|

市場調査レポート

商品コード

1687231

界面活性剤- 市場シェア分析、産業動向・統計、成長予測(2025~2030年)Surfactants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 界面活性剤- 市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

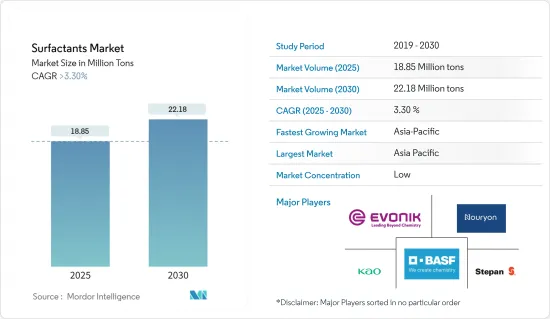

界面活性剤市場規模は2025年に1,885万トンと推定され、予測期間(2025~2030年)のCAGRは3.3%を超え、2030年には2,218万トンに達すると予測されます。

主要ハイライト

- 短期的には、パーソナルケアと化粧品産業の勃興と、洗剤とクリーナーの製造における使用量の増加が、界面活性剤市場の成長を牽引すると予想されます。

- しかし、界面活性剤の使用に対する環境意識の高まりは、市場の成長を妨げると予想されます。

- 界面活性剤のセグメントにおける新たな発明やバイオベースの界面活性剤の導入は、さらなる機会を生み出すと考えられます。

- アジア太平洋が市場を独占し、予測期間中に最も高いCAGRで推移すると予想されます。

界面活性剤市場の動向

陰イオン界面活性剤が市場を独占する見込み

- 陰イオン界面活性剤は、界面活性剤高分子の頭部が負に帯電したままの表面活性試薬の一種に属します。これにより、液体中に浮遊する不純物や粒子と結合することができます。

- 陰イオン界面活性剤は、界面活性剤市場全体のシェアの約半分を占めています。環境規制への関心の高まりにより、陰イオン界面活性剤の需要が増加すると予想されます。

- 陰イオン界面活性剤は、工業用と家庭用洗浄剤、殺虫剤製剤に広く使用されています。陰イオン界面活性剤の中では、生分解性直鎖アルキルベンゼンスルホン酸塩(LAS)が最も一般的で、廃水システムや河川水に含まれています。

- 陰イオン界面活性剤は、汚れ、粘土、一部の油性の汚れを除去するのに最適な働きをします。陰イオン界面活性剤は、イオン化によって作用します。水に加えると、陰イオン界面活性剤はイオン化してマイナスの電荷を帯びる。マイナスに帯電した界面活性剤は、粘土のようなプラスに帯電した粒子と結合します。陰イオン界面活性剤は、粒子状の汚れを除去するのに効果的です。

- 最も使用されている陰イオン界面活性剤には、スルホン酸塩、アルコール硫酸塩、リン酸エステル、アルキルベンゼンスルホン酸塩、カルボン酸塩などがあります。

- 陰イオン界面活性剤は、起泡性、洗浄性、増粘性、可溶化性、乳化性、抗菌効果、浸透促進、その他の特殊効果などの優れた特性により、パーソナルケア用途のスキンケア製品やヘアケア製品などの化粧品への需要が増加しており、需要を押し上げると予想されています。

- 現在、エコフレンドリー代替品に対する市場の需要が、バイオベースの陰イオン界面活性剤の需要を押し上げています。

アジア太平洋が市場を独占する見込み

- アジア太平洋では、中国が市場を独占すると見られています。中国では、化粧品とパーソナルケアが最も急成長しているセグメントの一つです。人口の継続的な増加も、同国におけるパーソナルケア、石鹸、洗剤の需要を煽る要因であり、界面活性剤市場を拡大しています。

- 中国の化学産業からの生産物は、石鹸、洗剤、化粧品など様々な製品に不可欠です。洗濯、ケア、洗浄剤のメーカーは国内に60社以上あります。しかし、この市場はBASF SEやEvonik Industries AGのような世界的企業が独占しています。また、中国は石鹸・洗剤製品の最大輸出国のひとつです。

- さらに、インドは世界最大の石鹸生産国のひとつです。同国の一人当たりのトイレ・入浴用石鹸消費量は約800グラムです。インドの人口の約65%は農村部に住んでおり、可処分所得の増加と農村市場の成長により、消費者は高級品にシフトしています。このシフトがインドの界面活性剤市場を牽引すると予想されます。

- India Brand Equity Foundationによると、美容・化粧品・グルーミング市場は2025年までに200億米ドルに達すると予想されています。

- 日本の経済産業省によると、2022年のカチオン界面活性剤の国内総生産量は4万6,090トンで、前年比3%以上の増加を記録しました。

- 韓国の塗料・コーティング市場はアジア太平洋で4番目に大きいです。KCC、Samhwa Paints、Kangnam Jevisco(旧Kunsul Chemical Industrial Company、通称KCI)、Noroo Paints、Chokwang Paintsが主要な塗料・コーティングメーカーです。彼らは韓国の塗料市場を独占しています。

- 全体として、この地域の界面活性剤市場は予測期間中に安定した成長を遂げると予想されます。

界面活性剤産業概要

界面活性剤市場は非常に細分化されており、上位5社のシェアはごくわずかです。市場の主要企業(順不同)には、Nouryon、Evonik Industries AG、Kao Corporation、BASF SE、Stepan Companyなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- パーソナルケアと化粧品産業からの世界の需要拡大

- 洗剤やクリーナーの製造における使用の増加

- 市場抑制要因

- 環境への懸念と規制

- その他の抑制要因

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 価格分析

第5章 市場セグメンテーション

- タイプ別

- 陰イオン界面活性剤

- 直鎖アルキルベンゼンスルホン酸塩(LASまたはLABS)

- アルコールエトキシ硫酸塩(AES)

- アルファオレフィンスルホン酸塩(AOS)

- セカンダリーアルカンスルホン酸塩(SAS)

- メチルエステルスルホネート(MES)

- スルホコハク酸塩

- その他の陰イオン界面活性剤

- カチオン界面活性剤

- 第四級アンモニウム化合物

- その他のカチオン界面活性剤タイプ

- 非イオン界面活性剤

- アルコールエトキシレート

- エトキシル化アルキルフェノール

- 脂肪酸エステル

- その他の非イオン界面活性剤

- 両性界面活性剤

- シリコーン系界面活性剤

- 陰イオン界面活性剤

- 用途別

- 家庭用石鹸と洗剤

- パーソナルケア

- 潤滑油・燃料添加剤

- 産業・施設向け洗浄

- 食品加工

- 油田用化学品

- 農業用化学品

- 繊維加工

- エマルジョン重合

- その他

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Arkema

- Ashland

- BASF SE

- Bayer AG

- Cepsa

- Clariant

- Croda International PLC

- Dow Inc.

- Emery Oleochemicals

- Evonik Industries AG

- Galaxy Surfactants

- Geo Speciality Chemicals

- Godrej Industries Limited

- Huntsman International LLC

- Innospec

- Kao Corporation

- KLK Oleo

- Lankem

- Lonza

- Nouryon

- Oxiteno

- P& G Chemicals

- Reliance Industries Ltd

- Sanyo Chemical Industries Ltd

- Sasol

- Sinopec(China Petrochemical Corporation)

- Solvay

- Stepan Company

- Sulfatrade SA

- Sumitomo Chemical Co. Ltd

- Taiwan NJC Corporation Ltd

- TENSAC

- YPF SA

第7章 市場機会と今後の動向

- バイオベース界面活性剤の用途基盤の拡大

- 特殊界面活性剤の応用におけるイノベーションの可能性

目次

Product Code: 56859

The Surfactants Market size is estimated at 18.85 million tons in 2025, and is expected to reach 22.18 million tons by 2030, at a CAGR of greater than 3.3% during the forecast period (2025-2030).

Key Highlights

- Over the short term, the rising personal care and cosmetic industry and the growing usage in the manufacturing of detergents and cleaners are expected to drive the growth of the surfactant market.

- However, the increasing environmental awareness against the use of surfactants is expected to hinder the growth of the market.

- New inventions in the field of surfactants and the introduction of bio-based surfactants are likely to create more opportunities.

- Asia-Pacific is expected to dominate the market, and it is likely to witness the highest CAGR during the forecast period.

Surfactants Market Trends

Anionic Surfactants are Expected to Dominate the Market

- Anionic surfactants belong to the class of surface-active reagents, in which the head of the surfactant macromolecule remains negatively charged. This allows it to bind to impurities and particles suspended in the liquid.

- Anionic surfactants account for approximately half of the total share of the surfactants market. A growing focus on environmental regulations is expected to increase the demand for anionic surfactants.

- Anionic surfactants are widely used for industrial and household cleaning and for pesticide formulations. Of the anionic surfactants, biodegradable linear alkylbenzene sulfonates (LAS) are the most common and can be found in wastewater systems and river water.

- Anionic surfactants work best to remove dirt, clay, and some oily stains. They work through ionization. When added to water, the anionic surfactants ionize and take a negative charge. The negatively charged surfactants bind to positively charged particles like clay. Anionic surfactants are effective in removing particulate soils.

- Some of the most used anionic surfactants are sulfonic acid salts, alcohol sulfates, phosphoric acid esters, alkylbenzene sulfonates, and carboxylic acid salts.

- The increasing demand for anionic surfactants in cosmetic products, such as skincare and hair care products in personal care applications, owing to their superior characteristics, such as foaming, cleansing, thickening, solubilizing, emulsifying, antimicrobial effects, penetration enhancement, and other special effects, is expected to boost the demand.

- The current market demand for environment-friendly alternatives has led to a boost in demand for bio-based anionic surfactants.

Asia-Pacific is Expected to Dominate the Market

- In Asia-Pacific, China is likely to dominate the market studied. In China, cosmetics and personal care are among the fastest-growing sectors. Continuous growth in population is another factor fuelling the demand for personal care, soaps, and detergents in the country, which augments the surfactants market.

- The output from the Chinese chemical industry is essential in various products, including soaps, detergents, cosmetics, etc. There are more than 60 manufacturers of washing, care, and cleaning agents in the country. However, the market studied is dominated by global players like BASF SE and Evonik Industries AG. China is also one of the largest exporters of soaps and detergent products.

- Moreover, India is one of the largest producers of soaps in the world. The per capita consumption of toilet/bathing soaps in the country is around 800 grams. Around 65% of the Indian population resides in rural areas, and the increasing disposable incomes and growth in rural markets make consumers shift to premium products. This shift is expected to drive the Indian surfactants market.

- According to the India Brand Equity Foundation, the beauty, cosmetic, and grooming market is expected to reach USD 20 billion by 2025.

- According to the Ministry of Economy, Trade and Industry (METI), Japan, in 2022, the total production of cationic surfactants in the country stood at 46.09 thousand metric tons, registering an increase of more than 3% compared to the previous year.

- The South Korean paint and coating market is the fourth-largest Asia-Pacific region. KCC, Samhwa Paints, Kangnam Jevisco (formerly Kunsul Chemical Industrial Company, popularly called KCI), Noroo Paints, and Chokwang Paints are the major paint and coating producers. They dominate the South Korean paint and coating market.

- Overall, the market for surfactants in the region is expected to witness steady growth during the forecast period.

Surfactants Industry Overview

The surfactants market is highly fragmented, with the top five companies accounting for a minimal share of the market. Some major players in the market (in no particular order) include Nouryon, Evonik Industries AG, Kao Corporation, BASF SE, and Stepan Company, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.1.1 Growing Demand from the Personal Care and Cosmetics Industry Globally

- 4.1.2 Increasing Usage in Manufacturing of Detergents and cleaners

- 4.2 Market Restraints

- 4.2.1 Environmental Concerns and Regulations

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Price Analysis

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Type

- 5.1.1 Anionic Surfactants

- 5.1.1.1 Linear Alkylbenzene Sulfonate (LAS or LABS)

- 5.1.1.2 Alcohol Ethoxy Sulfates (AES)

- 5.1.1.3 Alpha Olefin Sulfonates (AOS)

- 5.1.1.4 Secondary Alkane Sulfonate (SAS)

- 5.1.1.5 Methyl Ester Sulfonates (MES)

- 5.1.1.6 Sulfosuccinates

- 5.1.1.7 Other Types of Anionic Surfactants

- 5.1.2 Cationic Surfactants

- 5.1.2.1 Quaternary Ammonium Compounds

- 5.1.2.2 Other Types of Cationic Surfactants

- 5.1.3 Non-ionic Surfactants

- 5.1.3.1 Alcohol Ethoxylates

- 5.1.3.2 Ethoxylated Alkyl-phenols

- 5.1.3.3 Fatty Acid Esters

- 5.1.3.4 Other Non-ionic Surfactants

- 5.1.4 Amphoteric Surfactants

- 5.1.5 Silicone Surfactants

- 5.1.1 Anionic Surfactants

- 5.2 By Application

- 5.2.1 Household Soaps and Detergents

- 5.2.2 Personal Care

- 5.2.3 Lubricants and Fuel Additives

- 5.2.4 Industry and Institutional Cleaning

- 5.2.5 Food Processing

- 5.2.6 Oilfield Chemicals

- 5.2.7 Agricultural Chemicals

- 5.2.8 Textile Processing

- 5.2.9 Emulsion Polymerization

- 5.2.10 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 BASF SE

- 6.4.5 Bayer AG

- 6.4.6 Cepsa

- 6.4.7 Clariant

- 6.4.8 Croda International PLC

- 6.4.9 Dow Inc.

- 6.4.10 Emery Oleochemicals

- 6.4.11 Evonik Industries AG

- 6.4.12 Galaxy Surfactants

- 6.4.13 Geo Speciality Chemicals

- 6.4.14 Godrej Industries Limited

- 6.4.15 Huntsman International LLC

- 6.4.16 Innospec

- 6.4.17 Kao Corporation

- 6.4.18 KLK Oleo

- 6.4.19 Lankem

- 6.4.20 Lonza

- 6.4.21 Nouryon

- 6.4.22 Oxiteno

- 6.4.23 P&G Chemicals

- 6.4.24 Reliance Industries Ltd

- 6.4.25 Sanyo Chemical Industries Ltd

- 6.4.26 Sasol

- 6.4.27 Sinopec (China Petrochemical Corporation)

- 6.4.28 Solvay

- 6.4.29 Stepan Company

- 6.4.30 Sulfatrade SA

- 6.4.31 Sumitomo Chemical Co. Ltd

- 6.4.32 Taiwan NJC Corporation Ltd

- 6.4.33 TENSAC

- 6.4.34 YPF SA

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Expansion of Application Base For Bio-based Surfactants

- 7.2 Possible Innovations in the Application of Specialty Surfactants