|

市場調査レポート

商品コード

1444104

PEMFC(固体高分子形燃料電池):市場シェア分析、業界動向と統計、成長予測(2024~2029年)Polymer Electrolyte Membrane Fuel Cells (PEMFCs) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| PEMFC(固体高分子形燃料電池):市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 156 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

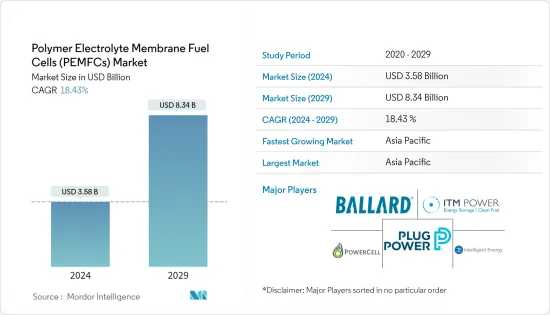

PEMFC(固体高分子形燃料電池)の市場規模は、2024年に35億8,000万米ドルと推定され、2029年までに83億4,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に18.43%のCAGRで成長します。

2020年はCOVID-19が市場にマイナスの影響を与えましたが、パンデミック前の水準に達しました。

主なハイライト

- 市場を牽引する主な要因は、燃料電池分野における研究開発(R&D)活動の増加であり、これにより、高い出力密度、燃料補給時間の短縮、保管耐久性の延長、寿命の延長など、いくつかの技術的利点がもたらされています。PEMFCのサイクルは、リチウムイオン電池などの代替燃料電池よりも優れています。これにより、PEMFC搭載車両の採用が促進されており、予測期間中に市場を牽引すると予想されます。

- ただし、PEMFC技術の現在の高コストと市場での他の実行可能なエネルギーシステムの入手可能性は、予測期間中の市場の成長を妨げると予想されます。

- 燃料電池内の白金の割合を減らし、最終コストを削減するなど、PEMFCの技術進歩により、予測期間中に市場にいくつかの機会が生まれると予想されます。

- 2022年の世界のPEMFC市場はアジア太平洋が独占しており、中国が大きなシェアを占めています。この成長の主な要因は、中国や日本などの各国政府がクリーンエネルギーの利用を促進するために始めた政策です。

PEMFC市場動向

政府の取り組みと民間投資の増加が市場を牽引すると予想される

- PEMFC市場は、主に主要市場における政府の取り組みの導入と民間部門からの投資支援の増加により、過去2年間で大幅な成長を遂げました。

- 2013年の政府イニシアチブであるカリフォルニア州エネルギー委員会の代替および再生可能燃料および車両技術プログラムは、最初の100の小売水素ステーションに共同資金を提供する長期権限を確立しました。これにより、民間部門による燃料電池市場への投資が促進されました。

- カリフォルニア燃料電池パートナーシップは、2030年までに1,000か所の水素ステーションのネットワークと燃料電池自動車の保有台数を最大100万台にすることを目指しています。

- 2022年 2月のプロジェクトでは、高温PEMFC(HT-PEMFC)が効果的な熱遮断により、大型車両やその他の大規模モビリティ用途の電動化に魅力的なソリューションを提供することが示されました。

- 燃料電池の中で最も普及しているのはPEM型です。欧州の燃料電池導入目標において重要な役割を果たし、PEMFC市場を牽引すると期待されています。

- 2022年 2月、ロスアラモス国立研究所の科学者たちは、より高温で動作する新しいポリマー燃料電池を開発しました。

- さらに、燃料電池ベースの車両の需要が世界中で増加しています。北朝鮮と米国は、燃料電池ベースの自動車の在庫において世界をリードする国です。 2021年、北朝鮮と米国は世界の燃料電池自動車在庫のそれぞれ38%と24%を占めました。

- したがって、このような政府の取り組みや投資は、予測期間中に市場を推進する可能性があります。したがって、上記の要因により、政府の取り組みとPEMFC技術への民間投資の増加が、予測期間中に市場を牽引すると予想されます。

アジア太平洋が市場を独占すると予想される

- アジア太平洋は、中国、日本、韓国などの国のクリーンエネルギー利用に対する政府の有利な政策により、PEMFCにとって有望な地域市場の一つとなっています。

- 中国は、主に水素自動車の普及促進を目的とした、国や省政府の有利な補助金や地方自治体からの奨励プログラムを背景に、同国の水素燃料電池産業が勢いを増しており、PEMFCの潜在力が最も高いと考えられています。

- 中国には潜在的に大きな市場があることに加えて、PEMFCを製造する国内企業が数多くあります。したがって、国の需要と国内の供給が存在し、市場の成長をさらに促進します。さらに、中国企業は国内外の市場に供給するため、2022年には電解槽の製造能力を1.5~2.5ギガワットに増強しようとしています。

- 一方、中国は、年間10万~20万トンの再生可能水素を製造し、2025年までに5万台の水素燃料車両を保有する計画を立てています。中国は現在、燃料電池トラックとバスの世界最大の市場であり、燃料電池の市場では第3位です。

- 最近、インドの科学者たちは、効率的な手順を通じて燃料電池用の白金ベースの電極触媒を独自に開発しました。この電極触媒は、市販の電極触媒と同等の特性を示し、燃料電池スタック性能の寿命を延ばすことができました。

- したがって、上記の要因により、アジア太平洋が予測期間中に市場を独占すると予想されます。

PEMFC業界の概要

世界のPEMFC市場の主要企業が統合されました。市場の主要企業としては(順不同)、Ballard Power Systems、Plug Power Inc.、ITM Power PLC、PowerCell Wednesday AB、Intelligent Energy Limitedなどが挙げられます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提条件

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2027年までの市場規模と需要予測(10億米ドル)

- 最近の動向と発展

- 研究開発状況

- 政府の政策と規制

- 市場力学

- 促進要因

- 抑制要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替製品やサービスの脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 地域別

- 北米

- 欧州

- アジア太平洋

- 世界のその他の地域

第6章 競合情勢

- 合併と買収、合弁事業、コラボレーション、および契約

- 有力企業が採用した戦略

- 企業プロファイル

- Cummins Inc.

- Bramble Energy

- Toshiba Corporation

- Ballard Power Systems

- Plug Power Inc.

- ITM Power PLC

- Powercell Sweden AB

- Intelligent Energy Limited

第7章 市場機会と将来の動向

The Polymer Electrolyte Membrane Fuel Cells Market size is estimated at USD 3.58 billion in 2024, and is expected to reach USD 8.34 billion by 2029, growing at a CAGR of 18.43% during the forecast period (2024-2029).

Though COVID-19 negatively impacted the market in 2020, it has reached pre-pandemic levels.

Key Highlights

- Major factors driving the market are increasing research & development (R&D) activities in the field of fuel cells, which has led to several technological advantages, such as high power density, less time to refuel, more extended storage durability, and more number of life-cycles of polymer electrolyte membrane fuel cells over its alternatives, such as Li-ion battery. This has been driving the adoption of polymer electrolyte membrane fuel cell-powered vehicles and is thus expected to drive the market during the forecast period.

- However, the current high cost of polymer electrolyte membrane fuel cell technology and the availability of other viable energy systems in the market is expected to hinder the market growth during the forecast period.

- The technological advancements in PEMFCs, such as reducing the share of platinum in the fuel cell, which in turn decreases its final cost, are expected to create several opportunities in the market during the forecast period.

- The Asia-Pacific dominated the global polymer electrolyte membrane fuel cells market in 2022, with China holding a significant share. The major factors attributing to the growth are the policies initiated by various governments in countries such as China and Japan to drive the use of clean energy.

PEM Fuel Cells Market Trends

Government Initiatives and Growing Private Investments are Expected to Drive the Market

- The PEM fuel cell market witnessed significant growth in the last two years, mainly due to the introduction of government initiatives in key markets and increasing investment support from the private sector.

- The Californian Energy Commission's Alternative and Renewable Fuel and Vehicle Technology Program, a government initiative in 2013, established long-term authority to co-fund the first 100 retail hydrogen stations. This encouraged the private sector to invest in the fuel cell market.

- The Californian Fuel Cell Partnership aims for a network of 1,000 hydrogen stations and a fuel cell vehicle population of up to 1,000,000 vehicles by 2030. The target reflects the input and consensus of more than 40 partners, including fuel cell technology companies, automakers, energy companies, government agencies and non-governmental organizations, and universities.

- In February 2022, a project showed that high-temperature polymer electrolyte membrane fuel cells (HT-PEMFCs) offer an attractive solution to electrify heavy-duty vehicles and other large-scale mobility applications due to effective heat rejection.

- Moreover, multiple institutions, including LANL (Katie Lim), Sandia National Labs (Cy Fujimoto), Korea Institute of Science and Technology (Jiyoon Jung), University of New Mexico (Ivana Gonzales), University of Connecticut (Jasna Jankovic), and Toyota Research Institute of North America (Zhendong Hu and Hongfei Jia) were involved in this project.

- Among fuel cells, the PEM type is the most popular one. It is expected to play a crucial role in Europe's target for fuel cell deployment and drive the PEM fuel cells market.

- In February 2022, scientists of the Los Alamos National Laboratory developed a new polymer fuel cell that operates at higher temperatures. The long-standing issue of overheating, one of the biggest technical obstacles to using medium- and heavy-duty fuel cells in vehicles, such as trucks and buses, was resolved by a new high-temperature polymer fuel cell that operates at 80-160 degrees Celsius and has a higher rated power density than cutting-edge fuel cells.

- Furthermore, there is a rise in fuel cell-based vehicle demand worldwide. North Korea and the United States are the leading countries in the world in terms of stock of fuel cell-based vehicles. In 2021, North Korea and the United States had 38% and 24% of world fuel cell-based vehicle stock, respectively.

- Hence, such government initiatives and investments are likely to propel the market during the forecast period. Therefore, owing to the abovementioned factors, government initiatives and growing private investments in PEMFC technology are expected to drive the market during the forecast period.

The Asia-Pacific is Expected to Dominate the Market

- The Asia-Pacific is one of the promising regional markets for polymer electrolyte membrane fuel cells due to favorable government policies for clean energy usage in countries such as China, Japan, and South Korea.

- China is considered to have the highest potential for PEMFC as the hydrogen fuel cell industry in the country has been gaining traction on the back of favorable national and provincial government subsidies and incentive programs from local authorities, mainly to encourage the uptake of hydrogen vehicles to cut pollution.

- Along with the potentially large market, China has numerous domestic enterprises that manufacture PEMFC. Hence, the country's demand and domestic supply are present, further bolstering the growth of the market. Moreover, Chinese companies seek to build their electrolyzer manufacturing capacity to 1.5-2.5 GW in 2022 to supply domestic and overseas markets.

- Meanwhile, China has plans to manufacture 100,000 to 200,000 tonnes of renewable hydrogen annually and have a fleet of 50,000 hydrogen-fueled vehicles by 2025. China is currently the world's largest market for fuel-cell trucks and buses and the third-largest for fuel-cell electric vehicles (FCEVs).

- Recently, Indian Scientists have indigenously developed platinum-based electrocatalysts for fuel cells through an efficient procedure. This electrocatalyst showed comparable properties to the commercially available electrocatalyst and could enhance the lifetime of the fuel cell stack performance.

- Therefore, owing to the abovementioned factors, the Asia-Pacific is expected to dominate the market during the forecast period.

PEM Fuel Cells Industry Overview

The key players in the global polymer electrolyte membrane fuel cells market are consolidated. Some of the major players in the market (in no particular order) are Ballard Power Systems, Plug Power Inc., ITM Power PLC, PowerCell Sweden AB, and Intelligent Energy Limited, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, until 2027

- 4.3 Recent Trends and Developments

- 4.4 Research and Development Status

- 4.5 Government Policies and Regulations

- 4.6 Market Dynamics

- 4.6.1 Drivers

- 4.6.2 Restraints

- 4.7 Supply Chain Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products and Services

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Geography

- 5.1.1 North America

- 5.1.2 Europe

- 5.1.3 Asia-Pacific

- 5.1.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Cummins Inc.

- 6.3.2 Bramble Energy

- 6.3.3 Toshiba Corporation

- 6.3.4 Ballard Power Systems

- 6.3.5 Plug Power Inc.

- 6.3.6 ITM Power PLC

- 6.3.7 Powercell Sweden AB

- 6.3.8 Intelligent Energy Limited