整形外科用装具およびサポーター:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Orthopedic Braces And Supports - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1907354

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

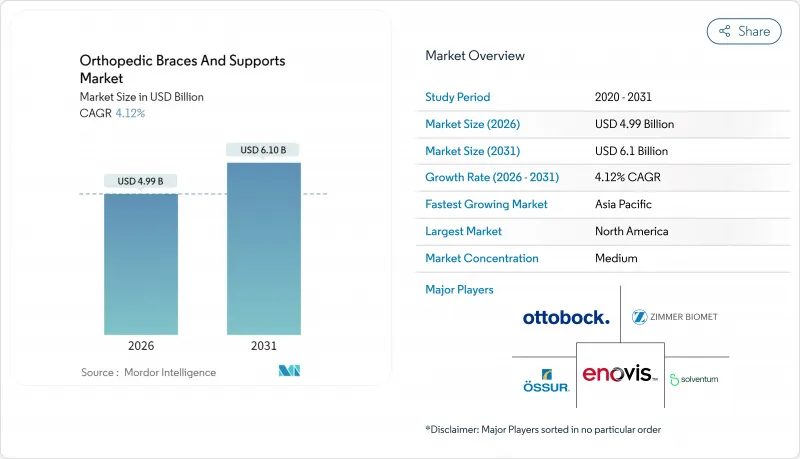

整形外科用装具およびサポーター市場は、2025年の47億9,000万米ドルから2026年には49億9,000万米ドルへ成長し、2026年から2031年にかけてCAGR4.12%で推移し、2031年までに61億米ドルに達すると予測されております。

着実な拡大は、高齢化に伴う骨折発生率の上昇、予防的装具装着への認知度拡大、在宅リハビリテーションプログラムへの移行に起因しております。AI搭載アライメントシステムから患者特化型3Dプリント技術に至る技術進歩により、整形外科用装具およびサポーター市場は汎用品製造から付加価値の高いスマートデバイスへと移行しています。特に北米における非外科的治療段階を包括する償還制度改革は、入院期間短縮につながる費用対効果の高い装具の需要を後押ししています。主要企業がイノベーションを重視する一方、低コストのアジア製品による価格圧力に直面しているため、競合の激しさは中程度に留まっています。

世界の整形外科用装具およびサポーター市場動向と洞察

骨折発生率の上昇

遠位橈骨骨折、指骨折、股関節骨折の発生率は、それぞれ10万人年当たり212件、117.1件、112.9件であり、固定装置に対する長期的な需要を裏付けています。装具を用いた早期可動化は障害リスクを低減し、費用対効果の高い治療を支えます。これは、慢性的な骨折後遺症を管理する支払者にとって極めて重要な提案です。

筋骨格系疾患の増加傾向

17億人以上が筋骨格系の疾患を抱えており、腰痛が整形外科受診の26%を占めています。腰部装具と理学療法を組み合わせた12週間の治療により、疼痛スコアは6.28から3.96に低下し、オズウェストリー指数による機能評価は46.56から33.13に改善しました。したがって、長期間の装着に適した快適で調整可能な装置への需要が高まっています。

軽傷への軽視

治療の遅れは依然として一般的であり、インドの農村部では外傷後の受診が遅れる子どもが71%に上り、しばしば予後を悪化させています。このような行動は予防的装具の販売を抑制し、長期的な成長を阻害しています。

セグメント分析

整形外科用装具およびサポーター市場において、2025年の収益の55.78%を下肢用装具が占めました。この主導的地位は、膝・足首・股関節の負傷率の高さに起因しています。膝装具が最大のサブカテゴリーを形成しており、前十字靭帯損傷は年間10万人あたり17.5件発生しています。スポーツ医学の需要は変形性関節症の管理と交差し、関節置換手術を遅らせるアンローダー設計の普及が進んでいます。3Dプリント足首サポートや調整可能な足部装具は、小売クリニックでの迅速なデジタルスキャン技術により、ランニングやハイキングコミュニティに浸透しつつあります。かつて術後プロトコル専用だった股関節外転装具は、現在では長期療養施設における高齢者の転倒予防プログラムで予防的使用が見られます。

脊椎装具は依然としてCAGR5.05%で最も成長が速いカテゴリーであり、2024年にFDA承認を得た神経刺激機能付き固定刺激装置の恩恵を受けています。慣性センサーを内蔵したスマートベルトは、姿勢分析データを臨床医に提供し、リハビリプログラムの質向上に貢献します。上肢用装具は数量こそ少ないもの、ハイテク職場における反復性ストレス障害削減のための人間工学的取り組みに後押しされています。ウェアラブルセンサーの統合により、装具は受動的なサポートから、動作修正を促す能動的なコーチへと変貌し、コンプライアンス向上を促進します。全体として、装具製品の構成は接続型ソリューションへ移行しつつあり、整形外科用装具およびサポーター市場がパーソナライズされたデータ豊富なケアへ向かう軌道を強化しています。

2025年時点では病院が収益シェアの50.63%を占めており、整形外科・外傷分野における広範な手術能力と統合購買契約を反映しています。資本予算により年間で多量の装具調達が可能であり、臨床的に支持されたブランドを優先する価値分析委員会の下で行われることが一般的です。しかしながら、成長は整形外科・外傷センターに偏っており、患者が専門的な技術と迅速な回復経路を求めることから、2031年まで年率5.18%の拡大が見込まれます。これらのセンターは患者の身体計測値に適合する在庫システムに投資し、フィット感の向上と在庫評価損の削減を図っています。

外来手術センターが成長を加速させております。Zimmer BiometとCBREの提携などにより、新たな外来施設が拡大し、変化する手術件数を捕捉しております。在宅医療環境も導入を促進しており、2023年には270万人の受益者をカバーしたメディケア資金が後押ししております。遠隔監視による装具のフィッティングと調整プロトコルにより、費用対効果の高いフォローアップケアが可能となっております。多様なエンドユーザーチャネルが相まって、整形外科用装具・補助具市場は病院中心の景気循環から保護されております。

地域別分析

北米は2025年の収益の40.21%を占め、非外科的整形外科治療を償還する堅調な保険適用とCMSプログラムが基盤となっています。米国は先進的な製造技術により地域での優位性を維持し、2024年には29億米ドルの整形外科製品をアジアへ輸出しました。カナダでは公的資金による人工関節置換術パッケージの導入が拡大し、メキシコではセグロ・ポプラーラ(国民保険)の拡充によりアクセスが拡大しています。成熟した普及率にもかかわらず、AIを活用したアライメント技術や遠隔リハビリテーションといった継続的な技術革新により、整形外科用装具およびサポーター市場は中程度の単一桁成長を維持しています。

欧州は、国民皆保険制度と医療機器規則(MDR)に基づく厳格な市販後調査によって形成された確固たる基盤を維持しています。ドイツはブレーメンとバイエルンのクラスターを活用したスマート整形外科研究により、地域のイノベーション拠点としての役割を果たしています。英国の医薬品医療製品規制庁(MHRA)はMDRのスケジュールに沿いながら独自の審査経路を確立し、ブレグジット後も供給の継続性を確保しています。南欧諸国では予算制約に対応するため、非侵襲的筋骨格ケアへの資金配分が増加傾向にあります。この結果、欧州では厳格な臨床的・経済的価値基準を満たす、エビデンスに基づく高品質医療機器への需要が引き続き高い水準を維持しています。

アジア太平洋地域は、中産階級の拡大、政府保険の導入、スポーツ参加率の上昇を背景に、2031年までCAGR5.26%という最速の伸びを示します。中国では2025年に45万5千件の関節置換術と100万件の骨折治療が予測され、リハビリテーション中の装具需要を牽引します。日本は超高齢社会に対応するため、スマートリハビリテーション技術の採用を加速させております。一方、オーストラリアでは広大な地域をカバーする遠隔装具フォローアップを含む遠隔医療プログラムに資金を投入しております。インド、タイ、マレーシアでは輸入依存度を低減するため国内製造を奨励しており、合弁事業の機会が開かれております。通貨変動や入札ベースの調達により価格設定上の課題は生じておりますが、数量面での機会により、整形外科用装具およびサポーター市場は地域全体で高い魅力を維持しております。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 骨折発生率の増加

- 筋骨格系疾患の増加傾向

- 増加する交通事故およびスポーツ傷害

- スマート/3Dプリント製サポートへの技術的移行

- 新型コロナウイルス感染症後の在宅リハビリテーション需要の急増

- 非外科的整形外科治療に対する一括償還

- 市場抑制要因

- 軽微な負傷への軽視

- 次世代装具に対する認知度の不足

- 未検証のDTC電子商取引用装具に対する医師の採用率が低い

- アジアからのコモディティ輸入品による価格圧力

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品別

- 下肢用装具およびサポーター

- 足首・足

- 股関節

- 膝

- 脊椎装具およびサポーター

- 上肢用装具およびサポーター

- 肘

- 手と手首

- 肩

- その他

- 下肢用装具およびサポーター

- エンドユーザー別

- 病院

- 整形外科・外傷センター

- 在宅ケア環境

- その他

- 用途別

- 靭帯損傷

- 予防医療および予防的使用

- 術後リハビリテーション

- 変形性関節症の管理

- その他

- 年齢層別

- 小児

- 成人

- 高齢者

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Solventum

- Essity(BSN Medical)

- DJO LLC(Enovis)

- Ossur

- Ottobock

- Zimmer Biomet

- Bauerfeind

- Medi GmbH

- DeRoyal Industries

- Bird & Cronin

- Frank Stubbs

- ALCARE

- Becker Orthopedic

- Thuasne

- Tynor Orthotics

- Rehan Health

- Breg Inc.

- United Ortho

- OrthoPediatrics Corp.

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日