長が促進されます。

- その反面、代替添加剤はPU添加剤と同じ用途にも使用できます。例えば、シリコン添加剤とアクリル添加剤は、どちらもPUフォームに対して有効な添加剤です。

- より革新的で費用対効果の高い添加剤に対する需要の高まりは、今後の市場にとって好機となると予測されます。

- アジア太平洋地域が最大のシェアを占め、予測期間中に最も高い成長率を記録すると予想されます。

ポリウレタン添加剤市場の動向

自動車産業からの需要の増加

- 自動車産業は、PU材料の多様な用途を示す最良の例の一つです。ほぼすべてのタイプのPU製品が自動車エンドユーザー産業で使用されています。

- 柔軟なPU発泡体は、座席、ヘッドレスト、アームレスト、HVAC、その他の自動車用内装システム、旅客機、列車、バスなどに使用されています。PUコーティングは、自動車の外装に高い光沢、耐久性、耐傷性、耐腐食性を提供します。PUコーティングはまた、フロントガラスや窓のグレージングにも使用され、強度を高め、曇り止めを提供します。

- PUエラストマーはタイヤのパンクを防ぎ、ショックアブソーバーなどの成形部品にも使用されています。熱可塑性PU材料は、外装ボディー部品、トランクライナー、アンチロックブレーキシステム、タイミングベルト、燃料ラインなど、多くの自動車部品の製造に使用されています。PUエラストマーのユニークな特性は、ガスケット、Oリング、その他のシールに独占的に使用されています。

- 座席は、自動車産業におけるPUの最大の用途です。多くの自動車用シートメーカーは、バイオベースのポリオールを使用した製品を求めています。しかし、世界のほとんどのPU市場では、「グリーン」PUの市場浸透はまだ始まったばかりです。

- 世界全体では、90%以上の自動車が1液型PUシーラントを使用してフロントガラスとリアガラスを接着して生産されています。自動車産業は、反応射出成形(RIM)PU部品の最大のエンドユーザー産業です。RIMは、重量やかさを増やすことなく、自動車のフェンダー、バンパー、スポイラーの衝撃吸収を最大化するために使用されます。

- 国際自動車製造者機構(OICA)によると、2022年には世界中で約8,502万台の自動車が生産されました。この数字は、前年と比較して約6%増加したことになります。2022年には中国、日本、ドイツが自動車と商用車の最大の生産国であり、これがPU添加剤市場を牽引しています。

- しかし、ガソリン車やディーゼル車による環境汚染への懸念が高まる中、電気自動車の生産は今後5年間で回復すると予想されます。このことが、予測期間中に調査された市場の需要を押し上げる可能性が高いです。

- 2023年8月、ミシガン州を拠点とする世界テクノロジー企業AltairとCenter for Automotive Research(CAR)は、内装製品用ポリウレタンフォームが評価され、2023年のEnlighten賞のFuture of Lightweighting部門にMarelliを選出しました。

- さらに、世界の電気自動車市場は大幅に拡大しており、これが研究対象の市場に利益をもたらしています。例えば、2022年には、バッテリー電気自動車(BEV)とプラグインハイブリッド電気自動車(PHEV)が世界中で約1,050万台販売され、前年の677万台に比べて55%の成長率を記録しました。

- 上記のすべての要因が、予測期間中の市場を牽引すると予想されます。

中国がアジア太平洋地域を支配する見込み

- アジア太平洋地域では、中国がGDPで最大の経済大国です。中国のGDP値は2022年の世界経済の7.73%を占め、GDP成長率は前年比3%です。

- 中国は世界でも有数の大国であり、その成長において建設部門は他のほとんどすべての部門を圧倒しています。2022年、建設産業は中国の国内総生産の約6.9%を占め、中国の建設産業の付加価値は前年比で約5.5%増加しました。

- 中国における家具製造業の急成長は、国内需要の増加に加え、海外市場からの大きな需要が大きな要因となっています。

- 中国は2022年の世界の家具生産量のほぼ53%を占めました。国内需要の増加と欧州諸国への輸出により、生産量はさらに急増しました。

- OICAによると、中国は2009年以来、世界最大の自動車製造国であり自動車市場です。中国の年間自動車生産台数は世界の自動車生産台数の32%以上を占め、これはEUや米国と日本を合わせた生産台数を上回る。

- しかし、同国における電気自動車の人気は、今後数年間でPU添加剤の需要を促進すると予想されます。中国政府は、2025年までに最低5,000台、2030年までに100万台の燃料電池電気自動車を導入する計画です。政府が電気自動車、ハイブリッド車、燃料電池車の利用を促進していることは、予測期間中の市場調査を促進すると予想されます。

- このような要因により、同国ではポリウレタン添加剤の需要が増加すると予想されます。

ポリウレタン添加剤産業の概要

ポリウレタン添加剤市場は、その性質上、部分的に断片化されています。主なプレーヤー(順不同)としては、Evonik Industries AG、Air Products Inc.、Covestro AG、Huntsman International LLC、BASF SEなどが挙げられます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 建設業界におけるポリウレタン需要の増加

- 自動車産業からの需要増加

- 持続可能なポリウレタン製品に対する需要の高まり

- 抑制要因

- 代替添加剤の入手可能性

- 厳しい政府規制

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(金額ベース市場規模)

- タイプ別

- 発泡剤

- 触媒

- 難燃剤

- 界面活性剤

- その他添加剤(充填剤、乳化剤、架橋剤)

- 用途別

- 接着剤およびシーラント

- コーティング剤

- 軟質発泡成形品

- 硬質フォーム

- その他の用途(エラストマー、繊維、複合材料、医療機器)

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Air Products Inc.

- Covestro AG

- BASF SE

- Dow

- GEO Specialty Chemicals Inc.

- Huntsman International LLC

- Eastman Chemical Company

- Evonik Industries AG

- Momentive Performance Materials Inc.

- KAO Corporation

- Specialty Products Inc.

- Tosoh Corporation

第7章 市場機会と今後の動向

- より革新的で費用対効果の高い添加剤への需要の高まり

- その他の機会

The Polyurethane Additives Market size is estimated at USD 3.79 billion in 2025, and is expected to reach USD 4.61 billion by 2030, at a CAGR of greater than 4% during the forecast period (2025-2030).

The market was negatively impacted by the COVID-19 pandemic as there was a slowdown in production and mobility wherein industries were forced to delay their production due to containment measures and economic disruptions. Currently, the market has recovered from the pandemic. The market reached pre-pandemic levels in 2022 and is expected to grow steadily in the future.

Key Highlights

- The rising demand for polyurethane in the construction industry will likely propel additives' consumption. One of the largest applications is the use of rigid PU foam as wall and roof insulation, insulated panels, and gap fillers for the space around doors and windows. Thereby augmenting the market's growth.

- On the flip side, the alternative additives can be used in some of the same applications as PU additives. For example, silicon additives and acrylic additives are both effective additives against PU foams.

- The increasing demand for more innovative and cost-effective additives is projected to act as an opportunity for the market in the future.

- The Asia-Pacific region is expected to account for the largest share and register the highest growth rate over the forecast period.

Polyurethane Additives Market Trends

Increasing Demand from the Automotive Industry

- The automotive industry provides one of the best examples of the diverse applications of PU materials. Nearly every type of PU product is used in the automotive end-user industry.

- Flexible PU foams are used in seating, headrests, armrests, HVAC, and other interior systems for automotive, like in airliners, trains, and buses. PU coatings provide a vehicle's exterior with high gloss, durability, scratch resistance, and corrosion resistance. PU coatings are also used for glazing windshields and windows, increasing strength and providing fog resistance.

- PU elastomers protect against tire punctures and are used in other molded components, such as shock absorbers. Thermoplastic PU materials are used to manufacture many automotive parts, including exterior body parts, trunk liners, anti-lock brake systems, timing belts, and fuel lines. The unique properties of PU elastomers contribute to their exclusive usage in gaskets, O-rings, and other seals.

- Seating is the largest application of PU in the automotive industry. Many automotive seating manufacturers demand products made with bio-based polyols. However, the market penetration of "green" PU is still emerging in most global PU markets.

- Globally, more than 90% of automobiles are produced with bonded windshields and rear windows using one-component PU sealants. The automotive industry is the largest end-user industry for reaction injection molding (RIM) PU parts. RIM is used to maximize the shock absorption of vehicle fenders, bumpers, and spoilers without adding weight or bulk.

- In 2022, according to the Organisation Internationale des Constructeurs d'Automobiles (OICA), around 85.02 million motor vehicles were produced worldwide. This figure translates into an increase of around 6% compared with the previous year. China, Japan, and Germany were the largest producers of cars and commercial vehicles in 2022, which is driving the PU additive market.

- However, with growing concerns about environmental pollution from petrol- and diesel-based vehicles, the production of electric vehicles is expected to pick up over the next five years. This is likely to drive the demand in the market studied over the forecast period.

- In August 2023, Global technology company Altair and the Center for Automotive Research (CAR), both based in Michigan, named Marelli as the 2023 Enlighten award winner in the Future of Lightweighting category for its polyurethane foam for interior products.

- Further, the global electric vehicle market is expanding significantly, which is benefitting the market studied. For instance, in 2022, around 10.5 million units of battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) were sold across the globe, witnessing a growth rate of 55% compared to 6.77 million units sold in the previous year.

- All the factors above are expected to drive the market during the forecast period.

China is Expected to Dominate the Asia-Pacific Region

- In Asia-Pacific, China is the largest economy in terms of GDP. The GDP value of China represents 7.73% of the world economy in 2022 and has a 3% GDP growth compared to the previous year.

- China is one of the largest countries in the world, where the construction sector dominates almost all other sectors in growth. In 2022, the construction industry accounted for around 6.9% of China's gross domestic product, and the value added to the Chinese construction industry increased by about 5.5% compared to the previous year.

- The rapid growth of the furniture manufacturing industry in the country is majorly fueled by the increasing domestic demand, coupled with significant demand from the foreign market.

- China accounted for almost 53% of the global furniture production in 2022. The production was further increased rapidly due to the increase in domestic demand and exports to European countries.

- According to the OICA, China remains the world's largest automotive manufacturing country and automotive market since 2009. Annual vehicle production in China accounted for more than 32% of worldwide vehicle production, which exceeds that of the European Union or that of the United States and Japan combined.

- However, the popularity of electric vehicles in the country is expected to propel the demand for PU additives in the coming years. The Chinese government plans to have a minimum of 5,000 fuel-cell electric vehicles by 2025 and 1 million by 2030. The government promoting the use of electric, hybrid, and fuel-cell electric vehicles is expected to drive the market studied during the forecast period.

- Such factors are expected to increase the demand for polyurethane additives in the country.

Polyurethane Additives Industry Overview

The polyurethane additives market is partially fragmented in nature. The major players (not in any particular order) include Evonik Industries AG, Air Products Inc., Covestro AG, Huntsman International LLC, and BASF SE. among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Rising Demand for Polyurethane in the Construction Industry

- 4.1.2 Increasing Demand from the Automotive Industry

- 4.1.3 Growing demand for sustainable Polyurethane products

- 4.2 Restraints

- 4.2.1 Availability of Alternative Additives

- 4.2.2 Stringent Government Regulations

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Blowing Agents

- 5.1.2 Catalysts

- 5.1.3 Flame Retardants

- 5.1.4 Surfactants

- 5.1.5 Other Additives( Filler, Emulsifiers, and Crosslinking Additives)

- 5.2 Application

- 5.2.1 Adhesives and Sealants

- 5.2.2 Coatings

- 5.2.3 Flexible Molded Foams

- 5.2.4 Rigid Foams

- 5.2.5 Other Applications (Elastomers, Fibers, Composites, and Medical Devices)

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Air Products Inc.

- 6.4.2 Covestro AG

- 6.4.3 BASF SE

- 6.4.4 Dow

- 6.4.5 GEO Specialty Chemicals Inc.

- 6.4.6 Huntsman International LLC

- 6.4.7 Eastman Chemical Company

- 6.4.8 Evonik Industries AG

- 6.4.9 Momentive Performance Materials Inc.

- 6.4.10 KAO Corporation

- 6.4.11 Specialty Products Inc.

- 6.4.12 Tosoh Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Demand for More Innovative and Cost-effective Additives

- 7.2 Other Opportunities