|

市場調査レポート

商品コード

1850266

ネットワークオートメーション:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Network Automation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ネットワークオートメーション:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月23日

発行: Mordor Intelligence

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

概要

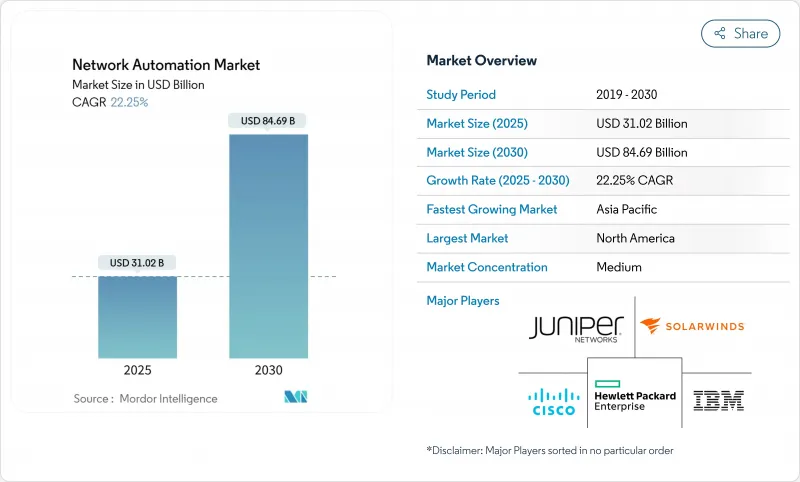

ネットワークオートメーション市場規模は、2025年に310億2,000万米ドル、2030年には846億9,000万米ドルに達すると推定され、CAGRは22.25%と勢いがあります。

成長を後押ししているのは、広大なハイブリッド環境の管理、運用コストの削減、ポリシー主導のオーケストレーションによる設定ミスの排除を目指す企業です。クラウドファーストの移行、SD-WANの広範な採用、5Gネットワークスライシングへの投資の急増は、自動化導入の完璧な背景を作り出しています。同時に、AI対応の自己修復機能は、基本的なスクリプト作成から自律的な運用へと期待を変えつつあります。インテントベースのネットワーキングとマルチクラウドの可視性をシームレスに融合させるベンダーが最速で前進する一方、顧客はロックインを防ぎ、DevOps統合を加速させるオープンAPIを優先しています。

世界のネットワークオートメーション市場の動向と洞察

データセンター・ネットワークのアップグレード急増

AIワークロードの急増により、事業者はGPUクラスタを効率的に相互接続するために400G、800G、そして間もなく1.6Tのスイッチング・ファブリックの導入を余儀なくされています。アマゾンがペンシルベニア州とノースカロライナ州に300億米ドルを投じたことは、ハイパースケーラーが巨大なリーフスパインファブリックを調整するために高度な自動化をいかに利用しているかを明確に示しています。ハイパースケール以外の企業もアップグレードを進めています。従来の10Gリンクではデータ集約的な分析がサポートされなくなり、光レイヤーとパケットレイヤーのインテント・ベースのコンフィギュレーションに対する需要が加速しています。オペレータは、人によるレビューなしに修復ワークフローをトリガーするソフトウェア定義の遠隔測定を導入しています。光ファイバープロバイダーのZayoは、2030年までにAIデータセンターの容量が倍増するという自信を反映し、このアップグレードサイクルに沿った長距離拡張に40億米ドルを計上しました。

IoTとコネクテッドデバイスの普及

工場フロアでは現在、確定的なレイテンシーを要求する何千ものセンサーがホストされており、管理者は手動によるVLANプロビジョニングをクローズドループのセグメンテーションに置き換えることを余儀なくされています。エリクソンの南京工場では、500台のドライバーをLTE-Mで接続した後、12ヶ月でROIを達成し、年間メンテナンス費用を1万米ドル削減しました。ハネウェルはベライゾンの5Gを導入し、技術者の訪問をなくし、グリッド予測を改善するリモート・メータリングを可能にしています。このような導入は、プログラマブル・ネットワークだけが効果的に取り締まることができるデバイス数とマイクロフローを増加させる。APAC全域でスマートシティとグリッド・プロジェクトが拡大する中、ネットワークオートメーション市場は、リアルタイム・トラフィック・エンジニアリングと迅速なポリシー普及への継続的な投資から利益を得ています。

オートメーションに精通したエンジニアの不足

Atomitechの2025年調査によると、75%がすでにインシデントトリアージにAIを導入しているにもかかわらず、運用スタッフの92.2%がスキル不足に悩んでいます。自動化の専門知識は現在、Python、RESTful API、Infrastructure-as-Codeに及んでおり、従来のCCNAレベルの管理者は取り残されています。企業は社内トレーニングを加速させ、大学と提携しているが、学習曲線はプロジェクトを遅らせ、賃金を高騰させています。半導体の人材不足は、高性能な自動化パイプラインを支える特殊なNICとアクセラレータのために、ギャップを深めています。ベンダーは、ローコード・オーケストレーションとGenAIコパイロットで対応しているが、採用はまだ、需要に見合うほど急成長していない労働力プールにかかっています。

セグメント分析

ハイブリッドアーキテクチャは2024年に148億米ドルをもたらし、ネットワークオートメーション市場シェアの47.6%を占め、2030年に向けて22.9%のCAGRで拡大します。ハイブリッド・ミックスにより、企業は固定シャーシ・スイッチへのサンク投資を維持しながら、バーストするクラウド・ワークロード向けに仮想ファブリックをオーバーレイできます。初期の移行はエッジデバイスの自動プロビジョニングに重点を置き、その後コアでスパインリーフポリシーの自動化が行われます。金融トレーディングデスクや産業プラントでは、レイテンシに敏感な機能のために決定論的な非仮想リンクを維持しており、物理的な資産が耐えられる理由を示しています。同時に、仮想オーバーレイはマイクロサービスのトラフィックを運び、変更ウィンドウを数日から数分に短縮します。

ハイブリッドの導入はまた、自動化されたフォールトドメインの背後にあるレガシーリタイアメントを段階的に進めることで、障害リスクを軽減します。デンソーは、Cisco DNA Centerを使用して、生産を停止することなく400の工場を更新し、イベント・ドリブン・テンプレートが大陸をまたいだ同時ファームウェア・リフレッシュをどのように処理するかを示しています。サービス・プロバイダーは、物理ノードと仮想ノードの両方にパフォーマンス・テレメトリーを組み込み、SLA違反を未然に防ぐAIエンジンに供給しています。その結果、ネットワークオートメーション市場は、顧客がハイブリッドエステート全体でコントローラを拡張するにつれて、経常的なライセンス収益を記録します。

ソリューションは2024年の売上高の69.3%、215億米ドルに相当するが、サービスのCAGRは22.7%と成長が加速しています。企業はコンフィギュレーション、アシュアランス、アナリティクスに及ぶオーケストレーション・スイートを購入するが、成功するかどうかはカスタマイズされたプレイブックにかかっており、サービス拡大に拍車をかけています。インテント・ベースのエンジンには、トポロジー・ディスカバリー、ポリシー・モデリング、ITSMプラットフォームとの統合が必要だが、多くの社内チームはこの作業を専門家に委ねています。

プロフェッショナル・サービスは、アドバイザリー、構築、マネージド・オペレーションの3つに分類されます。Telecom ItaliaはItentialと組み、サービスのロールアウトを70%短縮し、インテグレーターがドメイン固有のワークフローをスクリプト化する共同イノベーションを実証しています。一方、デプロイ後のマネージド・サービスは、定期的なコンプライアンス・チェックとパッチの自動化を収益化します。コンサルティングを手掛けるベンダーは、導入時間を短縮するベストプラクティス・ライブラリをパッケージ化することで差別化を図り、ソフトウェア基盤を強化し、サブスクリプションの更新を促進します。

ネットワークオートメーション市場は、ネットワークインフラ(物理、仮想、ハイブリッド)、コンポーネント(ソリューション、サービス)、導入形態(クラウド、オンプレミス)、組織規模(大企業、中小企業)、エンドユーザー産業(ITおよび通信、銀行および金融サービスなど)、地域別に区分されます。市場予測は金額(米ドル)で提供されます。

地域別分析

北米は2024年の売上高の27.5%を占め、継続的なコンプライアンス自動化を求めるハイパースケールクラウド事業者や防衛機関が中心となっています。Amazonの300億米ドルを投じたインフラ構築はスケールメリットを実証し、米国海兵隊の「Comply-to-Connect」プログラムは95%のパッチ適用を成功させ、監査要員をより価値の高い業務に解放した。ベンチャー企業のエコシステムは、地域のスタックをさらに充実させ、イノベーション・サイクルを短縮しています。

アジア太平洋地域は最も急速に成長しており、インダストリー4.0への取り組みと拡大する5Gの足跡を背景に、2030年までCAGR 22.4%で拡大します。ソフトバンクは、日本のコングロマリットのマルチクラウド接続を管理するネットワークオートメーションに関連するAIコンピューティングに9億6,000万米ドルをコミットしました。一方、NTTはAIを使用した自律的な5G最適化をテストしており、通信事業者が自動化を単なるコスト削減ではなく、収益を実現するものとして扱っていることを示しています。

欧州では、GDPRへの厳格な対応と、エネルギーを考慮したルーティングを支持するグリーンITの義務付けが融合し、着実な勢いを維持しています。Elisabeth-TweeSteden Hospitalは、エクストリームネットワークスのファブリックを使用して業務を一元化し、医療データ保護規則を満たすと同時に、現場への訪問を削減しました。地域全体の政府がソブリン・クラウド・スタックの共同研究を支援し、オープンソースのオーケストレーションの需要に拍車をかけています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- データセンターネットワークのアップグレードの急増

- IoTとコネクテッドデバイスの普及

- 迅速なSD-WANと仮想化の展開

- クラウドとマルチクラウドへの移行の波

- AI駆動型自己修復インテントベースネット

- ゼロタッチ5Gネットワークスライシングの収益化

- 市場抑制要因

- 自動化スキルを持つエンジニアの不足

- レガシーインフラストラクチャの統合の問題

- 独自プラットフォームのベンダーロックインリスク

- 国境を越えた変更管理コンプライアンス

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- マクロ経済への影響の評価

第5章 市場規模と成長予測

- ネットワークインフラストラクチャ別

- フィジカル

- バーチャル

- ハイブリッド

- コンポーネント別

- ソリューション

- サービス

- 展開モード別

- クラウド

- オンプレミス

- 組織規模別

- 大企業

- 中小企業

- エンドユーザー業界別

- ITおよび通信

- 銀行および金融サービス

- 製造業

- エネルギーと公益事業

- 教育

- ヘルスケア

- 政府と防衛

- その他の産業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- ナイジェリア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Cisco Systems Inc.

- Juniper Networks Inc.

- IBM Corporation

- Hewlett Packard Enterprise Company

- Arista Networks Inc.

- VMware Inc.

- SolarWinds Corporation

- BMC Software Inc.

- Extreme Networks Inc.

- NetBrain Technologies Inc.

- Forward Networks Inc.

- Nuage Networks(Nokia Corp.)

- Huawei Technologies Co. Ltd.

- Red Hat Inc.

- Fortra LLC

- OpenText Corporation

- Fujitsu Limited

- Broadcom Inc.

- AppViewX Inc.

- F5 Inc.

- Anuta Networks Inc.

- Micro Focus International plc

- BlueCat Networks

- Apstra Inc.