|

市場調査レポート

商品コード

1851425

熱交換器:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Heat Exchanger - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 熱交換器:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月01日

発行: Mordor Intelligence

ページ情報: 英文 188 Pages

納期: 2~3営業日

|

概要

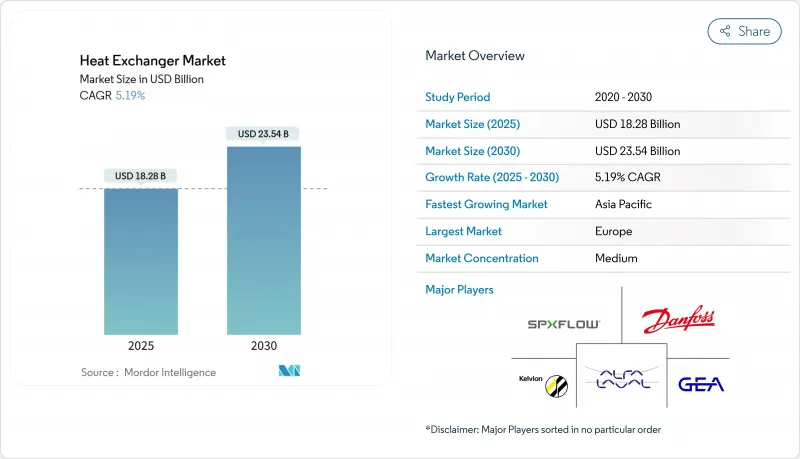

熱交換器の市場規模は2025年に182億8,000万米ドルと推定・予測され、2030年には235億4,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは5.19%です。

成長の原動力となっているのは、LNGインフラの構築、データセンターの液冷採用、産業用ボイラーや地域エネルギー・ネットワークの効率アップを促す規制などです。シェル・アンド・チューブ方式が高圧用途の主力であることに変わりはないが、節水が調達決定を後押ししているため、空冷装置が急速に拡大しています。水素のパイロット・プロジェクトや超臨界CO2パワー・サイクルに伴ってエキゾチック合金の需要が増加する一方、極圧とスペースの制約が重なる場所では、モジュール式のプリント回路設計が牽引力を増しています。一方、専門メーカーは極低温LNGトレインや200気圧水素ユニットなどのニッチをターゲットにしています。

世界の熱交換器市場の動向と洞察

LNG液化プロジェクトの急増が極低温交換器の需要を押し上げる

世界的な中規模および大規模LNGトレインの建設では、-150 °C以下で性能を発揮するコイル巻きユニットやプレートフィンユニットが必要とされる一方、厳しい熱的アプローチも維持されるため、高品位ステンレス鋼やアルミニウム合金の調達が加速しています。モジュール式熱交換器スキッドは、建設スケジュールを短縮し、コスト超過を抑制し、軽量化と乱流強化のために3Dプリントされたフロープレートを統合する製造業者に利益をもたらします。2025年から2026年にかけては、メキシコ湾岸とカタールのメガプロジェクトが熱交換器市場の中心になると予想され、アジア全域のブラウンフィールドのデボトルネッキングによる二次需要も見込まれます。ASMEセクションVIIIの認証を取得し、12週間の納期を提供するサプライヤーは、EPC企業が設備リストを標準化することでタイムラインのリスクを軽減するため、フレームワーク契約を確保すると思われます。

GCCと東南アジアにおける地域冷却の拡大がプレートフレーム販売を牽引

ドバイ、リヤド、シンガポールのような高湿度の都市部では、ピーク電力負荷を削減するために地域冷房システムに対する補助金が継続しており、ユーティリティ企業は、コンパクトな設置面積と容易な容量拡張により、ガスケット式プレートフレーム交換器を指定するようになっています。これらの配備は、塩水腐食を軽減するためにステンレスやチタンのプレートに依存しており、地区運営者は99%の可用性保証を要求しています。状態監視センサーをバンドルするOEMは、コンセッションオペレーターがパフォーマンスベースのメンテナンスモデルに軸足を移しているため、定期的なサービス収益を獲得できると思われます。

ニッケルとチタンの価格変動が耐食ユニットを押し上げる

クラス1ニッケルと航空宇宙グレードのチタン価格は、2024年以降、前四半期比で最大35%変動しており、材料をダウンスペックできない水素、海洋、オフショアプロジェクトの受注パイプラインを弱体化させています。ファブリケーターはEPCクライアントにサーチャージを転嫁するが、予算超過がプロジェクト延期の引き金となり、熱交換器市場の短期的な数量は縮小しています。ステンレス鋼クラッドプレートは露出を部分的に相殺するが、異種金属の拡散接合は溶接の完全性認証を複雑にします。

セグメント分析

2024年の熱交換器市場シェアでは、シェルアンドチューブ設計が35%を占め、圧力が60バールを超え、ファウリングマージンが高い場合の既定の選択肢としての地位を維持しています。標準化されたTEMA分類は、製油所、LNG前処理トレイン、硫黄回収装置の仕様を簡素化し、アフターマーケットの収益を支えるチューブバンドルとガスケットのリピートオーダーを支えています。同時に、インド、テキサス、中東の水不足の電力会社が液体排出ゼロ戦略を優先し、強制通風ファンと低騒音ギアボックスを搭載したユニットを駆動しているため、空冷タイプのCAGRが6%上昇しています。

2025年から2030年にかけては、設計者が従来のシェルでは対応できないコンパクトなフットプリントを求めているため、プリント回路やスパイラル巻きのフォーマットが高圧水素や超臨界CO2サイクルのシェアをかじると思われます。とはいえ、熱交換器市場では、既存のノズル位置が後付けバンドルに適合し、ライフサイクルコストを予測しやすいため、ブラウンフィールドの改修には引き続きシェル&チューブが好まれるであろう。ステンレス鋼製シェルと銅・ニッケル製チューブをブレンドした船舶用スクラバーは、IMO2020のコンプライアンス予算を獲得し、数量に若干の上昇をもたらすと思われます。

ステンレス鋼は2024年の熱交換器市場規模の30%を維持します。飲食品、製薬ラインでは、サニタリー仕上げと低炭素含有量により、割高な合金を使用しなくても規制を満たすことができます。チタン、ニッケル、インコロイ、ハステロイなどのエキゾチック合金は、2030年までのCAGRが6.5%で推移し、塩化物を多く含む塩水や水素脆化によってステンレスを選択できない水素、海水淡水化、洋上風力コンバーター・プラットフォームを取り込んでいます。

ポリマーと複合材料は、PTFEとグラファイトブロックが、特に半導体のウェットエッチングとリチウムイオンバッテリーのリサイクルにおいて、強酸性またはフッ化物を含む流れの下で金属を凌駕するため、小さな基盤から成長します。アディティブ・マニュファクチャリングは、腐食が激しい部分のみに高合金材料を配置するデュアルマテリアル格子を実現し、コストと重量を削減します。このような技術革新により、熱交換器業界は、従来のステンレスのカタログにとらわれることなく、用途に特化した冶金学へと移行しています。

熱交換器市場レポートは、タイプ別(シェル&チューブ、プレートフレーム、空冷、その他)、構造材料別(ステンレス鋼、炭素鋼、その他)、フローアレンジメント別(向流、並流、クロスフロー、ハイブリッド/マルチパス)、エンドユーザー産業別(石油・ガス、発電、水・廃水処理、その他)、地域別(北米、アジア太平洋、南米、その他)に分類されています。

地域分析

欧州は2024年の世界売上高の33%を占め、ボイラー改修と地域エネルギー展開を推進するEUのエコデザイン指令に後押しされました。ドイツの総合水素戦略は、電解槽プラントのプリント回路試作品に資金を誘導し、熱交換器市場の高価値の一角を支えています。フランスは、小型の安全クラス交換器を必要とするSMRプロジェクトを加速させ、北欧諸国は、チタンプレートパックを使用して周囲海水を利用する低温地域ループを開拓します。EN13445圧力容器認定を維持するOEMと地域内のスペアパーツハブが、アップタイム保証が入札得点の上位を占める中、シェアを獲得します。

アジア太平洋は2030年までのCAGRが最速の5.9%を記録し、中国の石油化学生産能力増強、インドの電力フリート拡大、ASEANの地区冷房利権が数量の伸びを下支えします。国内メーカーは、コスト面で有利なサプライチェーンを活用してシェル・アンド・チューブの受注を獲得し、日韓企業はアンモニア分解パイロット用のチタンとニッケルPCHEに注力しています。地元のEPCは、10週間以内に出荷されるモジュール式スキッドを提供するサプライヤーを高く評価しており、グローバルブランドは製造の現地化を迫られています。

北米では、メキシコ湾岸のLNG輸出ターミナルや、バージニア州、テキサス州、ケベック州でのデータセンター・キャンパス拡張の恩恵を受けています。米国エネルギー省の水素ハブは、拡散接合ニッケル合金を使用したPCHE実証試験に助成金を提供しています。カナダのオイルサンド事業者は、取水量を削減するためにエアフィン・ユニットを改修し、ファン・アシスト装置に二次的な吸引力を生み出しています。ラテンアメリカでは、採鉱精鉱と太陽熱発電所がブティックの受注を牽引し、中東では海水淡水化と石油化学のメガコンプレックスが需要を支えています。アフリカの勢いは、銅ベルトの製錬のアップグレードと結びついて、緩やかではあるが堅調に推移しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- LNG液化プロジェクトの急増が極低温交換機の需要を押し上げる

- GCCと東南アジアにおける地域冷房の拡大がプレートフレーム販売を牽引

- 水素パイロットプラント、200バールのサービスにプリント回路交換器を採用

- EUでは産業用ボイラーのアップグレードが義務化され、後付けチューブバンドルに拍車がかかる

- SMR(小型モジュール炉)展開には小型の安全級交換器が必要

- データセンターの液冷導入がマイクロチャンネル採用を加速

- 市場抑制要因

- ニッケルとチタンの価格変動が耐食ユニットの価格を上昇させる

- バイオリファイナリーでの採用を制限するバイオプロセスのファウリング問題

- 12週間のリードタイムに対するEPCの需要が受注生産設計を抑制

- 発電所における直接空冷は空冷式熱交換器をカニバリゼーションする

- サプライチェーン分析

- 規制の見通し

- テクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- タイプ別

- シェル&チューブ

- プレート&フレーム(ガスケットプレート、ろう付けプレート、溶接プレート)

- 空冷(フィン&チューブ、プレートフィン、マイクロチャンネル)

- 再生式(ロータリーおよびプレート)

- プリント回路

- その他(ダブルパイプ、スパイラル、コアキシャル)

- 建設材料別

- ステンレス

- 炭素鋼

- 非鉄(銅、アルミニウム)

- エキゾチック合金(チタン,ニッケル,ハステロイ)

- ポリマー・複合材料(PTFE,グラファイト,セラミック)

- フロー配列別

- 逆電流

- パラレル

- クロスフロー

- ハイブリッド/マルチパス

- 最終用途産業別

- 石油・ガス

- 化学・石油化学

- 発電(原子力を含む)

- 飲食品

- パルプ・紙

- 水処理と廃水処理

- その他の産業(自動車および輸送,冶金,鉱業, HVACR,製薬およびバイオテクノロジー)

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- 北欧諸国

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- チリ

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- エジプト

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的な動き(M&A、パートナーシップ、PPA)

- 市場シェア分析(主要企業の市場ランク/シェア)

- 企業プロファイル

- Alfa Laval AB

- Kelvion Holding GmbH

- Danfoss A/S

- SPX Flow Inc.

- GEA Group AG

- Hisaka Works Ltd.

- Xylem Inc.

- Thermax Ltd.

- Mersen SA

- API Heat Transfer Inc.

- GE Vernova Inc.

- Barriquand Technologies Thermiques SAS

- Koch Heat Transfer Company LP

- SWEP International AB

- Heatric

- Kobelco Steel Ltd.

- Accessen Group

- Funke WarmeaustauscherGmbH

- Tranter Inc.

- HRS Heat Exchangers Ltd.

- Hamon Thermal Europe SA

- Graham Corporation

- United Heat Transfer Ltd.

- KRN Heat Exchanger & Refrigeration Ltd.