|

市場調査レポート

商品コード

1939644

テレマティクス:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Telematics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| テレマティクス:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 171 Pages

納期: 2~3営業日

|

概要

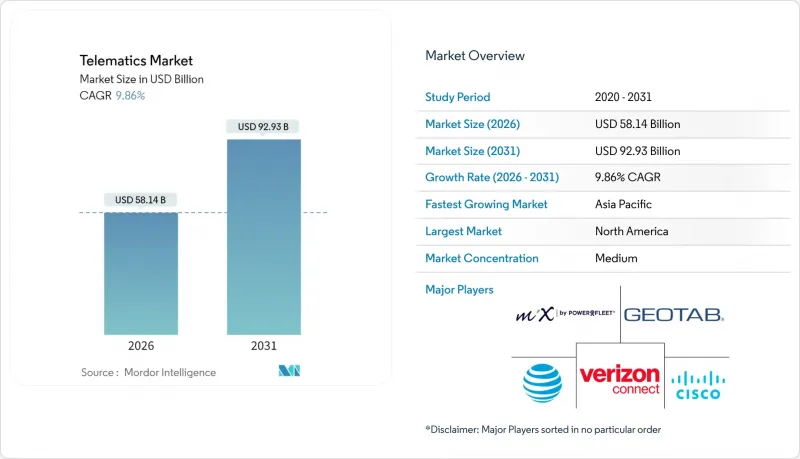

テレマティクス市場は2025年に529億3,000万米ドルと評価され、2026年の581億4,000万米ドルから2031年までに929億3,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは9.86%と見込まれます。

規制要件、特に欧州のeCallやインドのAIS 140は、自動車メーカーやフリート事業者に対し、工場レベルでの接続性組み込みを義務付けており、これがOEMの需要を加速させています。車両1台あたりの半導体搭載量は2030年までに倍増する見込みであり、ハードウェアコストは上昇するもの、高度な分析を支える豊富なデータストリームを実現します。リアルタイム運転データを活用した使用量ベースの保険プログラムは北米・欧州で急速に拡大しており、コネクテッドカーのビジネスケースを強化しています。5Gとエッジコンピューティングの急速な普及により、テレマティクスは単純な追跡から予測メンテナンスやV2X(車両間通信)へと変革を遂げています。UNECE WP.29およびISO/SAE 21434に基づくサイバーセキュリティ対応コストの上昇は、中小ベンダーに圧力をかけていますが、資金力のある企業には競争上の優位性をもたらしています。

世界のテレマティクス市場の動向と洞察

OEM組み込み接続義務の拡大

自動車メーカーは、2025年より適用されるEUデータ法など新たなデータ共有規則に対応するため、テレマティクスを車両電子機器に直接統合しています。同法はメーカーに対し、車両データをサードパーティサービスプロバイダーに開放することを義務付けています。ジオタブ社のボルボ・カーズとの提携により、同社のOEM統合は157ブランド以上に拡大し、組み込み型接続が急速に普及していることを証明しています。アナリストの試算によれば、コネクテッドサービスは1台あたり1,600米ドルの収益を生み出す可能性があり、自動車メーカーがデータを収益源と捉える動機付けとなっています。WirelessCarのような専門ベンダーは現在、OEMがデータ法を運用化する支援ツールキットを提供しており、導入スケジュールを加速させています。規制が強化される中、工場出荷時搭載ユニットが標準化されつつあり、対応可能なアフターマーケットが縮小し、テレマティクス市場の再編が進んでいます。

2025年以降、使用量ベース保険の導入が急増

保険会社は、リアルタイム運転データを活用し、人口統計に基づく価格設定から行動ベースの価格設定へと移行しています。Intuit社はZendriveの分析機能をCredit Karmaアプリに組み込み、2025年には600万人の会員に対し400万件の保険契約オファーを送信し、主流規模での展開を示しました。キアとLexisNexisはEU27カ国でドライバー評価スコア共有サービスを開始し、GDPR準拠を維持しつつ顧客登録を簡素化しました。安全運転者は最大30%の保険料割引を獲得可能となり、消費者需要を喚起すると同時に保険会社の損害率改善に寄与しています。ケンブリッジ・モバイル・テレマティクスは燃料消費量評価を追加し、保険会社が安全運転に加えエコ効率的な運転も評価するようになったことを実証しました。これらの進展はデータ中心の引受業務を強化し、テレマティクス市場の成長を加速させています。

サイバーセキュリティ対応コストの増大

国連欧州経済委員会WP.29は、自動車メーカーに対し、車両ライフサイクル全体で認証済みサイバーセキュリティ管理システムの運用を義務付けています。コンプライアンスには継続的な監視、インシデント報告、安全な更新チャネルが求められ、これによりエンジニアリングコストが増加し、開発サイクルが長期化しています。ISO/SAE 21434はライフサイクルリスク管理の手順を追加し、米国では現在、特定国からのコネクテッドカー部品の調達を禁止しており、サプライチェーン監査を強制しています。ハーマンなどのベンダーは、OEMメーカーが認証取得を進めるためのコンサルティング業務を展開しており、コンプライアンスがエンジニアリング業務から経費項目へと変容しつつあることを示しています。中小サプライヤーはこうしたコスト負担に苦慮する可能性があり、テレマティクス市場への新規参入勢いの鈍化につながりかねません。

セグメント分析

2025年時点でテレマティクス市場シェアの56.30%をアフターマーケットソリューションが占めており、これは改造車や混合フリートにおける歴史的役割を反映しています。OEMシステムは2031年までにCAGR11.62%で急速に拡大しており、よりクリーンなデータストリームとシームレスな保証統合を実現する工場出荷時接続機能への転換を示しています。テレマティクス市場はこの二つのチャネル構造から恩恵を受けています。なぜなら、古い車両には依然として後付けデバイスが必要である一方、新車はコネクティッド状態で生産ラインから出荷されるからです。

アフターマーケット向けeCallの規制標準化によりサードパーティ提供者の存在意義は維持されますが、EUデータ法などのOEMデータ共有規則は組み込み型チャネルを優遇します。自動車メーカーがコネクテッドカーのサブスクリプションを商用化するにつれ、下流価値の獲得が進み、アフターマーケットの利益余地は縮小します。このため提供者は、テレマティクス市場での地位維持に向け、分析機能と複数フリート対応性を強化しています。

2025年時点でテレマティクス市場規模の47.80%を占める組み込みユニットは、12.94%のCAGRで最も高い成長率を示しています。この移行は、予測メンテナンス、EVのバッテリー管理、規制に基づくデータ共有義務など、深い車両統合を必要とする要素によって推進されています。コスト重視のフリートではスマートフォンベースのソリューションも有効ですが、性能とデータ精度では組み込みアーキテクチャに劣ります。

フリート運営者は、電気フリートにおけるエネルギー費用を55%削減するスマート充電アルゴリズムなど、ミッションクリティカルな分析には組み込みハードウェアを好みます。5Gモジュールが標準化されるにつれ、V2Xや高精度測位といった高度なアプリケーションでは組み込みソリューションが主流となり、テレマティクス市場における戦略的重要性を確固たるものとするでしょう。

地域別分析

欧州は2025年に31.95%のシェアでテレマティクス市場をリードしました。これは義務化されたeCall、GDPRによる保護、2028年までに2,760万台と予測されるフリート管理ユニットの設置基盤に支えられています。2025年に施行されるEUデータ法はデータ共有を義務付け、プライバシー保護を維持しつつサードパーティサービスの新たな波を促進すると見込まれています。サプライヤー各社は、より厳格な統合・コンプライアンス要求に対応するため、コンチネンタルの「Aumovio」のようなコネクティビティスイートをブランド化しています。

アジア太平洋地域は最も成長が速い地域であり、2031年までCAGR12.26%で推移すると予測されています。インドのAIS 140義務化と政府による100カロールインドルピー(1,200万米ドル)の地理空間投資が、基盤となる地図インフラを拡充します。中国の新運転支援安全規制も、OEMのコネクティビティ基準を引き上げています。急速な都市化と大規模商用車両フリートが需要を創出し、世界のベンダーを現地パートナーシップへ導き、地域全体のテレマティクス市場規模を拡大させています。

北米は成熟した市場でありながら成長を続けており、ELD義務化や米国連邦調達庁によるGeotab社との40万台規模の政府車両導入契約など、政府系フリートの大規模導入が後押ししています。南北アメリカのフリート管理ユニットは2028年までに4,300万台に達すると予測されています。特定の外国製部品を制限するサプライチェーン安全保障規則により、ハードウェアコストは上昇する可能性がありますが、同時に国内の半導体投資を促進し、テレマティクス市場への長期的な供給安定化につながる可能性があります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- OEM組み込み型接続機能の義務化の拡大

- 使用量ベース保険(UBI)の導入は2025年以降に急増する見込みです

- 政府のeCallおよびAIS 140規制

- 5G/エッジ対応の無線(OTA)解析

- フリートの電動化にはリアルタイムのバッテリー分析が求められます

- モビリティ・アズ・ア・サービス(MaaS)プラットフォームの台頭

- 市場抑制要因

- サイバーセキュリティ対応コストの増加

- 初期導入時のTCU*ハードウェア価格の変動性が高め

- 複数管轄区域にわたるデータ主権の障壁

- 既存商用船隊における慣性

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- チャネル別

- オリジナル・エクイップメント・メーカー(OEM)

- アフターマーケット

- ソリューション別

- エンベデッド

- スマートフォンベース

- ポータブル/プラグイン

- 提供形態別

- ハードウェア

- サービス- エントリーレベル

- サービス- ミッドティア

- サービス- ハイエンド

- 車両タイプ別

- 乗用車

- 小型商用車(LCV)

- 大型商用車(HCV)

- 用途別

- フリート管理

- 保険テレマティクス

- 予知保全および診断

- ナビゲーションおよびインフォテインメント

- カーシェアリングおよびサブスクリプションサービス

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他のアジア

- 中東

- イスラエル

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Verizon Communications Inc.(Verizon Connect)

- Geotab Inc.

- Trimble Inc.

- TomTom N.V.

- MiX Telematics Ltd

- ATandT Inc.

- Cisco Systems Inc.

- LG Electronics Inc.

- Continental AG

- Robert Bosch GmbH

- ZF Friedrichshafen AG

- Harman International Industries Inc.

- Valeo SA

- Inseego Corp.(Ctrack)

- Microlise Group PLC

- Aplicom Oy

- Huawei Technologies Co. Ltd.

- Sierra Wireless Inc.

- Octo Telematics S.p.A.

- CalAmp Corp.